New Kids On The BRICS: What The Bloc’s Expansion Means For The Global Geopolitical And Economic Landscape

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe BRICS nations are coming of age.

At its annual summit in Johannesburg this week, the bloc of five emerging countries—Brazil, Russia, India, China and South Africa—announced plans to expand for the first time since 2010. On January 1, 2024, the BRICS will welcome six new members: Saudi Arabia, Argentina, Egypt, Ethiopia, Iran and the United Arab Emirates (UAE).

The expansion will further establish the group as a counterbalance to the G7’s global influence, catapulting BRICS’ share of global GDP to 36% as well as covering nearly half of the world’s population.

With dozens more nations expressing interest in joining the bloc, the BRICS are clearly positioning themselves for a multipolar world, one that is not dominated by the U.S. and other members of the West.

I expect the BRICS’ rise to create both opportunities and challenges for investors. Understanding the geopolitical, economic and regulatory landscape will be critical for navigating this environment successfully.

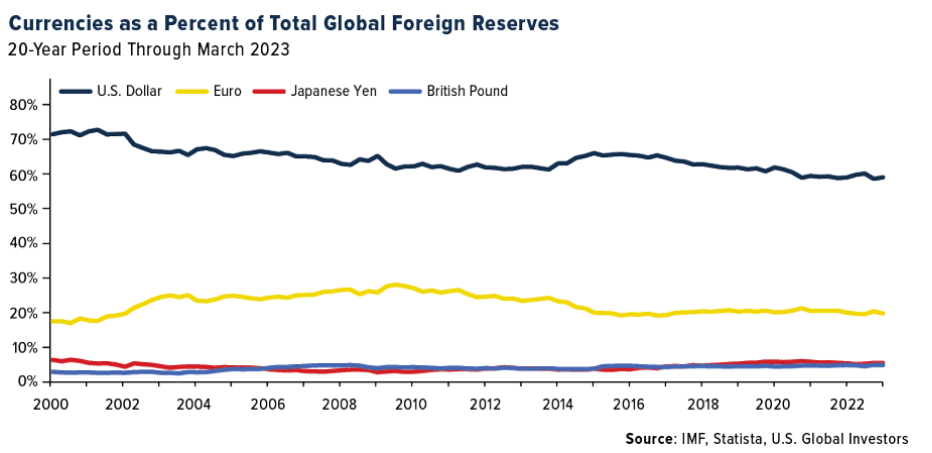

The Dollar’s Dominance Challenged

Perhaps most notably, Russian President Vladimir Putin—speaking remotely due to an International Criminal Court (ICC) arrest warrant for alleged war crimes—discussed the BRICS’ push to conduct trade in local currencies instead of the U.S. dollar, a move that would significantly reconfigure global trade dynamics.

Since the Bretton Woods Conference in 1944, the dollar’s status as the world’s primary reserve currency has offered the U.S. tremendous benefits such as cheaper financing and unparalleled leverage in the form of financial sanctions. But now, with BRICS nations seeking an alternative to the greenback (and growing their ranks from five members to 11), the currency landscape may see a new major tectonic shift, contributing to greater volatility in the Treasury market, exchange rates, inflation and more.

At the heart of this strategy lies the New Development Bank (NDB).

Established in 2015 as an alternative to Western lenders such as the World Bank and International Monetary Fund (IMF), the NDB has been making waves. Its recent decision to release an Indian rupee bond and to consider local currency bonds in other countries reflects its intent to diversify away from the dollar.

Former Brazilian leader and NDB’s current president, Dilma Rousseff, shared the bank’s ambitious plans to lend between $8 billion and $10 billion this year, with approximately 30% of the lending in local currencies. The U.S.-based financial system is “going to be substituted by a more multipolar system,” Rousseff told the Financial Times.

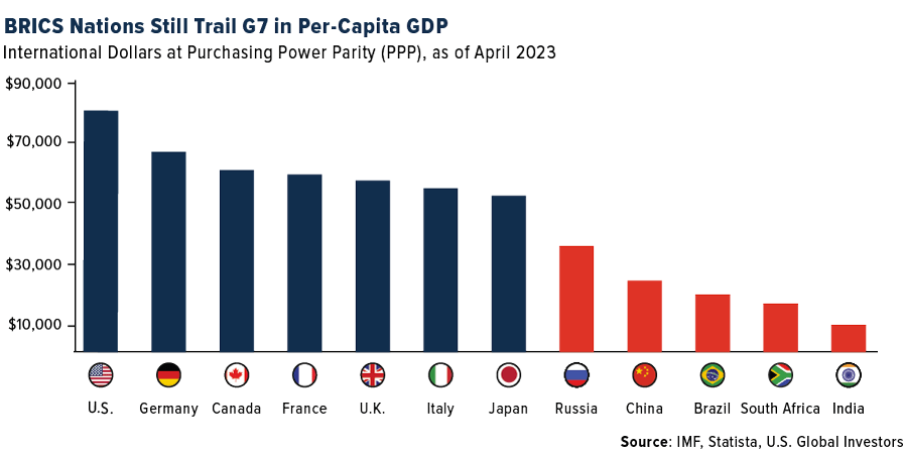

My own opinion is that the U.S. dollar will not be completely dethroned as a reserve currency, though we may end up seeing it share the stage more prominently with the euro, Chinese yuan, Bitcoin or some other currency. In their current roster, the BRICS represent over 32% of the world’s GDP, which is slightly more than the G7’s 30%; however, GDP per capita, an indicator of economic prosperity, remains a gap that the BRICS must bridge.

As the BRICS nations evolve and expand their influence, a more diversified global governance is inevitable. The current trajectory promises a world where traditional powerhouses, including the U.S. and European Union (EU), must adapt to new realities.

As an investor and an observer, staying nimble will be paramount.

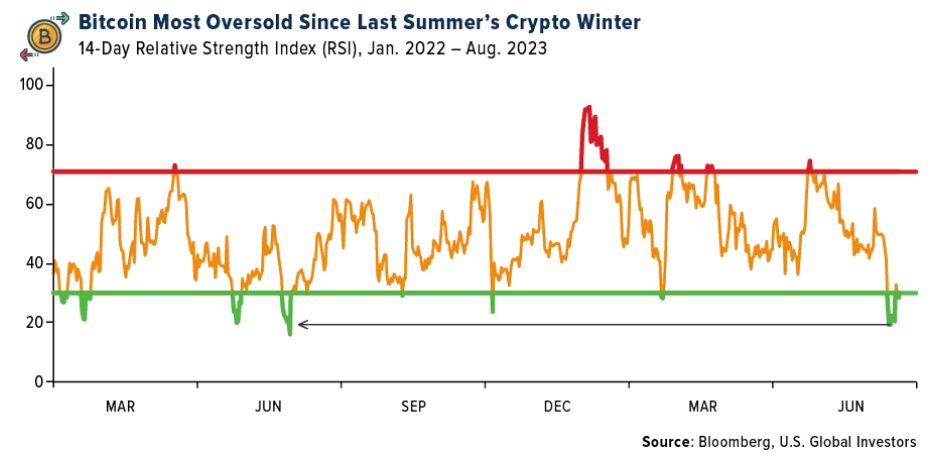

The Impact Of Rising U.S. Treasury Yields

Also shaping the market right now are rising U.S. Treasury yields. As these yields surge due to stronger-than-expected economic growth and the Federal Reserve’s tightening policies, risk-on assets, from stocks to Bitcoin, are feeling the heat. Over the past 30 days, the 10-year Treasury yield has risen some 9.4% while the S&P 500 and Bitcoin have lost 3.5% and 10.8%, respectively. Bitcoin, in fact, has fallen into the most extreme oversold territory since last summer’s crypto winter, triggered by the failures of crypto firms Celsius, Three Arrows Capital and Voyager.

With Jerome Powell asserting today at the Jackson Hole summit that it may be appropriate to hike rates further to combat inflation, investor focus could be shifting toward sectors less reliant on borrowing, like utilities and consumer staples. Still, many remain optimistic about the resilience of equities, especially in the context of a robust U.S. economy.

The standout exception to struggling equities, of course, has been artificial intelligence (AI) stocks in general and NVIDIA specifically. For the 12-month, year-to-date, three-month and five-day periods, the Santa Clara-based graphics processing unit (GPU) maker remains the top-performing S&P 500 stock by far as investors scramble to get exposure to companies involved in AI.

Gold’s Enduring Luster

In the midst of all this, gold continues its role as a stable store of value. Despite challenges like rising yields, my sentiment around gold remains bullish. Its current trading levels, though down from their peak, still indicate strong investor interest.

I’m also bullish on gold mining stocks, though I must urge investors to focus on high-quality, well-managed companies with strong balance sheets.

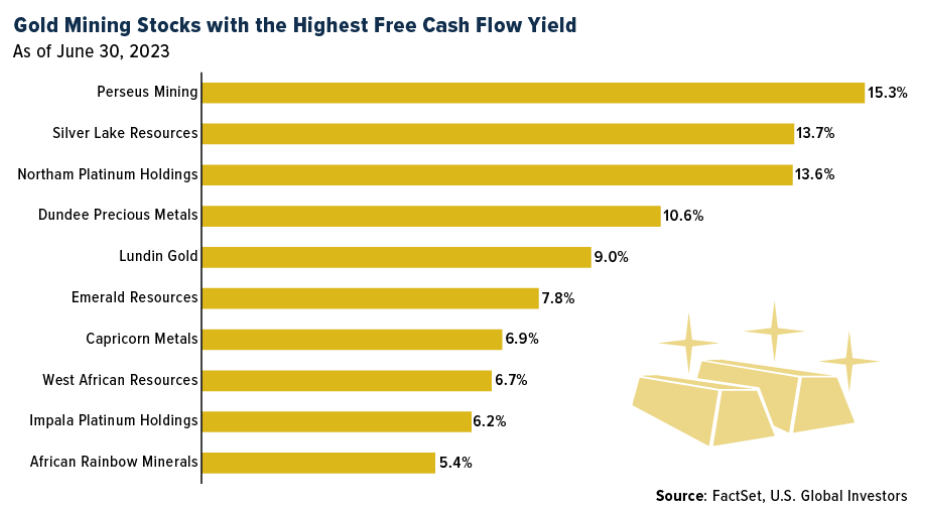

One of our favorite metrics when picking gold mining stocks is free cash flow (FCF) yield, which tells you how much free cash flow a company has relative to its market capitalization. Because explorers and producers have high operational costs and capital-intensive requirements, it’s important that they maintain healthy balance sheets.

Last month, I shared with you the top 10 gold mining stocks ranked by FCF yield, using data from the March quarter. In the chart below, I’ve updated the list for the quarter ended June 30.

Leading the pack with an FCF yield of 15.3% is Australia-based Perseus Mining, which operates three gold mines in Africa. The company reported a strong June quarter in terms of cash generation, with a net increase of $51 million in its overall cash position, taking into account cash, bullion and interest-bearing debt. At quarter-end, Perseus held $484 million in cash and physical gold, against a market cap of approximately $1.5 billion.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.45%. The S&P 500 Stock Index rose 0.90%, while the Nasdaq Composite climbed 2.26%. The Russell 2000 small capitalization index lost 0.21% this week.

- The Hang Seng Composite lost 0.08% this week; while Taiwan was up 0.61% and the KOSPI rose 0.58%.

- The 10-year Treasury bond yield fell 2 basis points to 4.228%.

Airlines And Shipping

Strengths

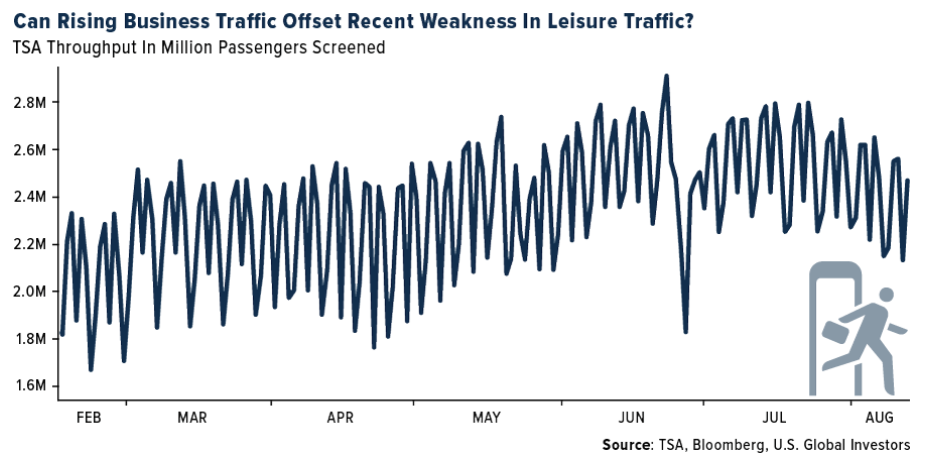

- The best performing airline stock for the week was Copa, up 3.6%. Chinese domestic travel continues its strong momentum with total spending on domestic air tickets remaining at 30% above 2019 levels in the first half of August. Japan summer demand remains strong although some of the Obon peak demand has been impacted by typhoon disruptions. Indian air travel has rebounded to above 2019 levels in recent weeks following a dip in July and early August. For long-haul flights, the summer peak demand has arrived with Taiwanese airlines seeing yields an average 30% above 2019.

- Despite the high 2021-2022 base, there may be further headroom to the current de-carbonization shipbuilding upcycle. In particular, demand for mid-sized dual-fuel (DF) containerships and tankers are expected to remain healthy in the second half of 2023, and 2024, while recent tightening of IMO regulations to drive fleet replacement for dry bulk carriers near mid-2025. Moreover, the tight demand-supply dynamics have continued to drive an ascent in newbuild price index.

- The global business travel industry has rebounded at a more accelerated rate than year-ago expectations. It is now expected to surpass its pre-pandemic spending level of $1.43 trillion in 2024 and to grow to $1.782 trillion by 2027. The forecast for 2023 is for $1.357 trillion in spend, up 32.1% year-over-year, versus last year’s forecast of $1.158 trillion. For context, in 2020 and 2021 during the depths of the pandemic, global business travel spend was $661MM and $697MM, respectively, and rebounded to $1.027 trillion in 2022.

Weaknesses

- The worst performing airline stock for the week was Allegiant, down 6.5%. Regarding the Pratt and Whitney jet engine issue, the FAA estimates 20 engines are affected on U.S.-registered aircraft only. Pratt’s August 4 service bulletin has instructed operators to remove affected engines for inspection by September 15 and RTX has indicated that 200 engines meet these criteria; therefore, the 20 engines referenced are the U.S. portion of this 200. Among U.S. operators, Spirit Airlines said that it has 13 of the 200 engines with potentially four more at JetBlue and so these would comprise most of the 20.

- Orient Overseas management believes demand weakness has played a more important role versus supply increase in the year-to-date market weakness. Management also mentioned that recent transpacific rate hikes do not represent a turnaround of the cycle. Management believes the shipping rate will remain soft unless demand becomes stronger. Profitable routes will attract extra capacity and drive down rates.

- Morgan Stanley believes the ongoing negotiations with Allegiant’s pilots could prove to be a meaningful cost headwind (especially with the Legacy’s recently announced contracts) and uncertainties surrounding the Sunseeker resort will remain until we see tangible execution. In fact, management announced last week that the opening of the Sunseeker Resort will now be delayed until later in the fourth quarter due to “unavoidable delays attributable to the lasting effects of Hurricane Ian.”

Opportunities

- Business travelers noted they are more frequently blending business and personal travel versus 2019 with 42% adding additional leisure days to their business trips. This is similar to comments heard from the airlines noting a shift in corporate travel coming out of the pandemic with an increase in “bliesure” trips.

- South Korean newspaper Dong-a Ilbo reported that Hapag-Lloyd is weighing a bid for the 38.9% stake in South Korean carrier HMM that the Korean Development Bank and the Korean Ocean Business Corporation want to sell. A combined Hapag-Lloyd and HMM would cement Hapag-Lloyd’s position as the No. 5 of the market but it is unlikely that Hapag-Lloyd, if they chose to bid for HMM, would end up winning the bidding war as the South Korean government prefers a South Korean owner for HMM. In the unlikely event of a Hapag-Lloyd and HMM tie up, Hapag-Lloyd would increase its focus on the Far East and Transpacific trade lanes and the ever-increasing consolidation in the shipping industry would enhance capacity discipline and support prices.

- Earlier this month, the U.S. Department of Transportation announced an increase in the number of Chinese passenger flights allowed to fly to the U.S. Beginning September 1, weekly roundtrips will increase to 18, increasing again to 24 per week by October 29.

Threats

- According to Goldman, for JetBlue, the main takeaway is that 2024 growth will likely be more muted compared to the company’s long-term goal of mid-to-high-single digit annual capacity growth. While capacity cuts in New York will be backfilled with new market additions, JetBlue’s fleet growth will likely fall short of its initial plan given ongoing delivery delays at Airbus which could be further exacerbated by the latest GTF issues.

- According to Bank of America, Japanese shipping continues to defy gravity with valuations near 0.8x book [trading range of 0.4-0.8] after 71% year-to-date performance. The bank is not convinced the worst is over with downside to both container and car carrier earnings ahead as supply pressures build.

- According to Cowen, the changes in its American Airlines model reflect an additional $1.0 billion in benefits the pilots are receiving following a review of United Airlines pilots’ contract. The new contract provides wage increases, snap-up provisions and quality of life benefits the pilots have been requesting for the past few years.

Luxury Goods And International Markets

Strengths

- According to Knight Frank’s Prime Global Cities Index, which tracks the performance of luxury residential prices, Dubai is leading home price growth among 46 major cities for the eighth consecutive quarter. On a year-over-year basis, home prices in the city went up by 48%. Another leading metro includes Tokyo, which saw 26.2% annual growth in the second quarter.

- At the beginning of the week, Toll Brothers, a luxury homebuilder, reported a quarterly earnings beat. The company’s quarterly sales stood at $2.69 billion, which beat the analyst consensus estimate of $2.41 billion, and rose full-year guidance for deliveries.

- Farfetch Ltd., an online retailer, was the best performing S&P Global Luxury stock in the past five days, gaining 12.26%. Citi lowered its price target for the Company from $4.3 to $3.0, maintaining a “sell” rating. The Company reported a disappointing second quarter and lowered its 2023 guidance.

Weaknesses

- The preliminary Eurozone (EU) Manufacturing PMI for August was reported at 43.7, slightly above the expected reading of 42.7, but still well below 50, separating growth from contraction. The EU’s Service PMI for August crossed below 50 for the first time since August of last year. The Manufacturing PMI in the United States weakened, falling from 49 to 47, pointing to a global economic slowdown.

- Foot Locker shares sold off sharply this week after the company reported earnings that missed Wall Street’s expectations and slashed its full year forecast amid concerns over weakening spending patterns. Shares of Food Locker suppliers, including Nike and Under Armour, corrected as well.

- Faraday Future Intelligence, an EV maker, was the worst performing S&P Global Luxury stock in the past five days, losing 37.50%. Shares dropped after the Company announced a reversed stock split at a ratio of 1 for 80. Under the reverse split, every 80 shares will be combined and converted into one share.

Opportunities

- According to Bank of America research, domestic travel demand in China is solid, and it will remain strong in the second half of the year. Many people already have travel plans during the mid-autumn festival and the October Golden Week festival. Chinese trips to Europe should also pick up in the coming months, supporting the luxury sector.

- Investment companies are becoming more interested in the luxury sector. The sector has shown resilience through challenging economic conditions as the super-rich continue to spend despite high inflation and rising rates. Tema Global Limited launched a luxury ETF (LUX US) in the middle of May this year, and this week Roundhill Investments launched another luxury ETF (LUXX US). U.S. Global Investors made an early move. On July 1, 2020, the company changed the focus of an existing mutual fund and merged the offering into luxury-focused mutual fund – recognizing this growing area of the market.

- JPMorgan said it is launching the tap-to-pay feature on iPhone for its merchant customers in the U.S., a move that will expand the number of stores that can accept payment from iPhones directly, without the need for a card reader. The bank said it will start the launch with cosmetics retailer Sephora. The luxury goods industry is influenced by technological advancements, enabling the sector to grow.

Threats

- According to The Watch Register, a company that helps owners, auction houses, and dealers identify stolen watches for a fee, luxury watches worth more than $1.3 billion have been reported as stolen or missing. The number of thefts significantly increased last year. Rolex is the most targeted brand on The Watch Register’s database, accounting for 44% of timepieces, followed by Omega and Breitling.

- According to the Federal Reserve Bank of San Francisco, the average United States consumer will run out of savings built up during the pandemic in the third quarter of this year. Earlier this year, San Francisco Fed researchers Abdelrahman and Oliveira published research estimating $500 billion of excess savings remained on household balance sheets as of March 2023, after peaking at $2.1 trillion in August 2021. But the numbers have been revised down, and now it is expected that this excess money will be depleted soon, removing a key support for consumer spending that boosted the U.S. economy.

- Next week inflation data will be released for the Eurozone and the data once again may show that food inflation is more stubborn than expected, not declining as quickly as desired by the European policymakers. Data will be released on August 31.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was the active iron ore futures contract, rising 6.43%. Iron ore rose for a fourth day on signs that demand from Chinese steel mills may be improving ahead of an expected pick-up in construction in September and October. The steel-making staple has rallied around 10% since last Wednesday’s close as sentiment improved due to the absence of government directives to cut steel production and as the post-summer ramp-up in building approaches. That is offsetting a worsening economic outlook in China.

- Europe’s Big Oils will return over $80 billion of cash to shareholders in 2023 – representing an 11.5% total cash yield on their aggregate market cap. The resilience of these shareholder distributions epitomizes one of the sector’s key signposts.

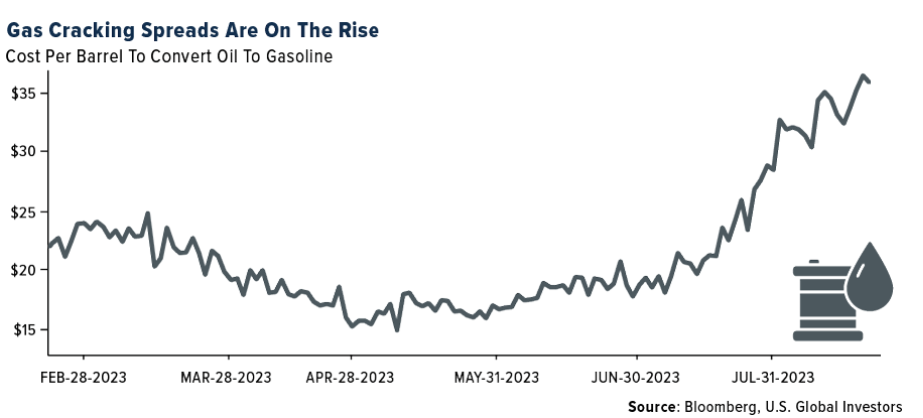

- According to UBS, Nymex diesel crack, which bottomed on April 28, has rebounded very strongly and is up 123% to $51.6/bbl. Nymex Gasoline crack, which also bottomed late April, has since moved up 25% to $37/bbl. RIN adjusted cracks in all regions (GC, Mid-Con, East Coast and West Coast) are all up $5/bbl. UBS expects delays in start-up of global refining capacity and shortages of products to keep cracks well above mid-cycle levels. Based on where the cracks are the group also sees potential upside to consensus numbers for the second half of this year and 2024.

Weaknesses

- The worst performing commodity for the week was lumber, dropping 4.02%, on construction seasonally dropping off mid-August as the late holiday season keeps buyers away. Chinese lithium spot prices fell another 8-10% as seasonal slowness and economic concerns continue to weigh on spot market sentiment. Over the past month, spodumene prices have been more resilient relative to LCE prices, resulting in a 60% collapse in Chinese conversion margins.

- According to Baker Hughes, the U.S. rig count decreased by 12 this week to 642. The land rig count decreased by 11 to 625 and the offshore rig count decreased by one to 17. Per Baker Hughes data, the oil rig count decreased by five while the gas rig count decreased by six and miscellaneous rigs decreased by one.

- In July, China’s coal production reached 378M tons, with daily average of 12.2M tons, marking a 6% month-over-month decline. This was below the NDRC’s target of 12.6M tons per day and represents the lowest level seen since October 2022. The reduction in coal production stems from disruptions caused by increased safety inspections and heavy rainfall, which have adversely impacted mining operations.

Opportunities

- Sentiment on nuclear continues to improve. Increasingly positive public opinion and growing policy support means plans for new nuclear, as well as preservation and restarts of existing nuclear fleets, are likely becoming more achievable. In recent years this change has been largely driven by increased focus on ESG, with nuclear power’s low carbon electricity generation a key strength; however, since the war in Ukraine, energy security has added a boost to sentiment.

- European natural gas advanced as workers serving a key export project in Australia prepare for a strike that could significantly dent global supplies in the run-up to winter. Disruptions risk impacting 10% of the world’s liquefied natural gas exports, a prospect that is keeping traders in Europe on edge. The region is still recovering from last year’s energy crisis, when Russian supply cuts left it highly exposed to shifts in the tight global market.

- Base metals climbed amid a broad rally in risk assets as traders eyed China’s battle to support its currency. Copper, aluminum, and zinc all gained on Tuesday, extending rallies seen in the previous session. The metals tracked rising global equity markets and received support from the weakening dollar. Investors are focusing on China’s battle to support the yuan, which is suffering due to the country’s ailing economic growth. A stronger local currency supports metals importers in the world’s top consumer by granting them greater purchasing power.

Threats

- China’s ongoing production ramp-up and import hikes have more than offset strong domestic consumption growth, resulting in a coal oversupply and significant restocking in China. Going forward, China’s coal production ramp-up could continue offsetting its strong coal consumption growth, posing a downside risk to China’s coal imports and, as a result, a significant bearish risk for the global market.

- North American E&P consensus capex forecasts are showing early signs of softening, but international operator capex expectations have moved broadly sideways year-to-date. 2024 capex forecasts for a sample of 12 North American E&Ps was flat/slightly up in the first half of this year but started to tail-off through second quarter earnings season, pulling back 2% over that period. This trend should have materialized earlier given that U.S. land rig counts are down nearly 20% year-to-date, and shale service company pricing commentary has indicated ~flat pricing at best.

- According to BMO, given the currently uncertain September scrap outlook, some easing in demand, and imports trending higher, spot HRC prices have more downside risk in the group’s opinion. However, BMO’s view remains that slowly expanding lead times, planned maintenance outages in September, and still lean service center inventories should offer some offset, absent automotive workers strike, which in their view would have a meaningful impact on the sheet market as direct shipments from mills to the auto OEMs accounted for 15% of total in 2022.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was BONE, rising 18.50%.

- JPMorgan is seeing “limited downside” for Bitcoin after its recent rout. The current selloff in crypto markets is likely near an end, the bank reasons, with long-position liquidations “largely behind us,” writes Bloomberg.

- Dubai-based crypto exchange BitOasis raised a round of fundings led by Indian digital-asset platform CoinDCX. Terms of the deal and valuation weren’t disclosed, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was PEPE, down 16.81%.

- Israeli police have accused businessman Moshe Hogeg and his partners of defrauding investors of $290 million in a cryptocurrency scam. This comes after a two-year investigation into the former owner of an Israeli Premier League soccer team, writes Bloomberg.

- A former employee at the NFT marketplace OpenSea was ordered to spend three months behind bars after being convicted in the first-ever insider-trading case involving digital assets, writes Bloomberg.

Opportunities

- Coinbase Global is sweetening its offer to buy back debt after investors agreed to tender a third of the bonds the company was seeking. It increased its compensation for the bonds to 67.5 cents on the dollar up from the 64.5 cents it was offering when it announced the tender on August 7, writes Bloomberg.

- European crypto-related exchange traded products have seen a boost in flows after BlackRock applied to launch a bitcoin fund in the U.S., according to Bloomberg.

- Coinbase Global has taken a stake in stablecoin issuer Circle citing “growing regulatory clarity for stablecoins in the U.S.,” writes Bloomberg.

Threats

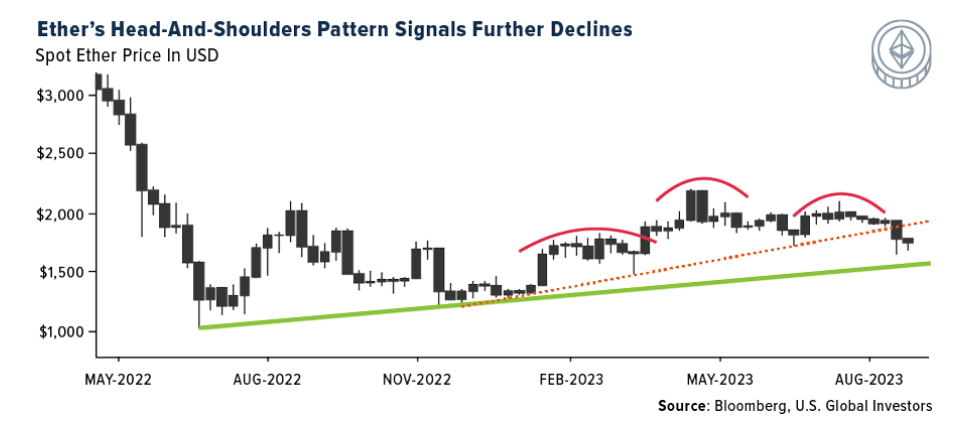

- This month’s crypto retreat may get worse if key charts for Ether prove prophetic. Ether has traced a head-and-shoulders price pattern, a technical study that signals further declines, writes Bloomberg.

- Crypto exchange Binance.US has faced a series of legal and financial challenges as regulators have increased their scrutiny of crypto companies of all kinds. For more than a month, customers of the crypto exchange have been unable to either deposit or withdraw dollars — a consequence of multiple banking partners cutting ties with the platform, writes Bloomberg.

- The U.S. Treasury Department sanctioned Roman Semenov for providing support to Tornado Cash and the Lazarus group. The sanctions were conducted in coordination with the Justice Department which unsealed an indictment against Semenov and who was arrested, according to Bloomberg.

Gold Market

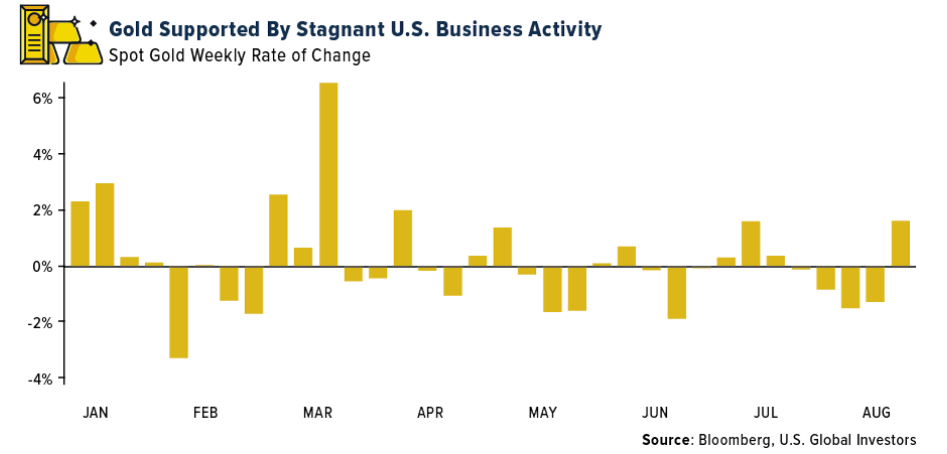

This week gold futures closed the week at $1,941.30, up $24.80 per ounce, or 1.29%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.41%. The S&P/TSX Venture Index came in off 0.83%. The U.S. Trade-Weighted Dollar rose 0.73%.

Strengths

- Gold rose for the first four days of the past week, extending a climb from a five-month low, as the dollar weakened on new economic data. Traders trimmed gains on Friday as the Federal Reserve’s monetary policy is leaning towards one more rate hike in September.

- Dundee Precious Metals announced it has entered into an investment protection agreement (IPA) with the Government of Ecuador for the Loma Larga project. The IPA grants Dundee tax stability and certain tax incentives, as well as legal protections including stability of the regulatory framework and resolution of disputes through international arbitration. Key incentives and protections for DPM under the IPA include a 5% discount on the income tax rate, fixed at 20%; tax stability on VAT and exemption on import duties for key machinery, among others. DPM also intends to meet certain additional milestones for Loma Larga, including resolution of the constitutional court case and receipt of the environmental license, prior to committing significant capital to the project.

- Resolute Mining’s headline EBITDA (earnings before interest, taxes, depreciation and amortization) of $101 million handily beat consensus of $86 million. Headline net profit after tax (NPAT) of $87 million also beat consensus of $20 million, driven by $38 million in non-cash adjustments (inventories, unrealized treasury), lower depreciation and amortization (D&A) and an income tax benefit.

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.42% on no specific news. In Zambia, mining company tax plunged 64% to 3.44 billion kwacha in the first half, while mineral royalty tax collected is down 40% year-on-year to 3.74 billion kwacha, Zambia Revenue Authority Commissioner General Dingani Banda says in Lusaka, the capital.

- Some of Mali’s top gold producers said a new law to allow the military-led government to increase its ownership of mines should not apply to existing operations, but analysts said it was likely to deter future investment. Mali’s Parliament would allow the state and local investors to take stakes as high as 35% in mining projects compared with 20% now. It will become effective once signed by President Assimi Goita, although it is unclear when that will be. “We are optimistic that, as in the past, we will find a mutually acceptable way to keep gold shining for Mali,” a spokesperson told Reuters, saying Barrick has had “constructive relationship with successive governments.”

- The prospects for jewelry in China, the main pillar of demand, look rockier. As the economy has slowed, households have conserved cash. That’s shown up in disappointing retail sales and a lapse into deflation that could worsen demand for costlier items if consumers expect prices to keep falling. Bloomberg Economics reckons the chances of deflation persisting into the first quarter of 2024 are about 35%.

Opportunities

- The near-term macro environment for gold is not that positive with U.S. real yields surging and the greenback on the rise, but bulls may be biding their time. The precious metal will likely be much stronger in about 12 months from now, according to the latest MLIV Pulse survey. The median of estimates from the 602 respondents was $2,021 an ounce, while the average was $2,074, shows the survey conducted last week. Not far below its record high of $2,075 set in 2020.

- According to Scotia, the streamers have outperformed the operators both year-to-date and shorter term, given the margin compression. With some signs of relief in inflationary pressures on operating costs, investors should start to consider rotating from the higher valued streamers (that are insulated from inflationary pressures in costs due to the nature of their business) into the lower valued operators. This is because: (1) companies have started to see easing of inflationary pressures in various input costs, which should be fully reflected in their costs once the higher cost inventories are drawn down; and (2) companies are expecting higher volumes in the second half of this year, which should also help with the costs. All of this should lead to margin expansion and help support higher valuations.

- According to Scotia, OceanaGold (OGC) is developing a pathway to achieving mining rates of at least 2 million tons per year from the underground, up from 1.6 million tons. Continuous improvement efforts include debottlenecking the mine, improving material movement, higher operational standards, visible leadership and greater crew engagement. They believe the 2023 drill program has the potential to both convert a significant amount of existing resources to reserves and expand the current resource by 50%.

Threats

- Bank of America is looking at estimate sensitivity to lower gold prices among their precious metal coverage. Based on net asset value (NAV), Kinross Gold, IAMGOLD and Eldorado Gold stand out as having particularly material downside relative to peers. Likewise, should gold go up, they have leverage there too.

- Global ETF gold holdings have declined 4.1% to 89.9 million ounces. With bond yields, which are typically negatively correlated to the gold prices expected to be pressured higher, and the Word Gold Council (WGC) calling for weaker than normal seasonal demand from India and China, ETF selling and lower gold prices may continue in near-term.

- According to Morgan Stanley, as a non-yielding asset, gold must compete for a place in portfolios – less of an issue when bond yields are low, but more challenging as yields rise. With central banks raising interest rates (except for China), it makes sense that gold ETF holdings are now the lowest since early 2020 and net long positioning is the lowest since March, with significant new shorts added.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

JetBlue

Allegiant Travel

Hapag-Lloyd

Airbus

American Airlines

United Airlines

Perseus Mining Ltd.

Northam Platinum Holdings Ltd.

Dundee Precious Metals Inc.

Lundin Gold Inc.

Emerald Resources NL

West African Resources Ltd.

Impala Platinum Holdings Ltd.

African Rainbow Minerals Ltd.

Toll Brothers

Williams Sonoma

Resolute Mining Ltd.

OceanaGold Corp.

Kinross Gold Corp.

IAMGOLD Corp.

Eldorado Gold Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on the Stock Exchange of Hong Kong, based on the average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization-weighted index comprised of publicly traded companies involved primarily in the mining of gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is a market capitalization-weighted and, at its inception, including 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index and add companies whose weight, when included, will be greater than 0.05% of the index

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries, and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investment requirements.

Purchasing power parity is a measure of the price of specific goods in different countries and is used to compare the absolute purchasing power of the countries’ currencies.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All