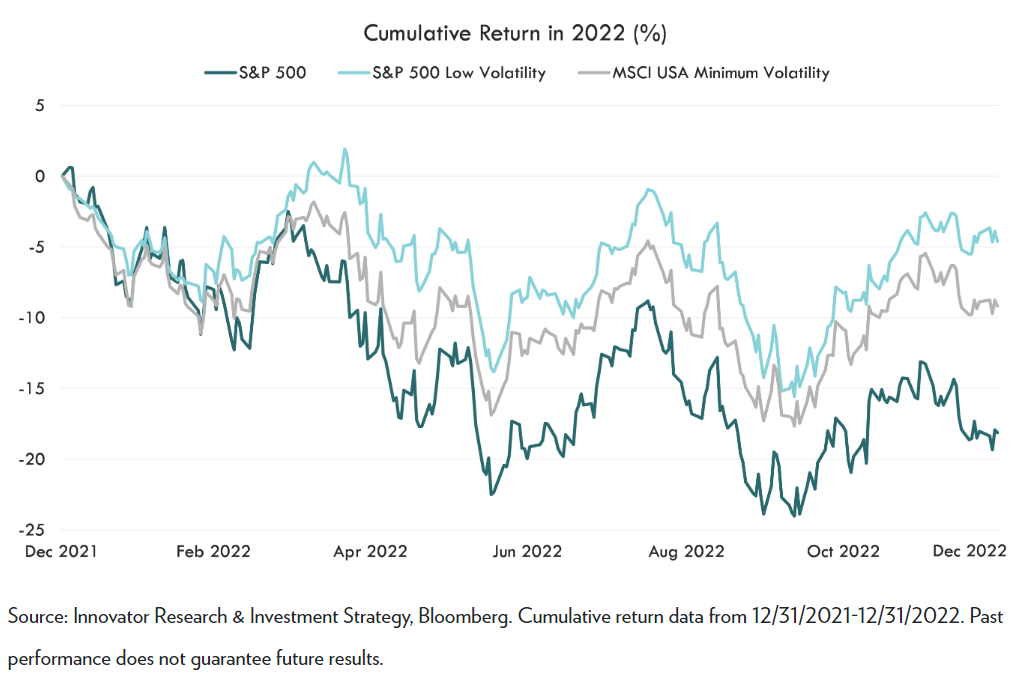

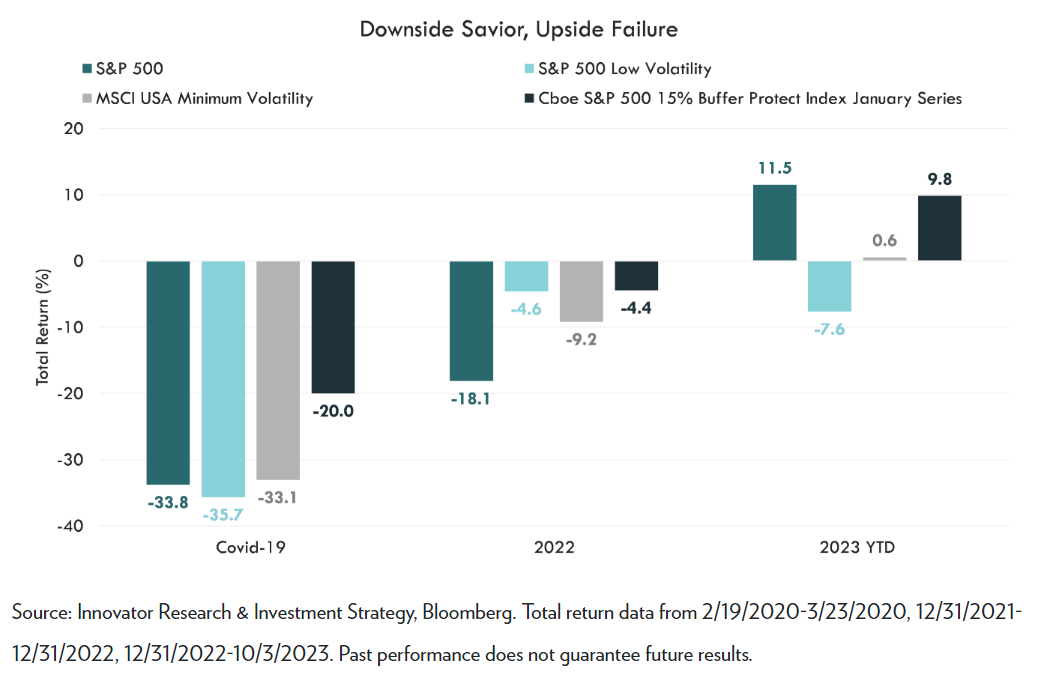

Rising rates and inflation acted as a wrecking ball to investment portfolios in 2022. U.S. equities and investment-grade fixed income witnessed double-digit declines, leaving investors scrambling for protection. Low volatility strategies experienced only a fraction of the losses compared to the S&P 500. The S&P 500 Low Volatility and MSCI USA Minimum Volatility Indices tracked the S&P 500 relatively closely until the second quarter when the S&P 500 fell over 16%1. Both low volatility strategies maintained their outperformance spread for the remainder of the year finishing at -4.6% and -9.2% vs. the S&P 500 at -18.1%2. How do these factor strategies work?

In 1976, Stephen A. Ross wrote a paper on arbitrage pricing theory that expanded on the Capital Asset Pricing Model, stating that various factors explain a stock’s return. Academia uncovered various factors as return drivers, like company’s size, volatility, value, quality and momentum. Factor-based investing involves systematically selecting a group of investments based these return drivers that are thought to be associated with higher returns, improved diversification, or reduced risk. While this approach has shown promise, it is not without its pitfalls, including the susceptibility to back-testing bias and the potential erosion of factor premiums over time.

You Never Know What You’re Going to Get

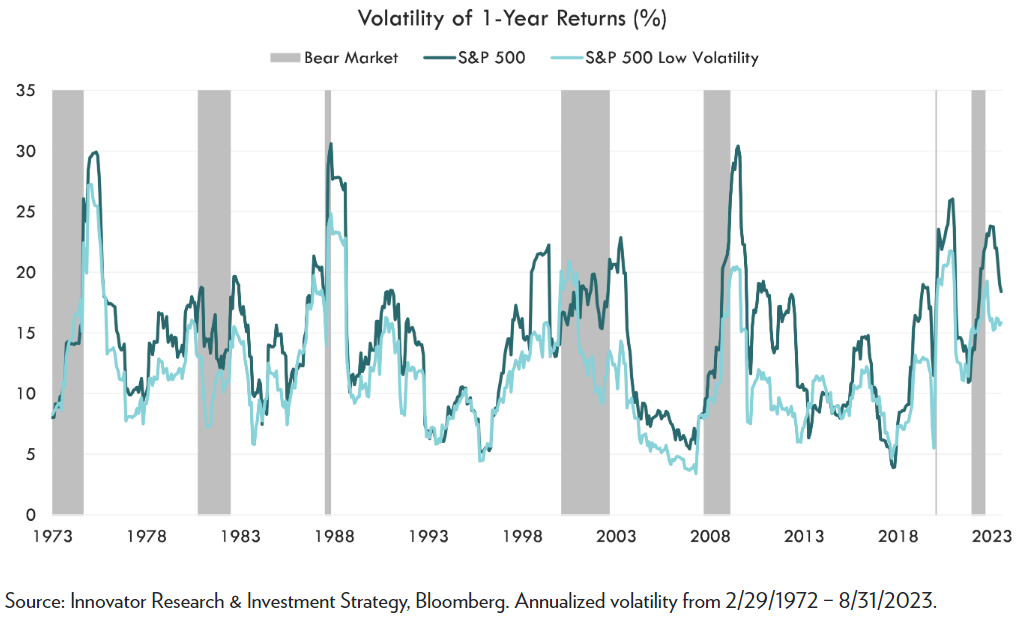

An investor that has experienced the global financial crisis might be hesitant to endure another major market downturn. Some might consider reducing risk through a greater allocation to bonds, while others may opt for a low volatility factor-based strategy. The S&P 500 Low Volatility Index selects 100 stocks from the S&P 500 demonstrating the lowest volatility on a trailing-one year time frame. The MSCI USA Minimum Volatility Index has a slightly different approach: the portfolio manager optimizes the weights to reach the minimum absolute volatility. However, both methodologies fall prey to a common caveat: past performance does not guarantee future results. Nothing guarantees that the least volatile stocks last year will be the least volatile stocks going forward. As shown in the chart below, the low volatility index has often reduced volatility compared to the S&P 500. However, investors have still assumed a large majority of the volatility in the time periods around bear markets. Just because the index selected the least volatile 100 stocks, doesn’t mean macroeconomic factors won’t drive the volatility in all stocks higher. We even see the low volatility index exceed the S&P 500 at during inflationary periods of the early 1970s, the beginning of the dot-com bubble, all of 2017, the beginning of the tightening cycle in 2022, and different spouts in between.

Lower Volatility Doesn’t Always Mean Better Performance

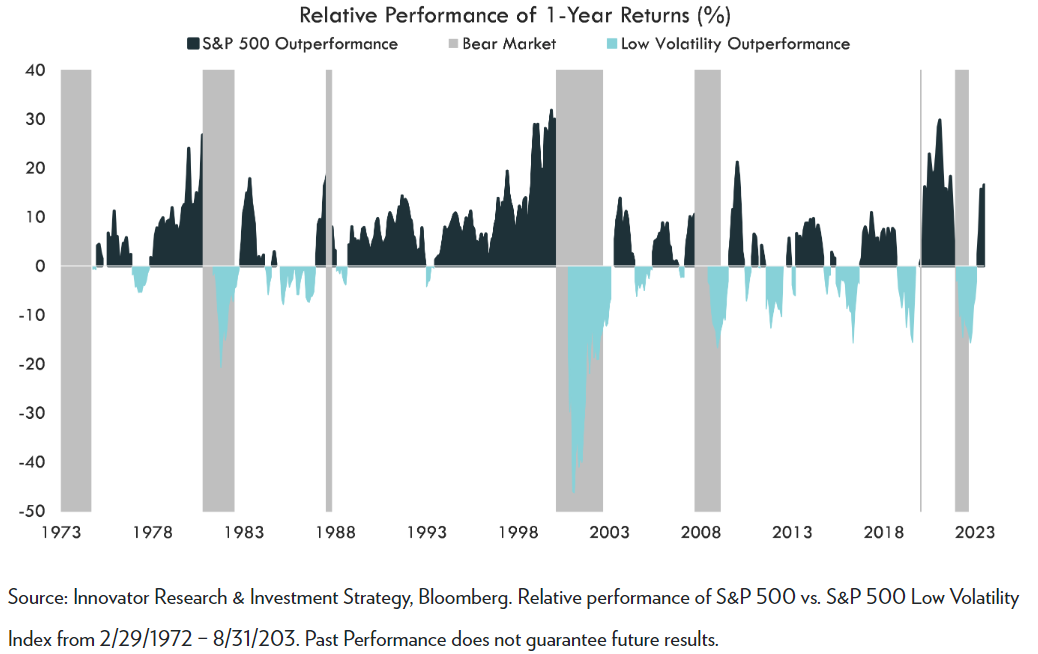

Most investors would expect that periods of heightened volatility would lead to greater drawdowns in stocks with higher sensitivity to market movements. While often true, this has not always been the case with the low volatility index. For example, the Covid-19 pandemic demonstrates where the low volatility index decreased volatility, but had returns fall below the S&P 500. In early 2008 during the Global Financial Crisis, we also saw lower volatility while the S&P 500 posted better performance. These instances underscore that a low volatility strategy is not infallible in mitigating market downturns. Moreover, one of its most significant drawbacks is its tendency to miss out on the full upside potential during bull markets. While low volatility has performed admirably during four of the seven bear markets examined, investing in the S&P 500 would have yielded superior returns in the other three bear markets and the majority of bull markets.

Bottom Line

Low volatility strategies appear to be an attractive option for guarding against market downturns. However, in practice, investors have no guarantee that today’s low volatility securities will be still be low in the future. For investors seeking to smooth out volatility while minimizing the unknowns, buffered equity strategies may offer a compelling alternative. Buffered equity strategies provide known levels of downside risk mitigation while allowing for upside participation to a predetermined cap. The chart below demonstrates how the CBOE S&P 500 15% Buffer Protect Index – January Series was able to mitigate downside risk in during the Covid-19 pandemic. In a sharp drawdown, the S&P 500 fell over 30%3. The low volatility index and minimum volatility index were almost even or worse while the CBOE S&P 500 15% Buffer Protect Index only fell 20%4. In 2022, both volatility strategies and the 15% buffer strategy meaningfully outperformed the S&P 500.

The double-digit drawdown across asset classes in 2022 led many investors to prepare for more of the same in 2023. Investors that continued to hold positions in volatility factor portfolios significantly trailed the S&P 500, which is up 11.5% year-to-date. Those in 15% buffer strategies have managed to capture about 85% of the S&P 5005.

Tom O'Shea is Director of Investment Strategy at Innovator. This material contains the current research and opinions of Tom O'Shea, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. The user of this information assumes the entire risk of any use made of the information provided herein. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of Innovator ETFs or any of its affiliates.

1. Source: Bloomberg. Data from 3/31/2022 -6/30/2022.

2. Source: Bloomberg. Data from 12/31/2021 -12/31/2022.

3. Source: Bloomberg. Data from 1/3/2022 – 3/23/2020.

4. Source: Bloomberg. Data from 1/3/2022 – 3/23/2020.

5. Source: Bloomberg. Data from 12/31/2022 – 10/3/2023.

The Cboe S&P 500 15% Buffer Protect Index Series are designed to provide target outcome returns to the US domestic stock market.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Innovator ETFs

Read more commentaries by Innovator ETFs