Is It Time For Investors To Consider Sector Rotation Amid A Tech-Heavy S&P 500?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsStocks are up 18.7% year-to-date, which is good news for portfolios and 401(k)s, but did you know that most of the heavy lifting has been done by a very small number of S&P 500 stocks?

You may be surprised to learn that more than 80% of gains so far in 2023 are due to the performance of only 10 companies, starting with Apple. The iPhone maker, valued at just under $3 trillion, contributed a not insignificant 15.6% to the market’s moves.

Apple was followed by a who’s who of mostly Silicon Valley and artificial intelligence (AI) companies. These include, in descending order, graphics card manufacturer NVIDIA (responsible for 15.4% of the gains), Microsoft (12.0%), Google parent Alphabet (9.6%, combining Class A and Class C shares), Amazon (8.6%), Facebook parent Meta Platforms (7.0%), Tesla (6.5%), semiconductor firm Broadcom (2.7%), drugmaker Eli Lilly (2.7%) and Adobe (1.8%).

There are a number of implications here that investors should be aware of, the most important being a lack of diversification. Investors who own an S&P 500 index mutual fund or ETF may be more exposed to concentration risk than they realize. Because the S&P is capitalization-weighted, superstar companies like Apple and Microsoft have a disproportionately massive impact on the index’s performance.

Also consider vulnerabilities to sector-specific risks. Most of the S&P 500’s gains in 2023 came courtesy of a single sector: technology. Any regulatory changes, economic shifts or other potential risks affecting tech will, once again, have a disproportionate influence on the index and any portfolios tracking it.

The Case For Sector Rotation

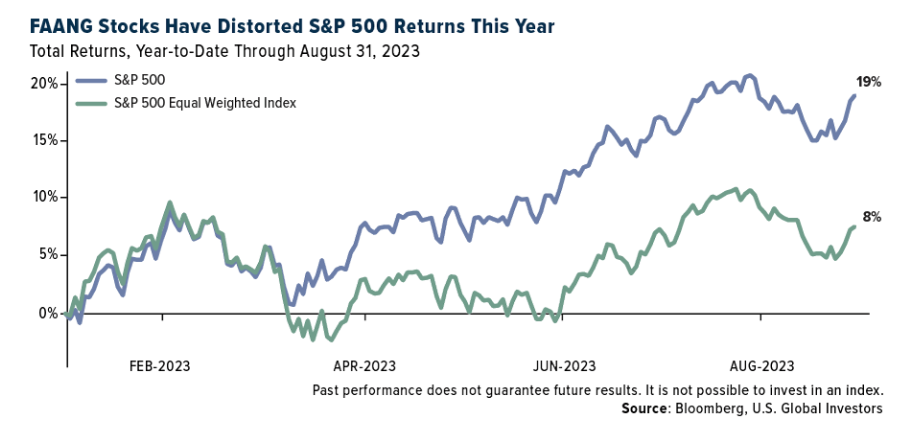

This may be easier to visualize if we compare the year-to-date performances of the S&P 500—which is weighted by market cap, remember—and the S&P 500 Equal Weight Index (EWI). As the name implies, the EWI includes the same 500 names as the original recipe index, but each company is given a fixed weight of 0.2%. Apple, then, has the same allocation as much smaller companies like Ralph Lauren (market cap: $7.65 billion) and Alaska Air ($5.74 billion).

As you can see, the market cap-weighted index significantly outperformed the EWI, 19% to 8%.

Given the current tech-sector focus, a sector rotation strategy may make sense for some investors.

Historically, leadership among sectors changes over time due to various factors such as interest rates, economic cycles, consumer sentiment and more. In a different economic environment, the next sector to lead the market could be financials or health care.

Though (tech) equities have been the star performers this year, it may be wise for investors to reconsider the role of other asset classes, including bonds, commodities, real estate, gold and Bitcoin. Many of these assets often have low correlations with stocks and could offer a cushion in times of volatility.

As loyal readers know, I recommend a 10% weighting in gold, with 5% in physical bullion and jewelry, the other 5% in high-quality gold mining stocks and funds.

The Four-Year Presidential Cycle

Another factor for investors to keep in mind is seasonality—specifically, the four-year presidential election cycle, something I’ve written about many times before. The third year of a president’s term has historically performed better than the other three years, the reason being perhaps that he’s looking ahead to reelection at the end of year four and is focused on market-friendly policies to support the economy.

Whether that’s the case with Joe Biden is up for debate, but the market’s respectable performance so far this year—the third of Biden’s four-year term—is in line with historical precedent.

Of course, none of this accounts for risk factors I already mentioned, like geopolitical tensions, inflation or unexpected economic downturns. Although it doesn’t guarantee better results, a diversified portfolio is still preferred for risk mitigation.

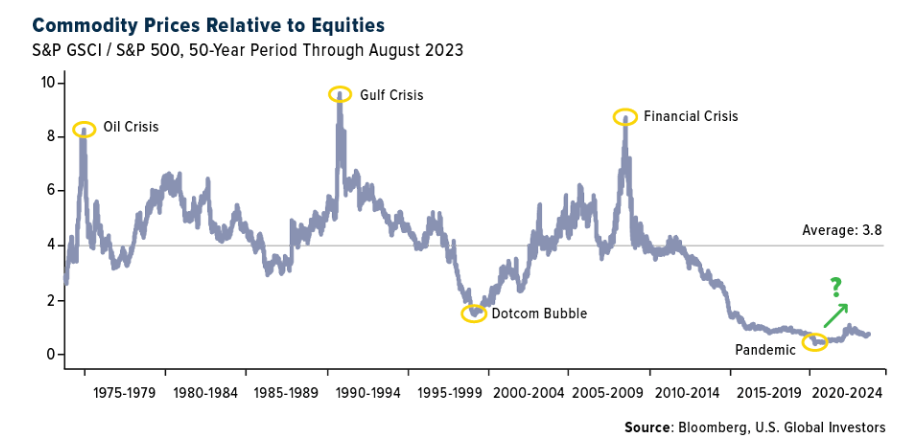

The Dawn Of A New Commodities Bull Market?

Speaking of diversification… We could be on the cusp of another structural bull market in commodities, if Stifel analysts’ projections are correct. In a report published this week, the financial services company suggests that metals and minerals are gearing up to dominate the market for the next decade after 13 years of underperforming stocks and fixed income. Indeed, commodity prices have not been keeping pace with equities, but that may be soon to change.

As Stifel sees it, a “perfect storm” of factors are stirring the pot, including the emergence of ESG (environmental, social and governance) investing, which has hiked up capital costs in the commodities sector, making higher returns imminent. Policies leaning toward the electrification of everything—think electric vehicles (EVs) and smart grids—are also going to tighten supply elasticity while increasing demand.

BRICS+ nations (Brazil, Russia, India, China and South Africa) are adding inflationary pressure to the mix by ramping up commodity demand. Western countries, meanwhile, are in debt up to their eyeballs, meaning the current monetary tightening cycle may be followed by a prolonged period of loose policymaking—good news for real, non-interest-bearing assets like commodities, gold and other minerals.

Besides gold, I prefer metals that will increasingly see higher demand as a result of decarbonization and electrification efforts. These include copper, lithium, nickel, cobalt and silver.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.43%. The S&P 500 Stock Index rose 2.40%, while the Nasdaq Composite climbed 3.25%. The Russell 2000 small capitalization index gained 3.56% this week.

- The Hang Seng Composite gained 2.01% this week; while Taiwan was up 0.99% and the KOSPI rose 1.77%.

- The 10-year Treasury bond yield fell 5 basis points to 4.178%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was SkyWest, up 10.6%. BNEF Oil research expects the demand for jet fuel to drop across September and October, in line with the seasonal trend as the end of the summer peak travel period transitions to the fall season lull.

- According to Stifel, seasonally adjusted volume data from LA/LB is encouraging, showing consecutive months of outperformance versus normal seasonality. LA/LB and the market share of imports has rebounded to 33%, up from 26%, and now well-above year-over-year and the 12-month average. While Stifel believes some rerouted shipments to the east coast are permanent, the group expects a substantial portion will eventually make its way back to LA/LB, providing a small tailwind to intermodal versus east coast.

- According to Bank of America, Japanese airlines look poised to deliver a second quarter beat and fiscal year 2023/24 guidance raise as peak summer demand arrives. Beyond the summer, the bank sees the Japanese airlines as beneficiaries of structurally higher inbound and transit demand helping keep international yields elevated consistent with stubbornly high yields globally.

Weaknesses

- The French maker of Absolute Vodka and Jameson Irish Whiskey, Pernod Ricard, expects sales to be weaker in the United States and China. U.S. consumers of premium spirits have been trimming consumption after demand soared during the pandemic. Annual profits of $3.3 billion missed analyst estimates and shares sold off this week.

- Nio, a Chinese electric car maker, posted disappointing quarterly results this week, with car sales and margins missing estimates. The company delivered 23,520 vehicles versus the planned production set at 23,792. Bloomberg reported a gross margin of 1% versus an estimated 3.25%. Nio shares traded lower.

- Faraday Future Intelligence, an EV maker, was the worst performing S&P Global Luxury stock for two weeks in a row, losing 41.52% this week. Last week the company announced a reverse stock split with a ratio of 1 for 80. This week, shares continued to trade lower following the split.

Opportunities

- According to recent positive news flow on Tesla, the company seems to be producing at least a few Cybertrucks a day at its Austin plant. The company is planning to start delivery of its long-awaited Cybertruck around the end of the third quarter. The National Highway Safety Administration could be ending its two-year-long investigation of Tesla’s drive-assistant systems Autopilots, and Full Self-Driving. Tesla also released an updated Model 3 in China with a slimmer look and a longer per-charge range at a higher price. The new Model 3 will go about 380 miles on one charge, up from about 30 miles from the old version, and the car will cost about 12% more.

- Chinese equities trading in the mainland and Hong Kong Stock Exchange gained this week supported by measures announced by the government. Last weekend, the government announced a tax cut on security transactions and lowered margin requirements for investors buying securities from 100% to 80%. In addition, China’s largest banks are preparing to cut interest rates on existing mortgages to support the property sector and cut deposit rates to shore up consumption.

- Luxury companies are adopting blockchain technology to track the authenticity and origin of high-end products. OTB Group, a member of the Aura Blockchain Consortium, runs blockchain technology specifically for luxury brands. The consortium was founded in 2021 by LVMH, Prada Group, and Richemont. When customers look up one of the 600,000 OTB products registered they can verify the authenticity of the product and see when the product was made, helping to boost the appeal of originals and make it harder to resell the fakes on the secondhand market.

Threats

- According to Bank of America research, Chinese luxury revenue was up 30% in the first half of 2023 versus the first half of 2021, but most of the improvement is due to domestic spending. In the second quarter, only 20-30% of Chinese luxury spending took place outside of mainland China versus 60-70% pre-pandemic. International travel will improve and with it, offshore luxury spending should increase, but Bank of America believes it is going to be a 2024-2025 phenomenon.

- August manufacturing PMI data is pointing to a global slowdown. In Europe, China, and the United States, the indexes measuring the manufacturing activities remain below 50 and in contractionary territories. The U.S. Manufacturing PMI was reported at 47.9, China at 49.7, and the Eurozone at 43.5. Caixin PMI (which measures production activity among Chinese smaller/private firms) unexpectedly crossed above the 50-mark, diverging from the China Manufacturing PMI (which tracks the manufacturing activity among larger state-owned companies).

- China is an important market for Tesla and competition is growing there. Tesla sold roughly 294,000 units in China in the first half of 2023, up almost 50% year-over-year. The company is expected to sell roughly 1.8 million units around the world in 2023, and Wall Street projects 2.4 million units to be sold in 2024. Tesla shares have been volatile in the month of August, following the busy week of positive/negative news flow on Tesla.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was crude oil, rising 7.58%. U.S. natural gas consumption was up 7% year-over-year this past week, driven by an increase in power burn and industrial demand. On a week-over-week basis, total demand decreased by 0.6 Bcf/d from lower power demand (-0.7 Bcf/d).

- Oil rose for a sixth day, as a slump in U.S. crude inventories added to signs of market tightness and as wider markets climbed. West Texas Intermediate traded above $82 a barrel, set for the longest run of increases since January. Prices were aided by gains in risky assets, with U.S. equity futures and stocks in

Europe climbing. - China’s refined zinc imports spiked to the highest level in more than four years after the country’s stimulus measures supported local prices, making inbound shipments more profitable. Imports of refined zinc, used in galvanizing steel, rose to 76,797 tons in July, the highest since April 2019, according to Chinese customs data. Imports more than tripled in the year’s first seven months from the same period in 2022.

Weaknesses

- The worst performing commodity for the week was lithium hydroxide, dropping 4.23%. Weighted average lithium prices were down 10.7% over the past two weeks, per Benchmark, with current prices around $34K- $40K depending on the grade. Benchmark noted this was driven by spot demand remaining weak for lithium chemicals, coupled with international contract prices falling in a lagged response to declining spot prices in Asia.

- UBS updated its U.S. natural gas supply/demand model to reflect EIA data through May and forecasted second half 2024 trends with balances projected to be 0.5-1.0Bcfpd oversupplied in 2024. Relative to the group’s $3.50/MMBtu FY24 HH forecast, the supply/demand outlook points to greater downside versus upside risk to price, with winter weather the key near-term driver. Additionally, with Lower48 supply holding in better than expected, any recovery in the rig count could loosen balances further.

- According to Baker Hughes, the U.S. rig count decreased by one this week to 631. The land rig count decreased by two to 631 and the offshore rig count increased by one to 17. As per Baker Hughes data, the oil rig count remained flat while the gas rig count decreased by one.

Opportunities

- Chile’s Minister of Economy sent a clear message welcoming private initiative to invest in lithium, indicating there is potential for stable rules of the game for current and entry of new players. Details should be coming in the next few months, a key for the sector and global lithium dynamics.

- China’s Zijin Mining Group Co. is developing plans to expand its copper mine in eastern Serbia due to demand for the metal considered vital to the global energy transition — an effort that could cost billions of dollars. The company opened the Cukaru Peki copper and gold mine almost two years ago, with a $678 million investment allowing it to reach reserves a few hundred meters deep. Now it wants to drill down almost 2 kilometers (1.25 miles) to make the most of assets acquired in a takeover spree. “These are vast reserves, which require additional

infrastructure, additional investment of around $3.5 billion to $3.8 billion,” said Branko Rakocevic, the top Serbian official at the mine, whom the Chinese company authorized to speak with reporters. - Aluminum climbed in London, with Morgan Stanley analysts forecasting that supply challenges in China could drive the market into deficit and support a long-term rally in prices. The lightweight metal rose as much as 1.2% on the London

Metal Exchange, climbing from an 11-month low struck last week as rebounding output in China and ructions in the country’s property industry weighed on sentiment.

Threats

- JPMorgan attended the largest U.S. steel industry conference in Atlanta this week and concluded that benchmark sheet prices have further room to fall amid cautious buyers sticking to contract volumes and/or buying ‘hand to mouth.’ This is largely a function of concerns over a potential United Auto Workers (UAW) strike at the Big Three Detroit auto makers in September, which could result in a significant portion of shipments being redirected to the spot market. Yet, many steel buyers said underlying demand was “holding up” for now. Benchmark HRC was last reported at $755 per ton, according to Platts (-12% QTD), with lead times hovering in the normal 4–6-week range.

- According to ExxonMobil’s energy outlook, oil and gas are projected to still make up 54% of the world’s energy supply by 2050 with the world failing to keep global temperature increases below 2 degrees Celsius. Oil use is expected to decline significantly in personal transportation but will remain essential for the industrial processes, while natural gas use is projected to increase by more than 20% by 2050 given its utility as a reliable and lower-emissions source of fuel. Given that oil and natural gas are projected to remain a critical component of a global energy system through 2050, sustained investments are essential to offset depletion as production naturally declines by 5-7% per year.

- The military coup in Gabon brought investors’ focus onto the international companies that help OPEC’s second-smallest member produce about 200,000 barrels of crude a day and other key minerals. Soldiers seized power four days after disputed presidential elections. The country’s former colonial ruler France has maintained strong business ties there, despite widespread concerns about its democracy and human rights record.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Toncoin, rising 32.08%.

- The resurgence story of EOS Network, a blockchain that raised $4 billion in its ICO with little to show in its early years, is briskly shaping up as EOS tokens were approved for trading on Japanese exchanges, as per a press release Wednesday, writes Bloomberg.

- The defeat of efforts to block a Bitcoin exchange-traded fund unleashed gains across the crypto space this week, including the price of Bitcoin, writes Bloomberg. The rally happened after Grayscale scored a legal victory this week in federal court.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Hedera, down 15.03%.

- One closely watched measure of Bitcoin mining revenue is hovering around a record low as the price of the largest digital asset stagnates and competition heats up, writes Bloomberg. The hashprice fell to $0.06 for a unit of computing power per day on Sunday, according to Hashrate Index data.

- Binance Asia-Pacific’s head Leon Foong is leaving the exchange. Foong, who led the expansion into markets like South Korea, Thailand, and Japan has resigned following the departure of other senior executives including chief strategy officer Patrick Hillman and general counsel Hon Ng, writes Bloomberg.

Opportunities

- The Cosmos Hub is voting on a major software upgrade proposal to replace existing staking, distribution, and slashing modules with the Liquid Staking Module. Enabling the LSM is a significant development for network liquidity and unlocking millions of dollars’ worth of ATOM tokens, writes Bloomberg.

- Robinhood Wallet, a multi-chain self-custody Web3 wallet, has expanded its offering to include support for Bitcoin, Dogecoin, and in-app Ethereum swaps, according to an article published by Bloomberg.

- Crypto exchange platform Coinbase said on X (formerly Twitter), that it has added PayPal stablecoin for trading on its platform, writes Bloomberg.

Threats

- The U.S. SEC has taken its first enforcement actions against NFTs, widening its assault on cryptocurrencies, and raising a host of questions for issuers, exchanges, buyers, and sellers of digital assets that can be used to transfer ownership of anything from artwork to real estate, writes Bloomberg.

- Ivan Bianco, a blockchain gaming-focused YouTuber based in Brazil who runs the channel Fraternidade Crypto, apparently had nearly $60,000 worth of cryptocurrency and a stash of NFTs stolen this week after accidentally revealing his crypto wallets seed phrases during a livestream.

- A group of specialists at Jump Crypto, one of the digital-asset world’s top market-making firms, have left to start a new software company focused on developing a financial data feed project built on blockchains, writes Bloomberg.

Gold Market

This week gold futures closed the week at $1,966.80, up $26.90 per ounce, or 1.39%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.40%. The S&P/TSX Venture Index came in up 1.77%. The U.S. Trade-Weighted Dollar rose 0.17%.

Strengths

- The best performing precious metal for the week was platinum, up 2.09% as hedge fund managers flipped their view that it was more attractive to be long futures now. According to BMO, Petra Diamonds reported the results of Tender 1 (F2024) with a marked improvement in diamond sales and revenue over Tender 5, which was expected given the deferral of Tender 6 (F2023). However, like-for-like rough diamond prices declined 4.3% from Tender 5.

- Dundee Precious Metals said that a court in Ecuador has reaffirmed its project concessions in the country and clarified expectations of the company toward certain local indigenous groups. Based on the Canadian gold miner’s preliminary analysis of the appeal of the Constitutional Protective Action filed against Ecuador’s Ministry of Environment, Water and Ecological Transition, the decision reaffirmed the company’s mining concessions for the Loma Larga project.

- Gold held around the highest in three weeks as U.S. inflation data printed in line with forecasts. The metal edged higher Thursday for a fourth session, after drawing support from weaker than expected U.S. economic data that diminished expectations of another rate hike by the Federal Reserve. Swaps contracts are now pricing in less than a 50% chance of another quarter-point increase this year. That has helped gold recover from a slide below $1,900 earlier in August, though it is still on track for a monthly loss of about 1%.

Weaknesses

- The worst performing precious metal for the week was palladium, down 0.59% as hedge funds pushed their net short position to a three-month high. Zijin Mining reported first-half recurring profit of Rmb10.418bn, 8% below consensus, due to lower-than-expected gold and zinc profit. The company declared an interim dividend of Rmb0.05/share, implying 13% payout ratio, versus nil in the first half of last year.

- Europe’s top copper producer Aurubis AG warned it may face losses in the hundreds of millions of euros after being hit by a massive scam involving shipments of scrap metal that it uses in its recycling business. Aurubis believes some of its suppliers have manipulated details about the scrap metal they provided and had been working with employees in the company’s sampling department to cover it up.

- Anglo American’s De Beers sold a provisional $370 million of rough stones in the seventh sale of 2023, compared with $411 million at the prior sale and $638 million a year earlier. “With the prevailing economic environment leading to softer end client demand for diamond jewelry in key consumer markets, and the traditionally lower levels of midstream trading during the summer period, sight holders continued to take a prudent approach to their purchasing during the seventh sales cycle of the year,” De Beers CEO Al Cook said.

Opportunities

- According to J.P Morgan, gold’s negative beta to real yields has historically been weaker over Federal Reserve hiking cycles while also displaying an overall more erratic relationship. Nonetheless, as the Fed pauses, cuts and then holds rates at a low level, the relationship and negative beta both steadily strengthen. This, in part, could also explain some of gold’s resilience in the face of the Fed’s most aggressive rate hiking campaign in 30 years. In their view, it also supports their thesis that an eventual push lower in real yields as the Fed moves towards cuts will catalyze further upside for gold prices in the coming year.

- According to Bank of America, for Hochschild Mining’s Volcan gold project in Chile’s Atacama region, recent studies based on heap leach processing and upfront capex of $900 million suggest Volcan would produce around 3.8 million ounces (Moz) of gold over 14 years with a net present value (NPV) of $826 million and an internal rate of return (IRR) of 21% at $1,800 per ounce of gold.

- Investor sentiment supporting gold’s prospects aligns with the outlook that real yields will either decrease or remain stable. Money managers are positive about the gold price in 2024, according to a recent survey, even though there are tough

challenges like a stronger dollar and the chance of even higher U.S. interest rates. Significantly, none of the respondents to the survey said they would cut their exposure to gold next year; some are even thinking about investing more.

Threats

- According to Bank of America, Fed Chair Jerome Powell delivered a moderately bearish message for gold at Jackson Hole: still-too-high inflation could merit further rate hikes (and rates are negatively correlated with the gold price).

- UBS expects some ongoing execution risk at Newmont to persist through the end of the year. In particular, the Penasquito mine in Mexico remains shut down since June 6, and timing of a restart is uncertain. Furthermore, they expect few upside catalysts before the Newcrest acquisition is closed later this year and Newmont has a chance to issue combined guidance.

- Junta leader Assimi Goita signed into law mining code that gives the state and domestic investors the right to take a stake of up to 35% in mining projects, compared with 20% previously. “The new mining law’s promulgation is part of the preservation of the interests of the Malian people,” Goita says in statement posted on X, formerly known as Twitter.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

Boeing

Hapag-Lloyd

HMM Co Ltd

American Airlines

Delta Air Lines

JetBlue Airways

United Airlines

Lululemon

Brunello Cuccinelli

Pernod Ricard

Nio

Tesla

LVMH

Prada Group

Richemont

Alaska Air Group Inc.

Dundee Precious Metals Inc.

Hochschild Mining PLC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P GSCI provides investors with a reliable and publicly available benchmark for investment performance in the commodity markets.

Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole. Stocks with betas higher than 1.0 can be interpreted as more volatile than the S&P 500.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All