Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Tailwinds to consumer strength are fading.

- Labor market cracks are becoming evident.

- Higher borrowing costs are a headwind for capex plans.

Planes, trains, and automobiles! That’s what this summer’s travel season has felt like for millions of Americans as their vacation plans have been interrupted by thousands of flight delays and cancellations. These widespread disruptions have been caused by unpredictable weather, staffing shortages, air traffic restrictions, and mechanical issues. And with passenger volumes up 15% over the last year and 29% of flights experiencing delayed arrivals and 6% being canceled this summer (both up sharply over 2022 levels), this busy season has been a ‘flightmare’ for travelers. And flights are not the only thing being delayed and canceled this summer. With the U.S. economy proving more resilient than expected and seemingly cruising on a flight path toward a soft landing, many prominent Wall Street strategists (including Fed staffers) are delaying or canceling their recession calls. While sentiment has made an abrupt shift, there are still plenty of risks on the horizon. Here are four reasons why we still expect a mild recession:

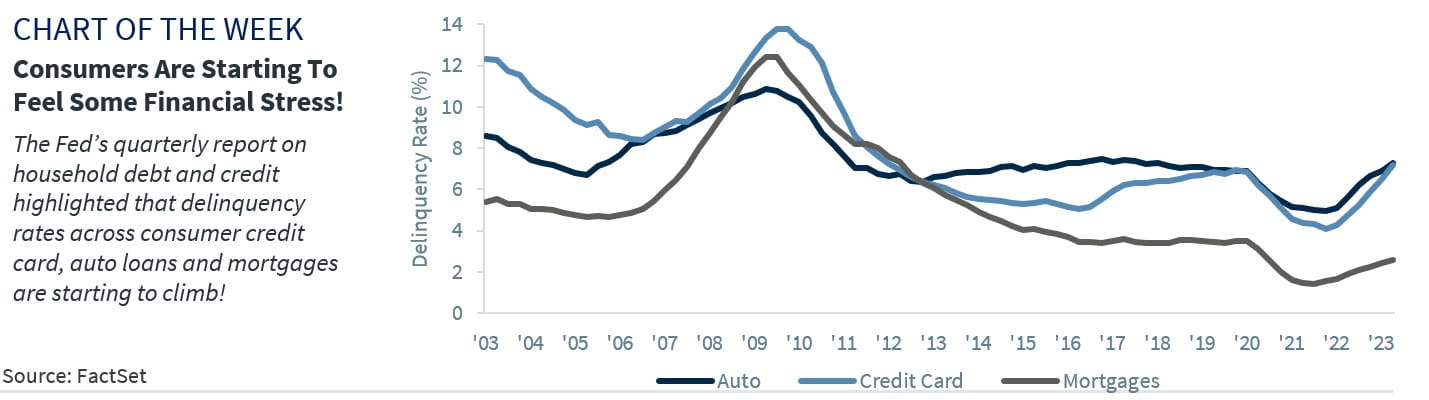

- Consumer strength likely to hit some ‘crosswinds’ | Consumer spending remains the lifeblood of the economy accounting for nearly two-thirds of economic activity. Over the last year, consumption has been supported by a historically tight labor market, the strongest wage gains in nearly forty years, and excess savings from the pandemic. However, with these tailwinds fading, the consumer’s runway may soon come to an end. With the excess savings buffer nearly depleted and likely to be exhausted by year-end, student loan payments resuming on October 1 after a three-year pause, and gas prices ticking higher, consumer spending is vulnerable to a pullback. And while consumers’ balance sheets have been reasonably healthy, signs of stress are building. For example, the Fed’s Quarterly Report on Household Debt and Credit reported an uptick in the percentage of delinquencies on credit cards, auto loans and mortgages, albeit up from low levels. And with credit card balances increasing and borrowing rates at historically high levels, consumer spending is likely to slow in the months ahead posing downside risks to economic growth.

- Employment trends are slowly ‘descending’ | While the unemployment rate continues to hover near a 53-year low of 3.5%, there are signs that the labor market is cooling. Not only did the pace of job growth (+187k) ease to its lowest level since December 2020, the six prior payroll reports were downwardly revised – the longest negative streak since 2009. And with the preliminary estimate of the annual benchmark revisions on August 23 likely to show further downward revisions, there is a strong likelihood that the Bureau of Labor Statistics has overstated the strength of the labor market. As we wait for this confirmation, other indicators, such as the declining number of job openings, easing quits rates, falling temp jobs (a historically strong signal that the labor market is weakening) and a pullback in the average workweek suggest cracks are forming in the labor market. While we’re not expecting a sharp rise in the unemployment rate during this business cycle, we do expect this softening trend to continue into year-end.

- ‘Thrust’ from services and good spending moderating | The composition of consumer spending has gone through some unusual shifts since the pandemic—with the over 20% surge in goods spending offsetting weakness in services spending during the height of the pandemic and then sharply reversing as the economy reopened and consumers en masse shifted back to spending on services, particularly on travel and experiences. However, after two consecutive summers of ‘revenge’ travel, spending on services is showing signs of fatigue. For example, airline fares have moderated on an MoM basis for three consecutive months, restaurant activity is lower relative to last year, and attendance at theme parks has softened. And the short-term economic boost from Taylor Swift’s "Eras Tour" (as flagged in the Fed’s Beige Book report) is ending as it moves overseas. Goods spending is unlikely to pick up the slack in service spending this time—suggesting that goods and service spending will be on a flat to downward trajectory.