August update

- Municipals posted negative total returns amid rising interest rates.

- Issuance exceeded tempered expectations, while demand waned as performance struggled.

- Late-cycle macro dynamics and fading seasonal tailwinds could create opportunity in the autumn.

Market overview

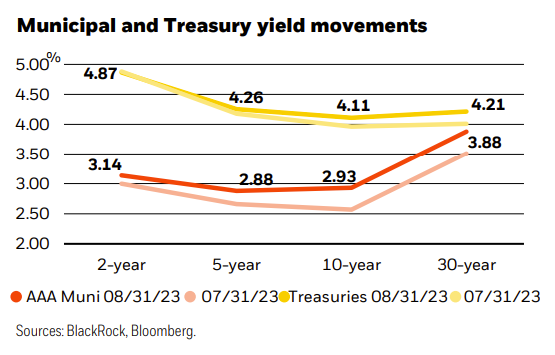

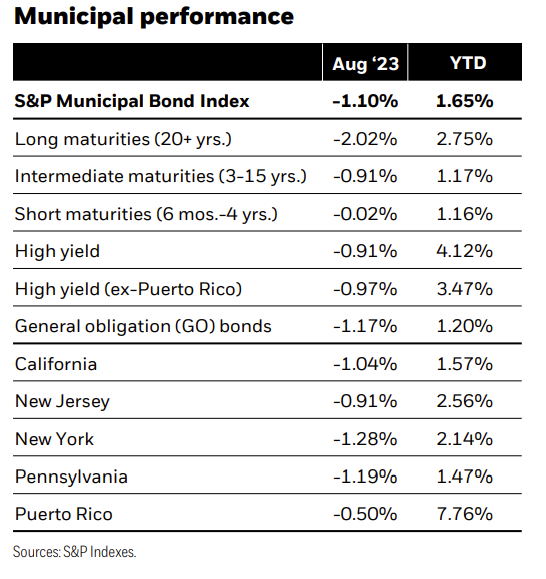

Municipal bonds deviated from the seasonal trend and posted negative total returns in August. Interest rates rose on the back of resilient economic growth, elevated Treasury supply, and a hawkish tone from the Federal Reserve (Fed) at the Jackson Hole Economic Symposium. The yield on the benchmark 10-year Treasury note closed at a new cycle high of 4.34% late in the month. Rich valuations and less favorable supply-and-demand dynamics prompted municipals to underperform comparable Treasuries. The S&P Municipal Bond Index returned -1.10%, bringing the year-to-date total return to 1.65%. Shorter-duration (i.e., less sensitive to interest rate changes) and higher-rated bonds performed best.

Issuance exceeded expectations at $37 billion, a 40% month-over-month increase, bringing the year-to-date total to $234 billion, down 10% year over year. As a result, the typical tailwind provided by net negative supply was subdued, as reinvestment income from maturities, calls, and coupons outpaced issuance by just $9 billion, compared to $14 billion last year. At the same time, demand waned alongside performance, and the asset class posted its first monthly net outflow since May.

While we acknowledge that near-term volatility will likely remain elevated, we believe that the next couple of months may prove to be a favorable period to add duration. Interest rates have historically peaked about two months prior to the end of a Fed tightening cycle, making the recent increase in yields a potential opportunity. In addition, supply-anddemand technicals in the municipal market tend to turn less constructive in September and October before strength reemerges into year-end, making the autumn a great time to buy ample supply at bargain prices.

Strategy insights

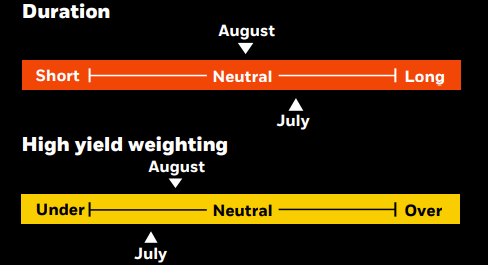

We maintain a neutral-duration posture overall. We prefer an up-in-quality bias and remain increasingly selective in non-investment grade. We strongly advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15-20-year part of the curve.

Overweight

- Essential-service revenue bonds

- Select highest-quality state and local issuers with broadest tax support Flagship universities

- Select issuers in the high yield space

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

- Senior living and long-term care facilities in saturated markets

- Lower-rated private universities

- Stand-alone and rural health providers

Credit headlines

Last month, brush fires erupted in the State of Hawaii’s county of Maui that spread rapidly due to strong winds from Hurricane Dora. The West Maui wildfire was the most devastating natural disaster in the state’s history with reports that it had completely burned down the historic town of Lahaina. Municipal bond exposure to this natural disaster is primarily related to GO debt issued by the county of Maui. Tourism drives Maui’s economy, and we expect the West Maui wildfire will impact visitor data in the short term, but nothing on the scale of the pandemic. Wildfire risk is not new to the State of Hawaii, but this tragic event underscores an increased risk to residents and visitors, as well as the state’s property insurance market.

A bigger risk to the municipal market is debt issued from the Hawaiian Electric Company, an investor-owned utility being targeted for its equipment’s potential role and contribution to the devastation in Lahaina/West Maui. The company has retained a restructuring advisor, has had its credit ratings cut to junk by all three agencies, and has been subject to notable declines in both market capitalization and bond prices. The county of Maui has sued the company, claiming negligence in maintaining equipment that was responsible for igniting the fire. However, Hawaiian Electric has revealed details of its own investigation that shows while its power lines did ignite a small fire on the morning in question, the fire was reported as “extinguished” by Maui County Fire Department. In addition, all power lines in the area were deenergized at the time the second wildfire ignited, which ultimately was responsible for the massive destruction to Lahaina. The situation is quite fluid in these relatively early stages, and we expect, given more time, investors will gain further clarity as to what exactly occurred in this tragedy.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 8, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: Equities are essential portfolio building blocks. Join VettaFi for the Equity symposium.

© BlackRock

Read more commentaries by BlackRock