Key takeaways:

- In many ways 2023 continues to be the mirror image of 2022, with the most volatile assets being some of the best performers for much of the year.

- Growing evidence of an economy that is slowing warrants an allocation to low volatility equities with a focus on companies who are able to provide stable and consistent earnings.

Russ Koesterich, Managing Director, discusses why a moderation in economic growth may warrant an increased allocation to lower volatility stocks in portfolios.

In many ways 2023 continues to be the mirror image of 2022. One market dimension where this is most apparent: For much of the year, the most volatile assets have been some of the best performers. Last year the most volatile companies were sold as investors wrestled with a rapid rise in inflation and surging interest rates. In contrast, 2023 has witnessed a surprisingly rapid return to these same companies.

Through the July market peak, the volatility style factor, i.e. companies with more price volatility than their peers, outperformed. Since then, there has been a shift in investor preferences towards stability. As more evidence builds that the economy is slowing, investors are less willing to embrace volatility. Assuming further economic moderation in the coming quarters, investors should consider raising their weight to less volatile, more stable companies.

After underperforming their more volatile peers for most of the year, low volatility stocks and indices have been posting better relative performance since the start of August. While absolute returns have still been nominally negative, low volatility indices have outperformed by roughly 200 bps. The converse is also true. After ripping higher in January and then again in the spring, more volatile securities have come under pressure as the market has turned lower.

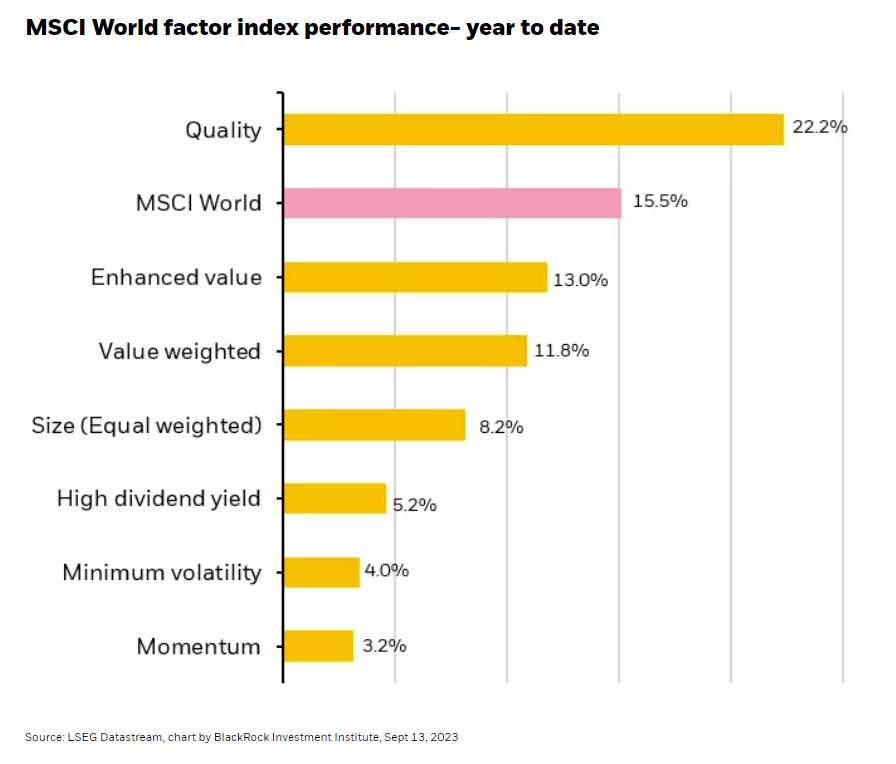

Stability Counts When Growth Slows

There are several possible explanations for the recent outperformance in low volatility stocks. After a summer of surprisingly resilient economic data, there is growing evidence the economy is slowing. Both job growth and inflation are moderating and there are signs of stress in pockets of the household sector. As typically happens, as the economy slows investors prefer more stable companies and more predictable earnings.

Valuation discrepancies may also be helping. Despite recent relative strength, low volatility stocks have significantly underperformed the market as well as other investment styles (see Chart 1). Prolonged underperformance has left these companies relatively cheap. Looking at the ACWI Low Volatility Index versus the traditional global ACWI Index confirms the relative value discrepancy. Low vol stocks are trading at roughly 17x forward earnings versus nearly 20x for the broader global index. To the extent that investors often pay more for higher quality, the current discount in less volatile companies is worth noting.

Not Just About Price

Our base case continues to be no U.S. recession, but even without an official contraction we are likely to see a slowdown. Economic slowdowns typically favor companies in more stable industries, notably staples and utilities. That said, I don’t think investors need limit themselves to the traditional defensive playbook.

Low volatility’s advantage stems from company fundamentals as much as price behavior. This suggests broadening the search to includes companies, regardless of industry, with more stable revenue, earnings, and margins. In addition to staples and utilities, many software, healthcare service and payment companies also display these characteristics. While this year’s rebound has generally favored taking a flier on many of last year’s biggest losers, slower economic growth should shift the investment narrative towards stability and consistency, regardless of the industry.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risks, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

The BlackRock Model Portfolios are provided for illustrative and educational purposes only, do not constitute research, investment advice or a fiduciary investment recommendation from BlackRock to any client of a third party financial advisor (each, a "Financial Advisor"), and are intended for use only by such Financial Advisor as a resource to help build a portfolio or as an input in the development of investment advice from such Financial Advisor to its own clients and shall not be the sole or primary basis for such Financial Advisor’s recommendation and/or decision. Such Financial Advisors are responsible for making their own independent fiduciary judgment as to how to use the BlackRock Model Portfolios and/or whether to implement any trades for their clients. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock Model Portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock Model Portfolios or any of the securities included therein for any client of a Financial Advisor. Information and other marketing materials provided by BlackRock concerning the BlackRock Model Portfolios –including holdings, performance, and other characteristics –may vary materially from any portfolios or accounts derived from the BlackRock Model Portfolios. Any performance shown for the BlackRock Model Portfolios does not include brokerage fees, commissions, or any overlay fee for portfolio management, which would further reduce returns. There is no guarantee that any investment strategy will be successful or achieve any particular level of results. The BlackRock Model Portfolios themselves are not funds. The BlackRock Model Portfolios, allocations, and data are subject to change.

For financial professionals: BlackRock’s role is limited to providing you or your firm (collectively, the “Advisor”) with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of the Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for a client’s account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein for any of the Advisor’s clients. BlackRock does not place trade orders for any of the Advisor’s clients’ account(s). Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics–may not be indicative of a client’s actual experience from an account managed in accordance with the strategy.

For investors: BlackRock’s role is limited to providing your Advisor with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of your Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for your account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein. BlackRock does not place trade orders for any Managed Portfolio Strategy account. Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics—may not be indicative of a client’s actual experience from an account managed in accordance with the strategy. This material is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock