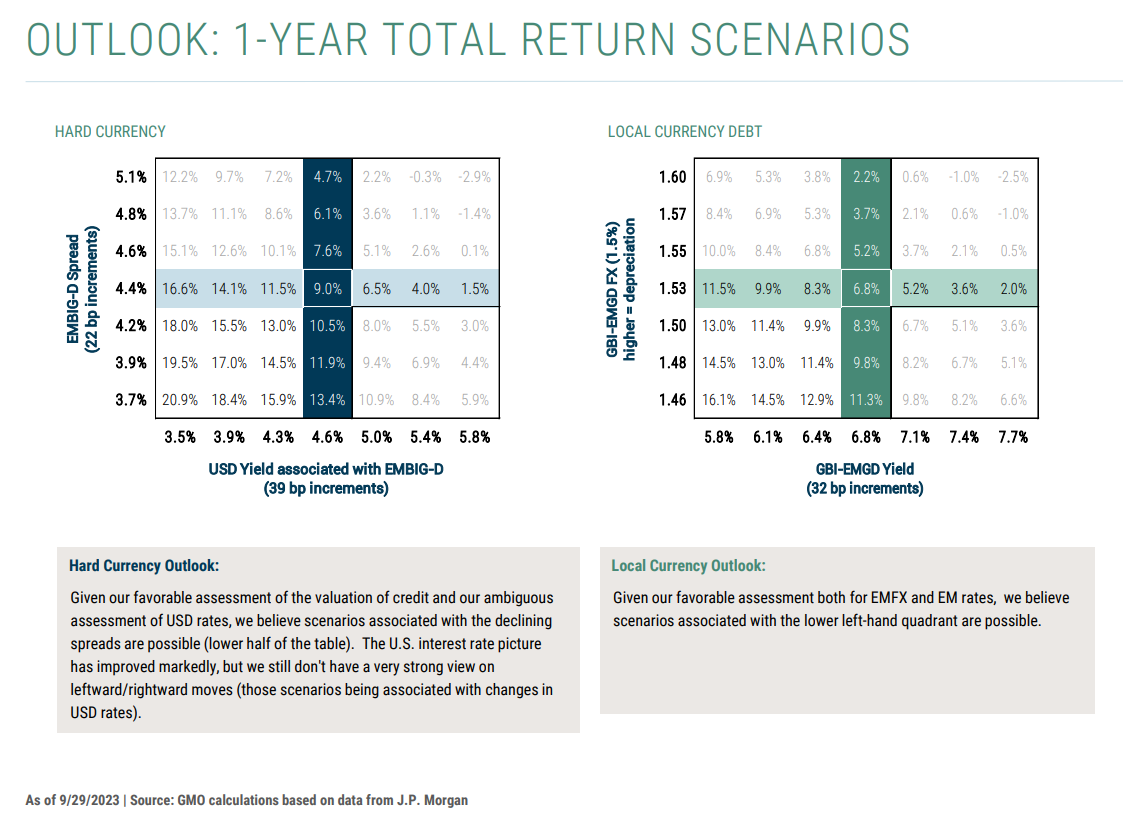

Our emerging market debt valuation metrics across all but the U.S. interest rate dimension remain unambiguously attractive. In our Quarterly Valuation Update, we provide our Q3 assessment.

Hard currency debt valuations:

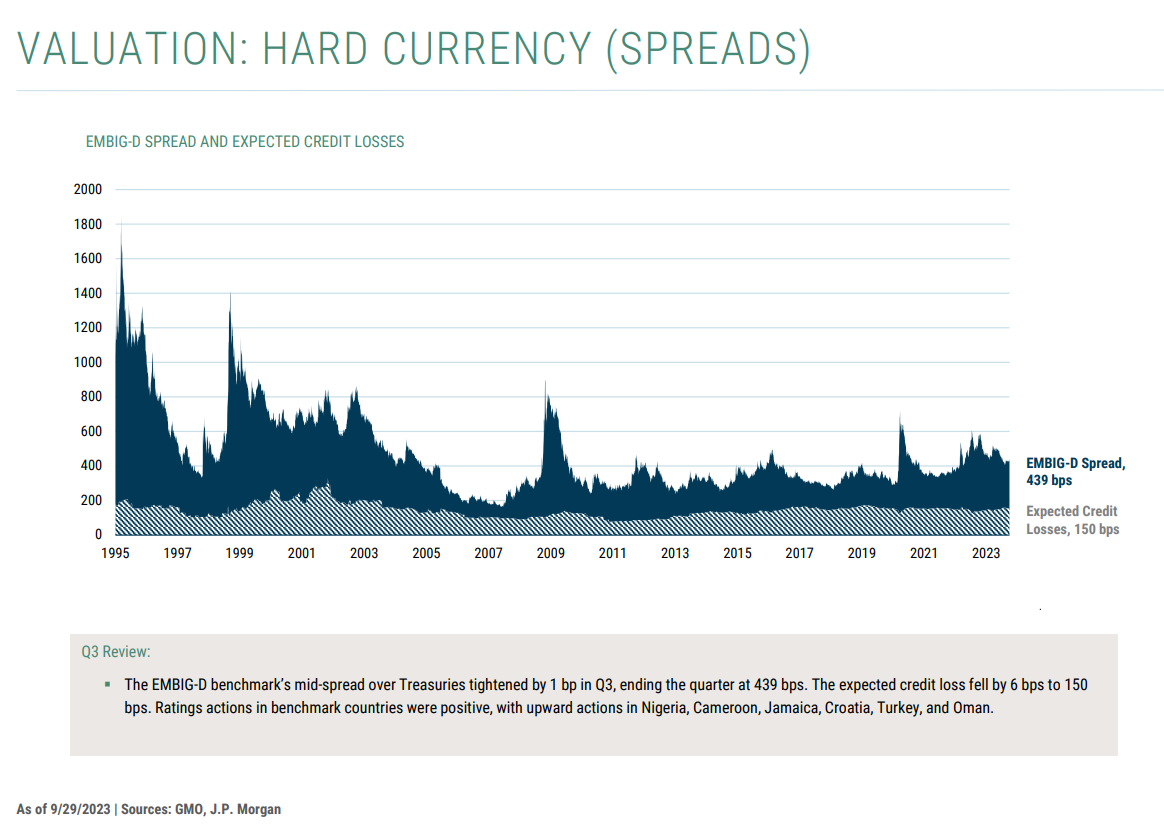

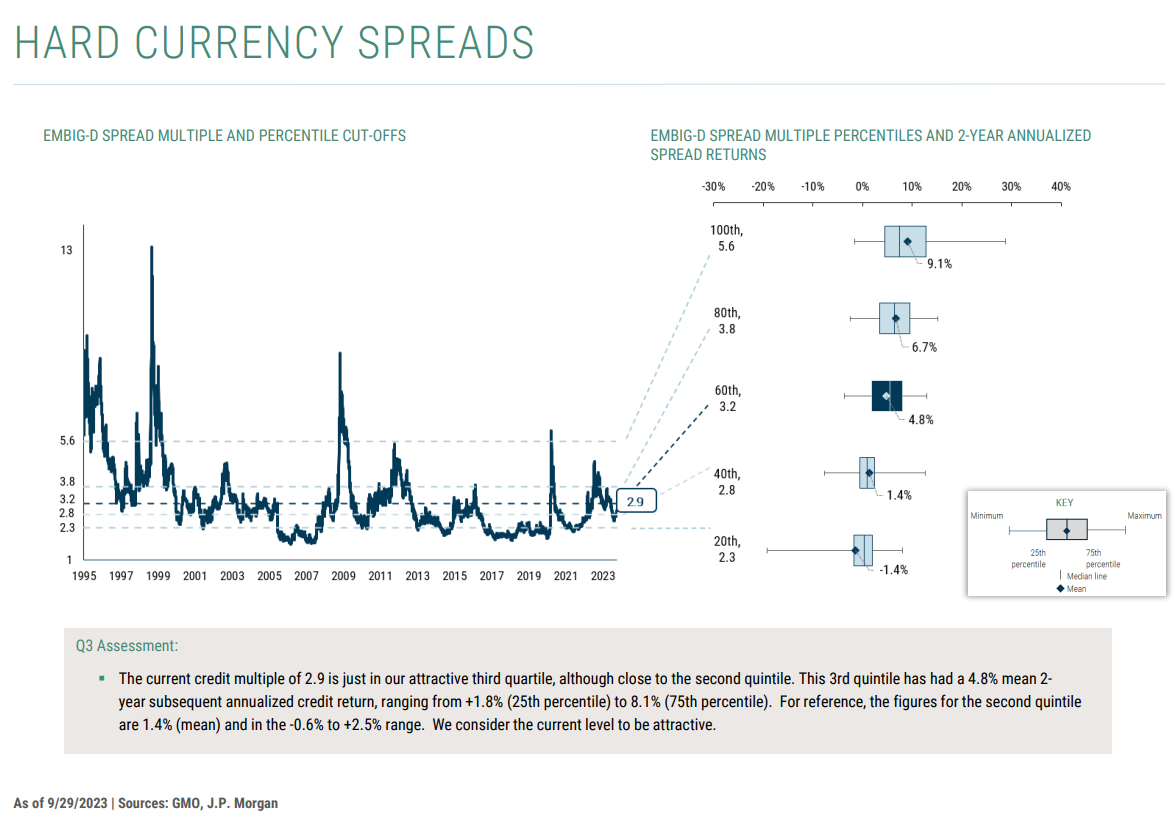

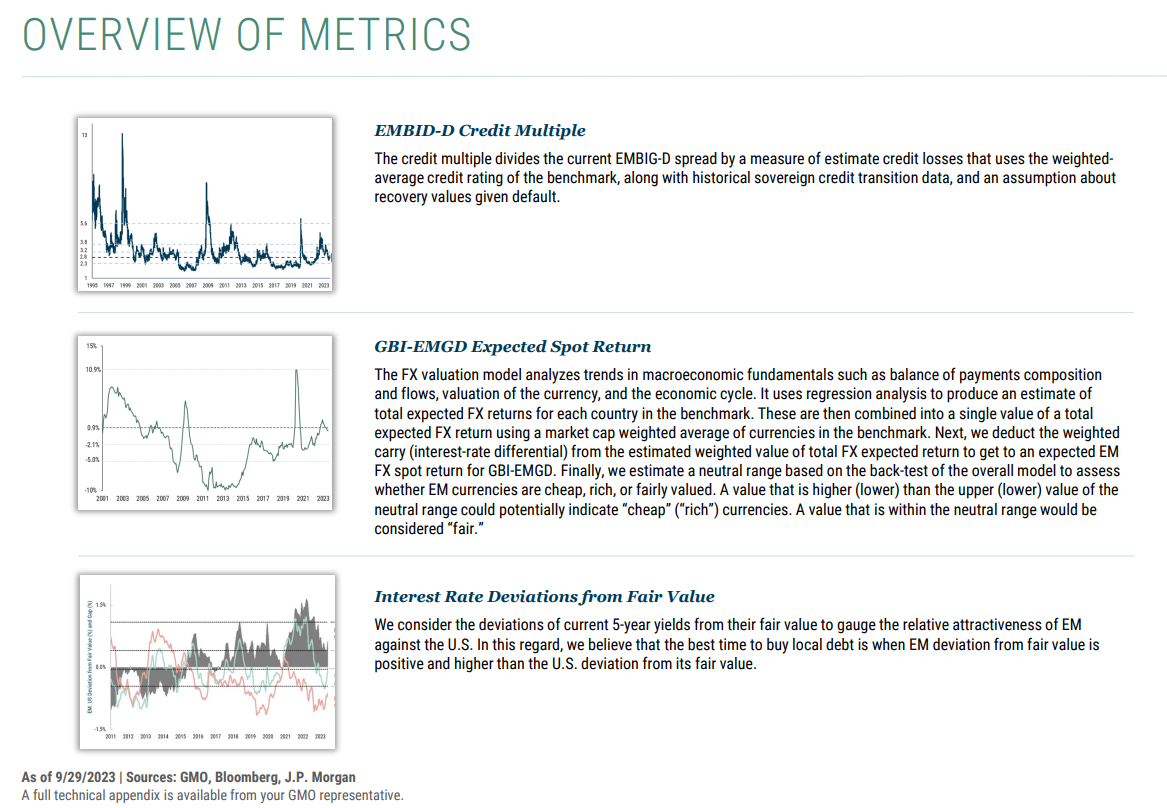

- EMBIG-D credit spreads tightened marginally. Expected credit losses also tightened, as ratings actions in benchmark countries were positive. The current credit multiple of 2.9 is in our third quintile of attractiveness, which is positive, although close to the second quintile. This quintile has had a +4.8% mean (+1.4% mean for the second quintile) 2-year subsequent annualized credit return (above the risk-free rate).

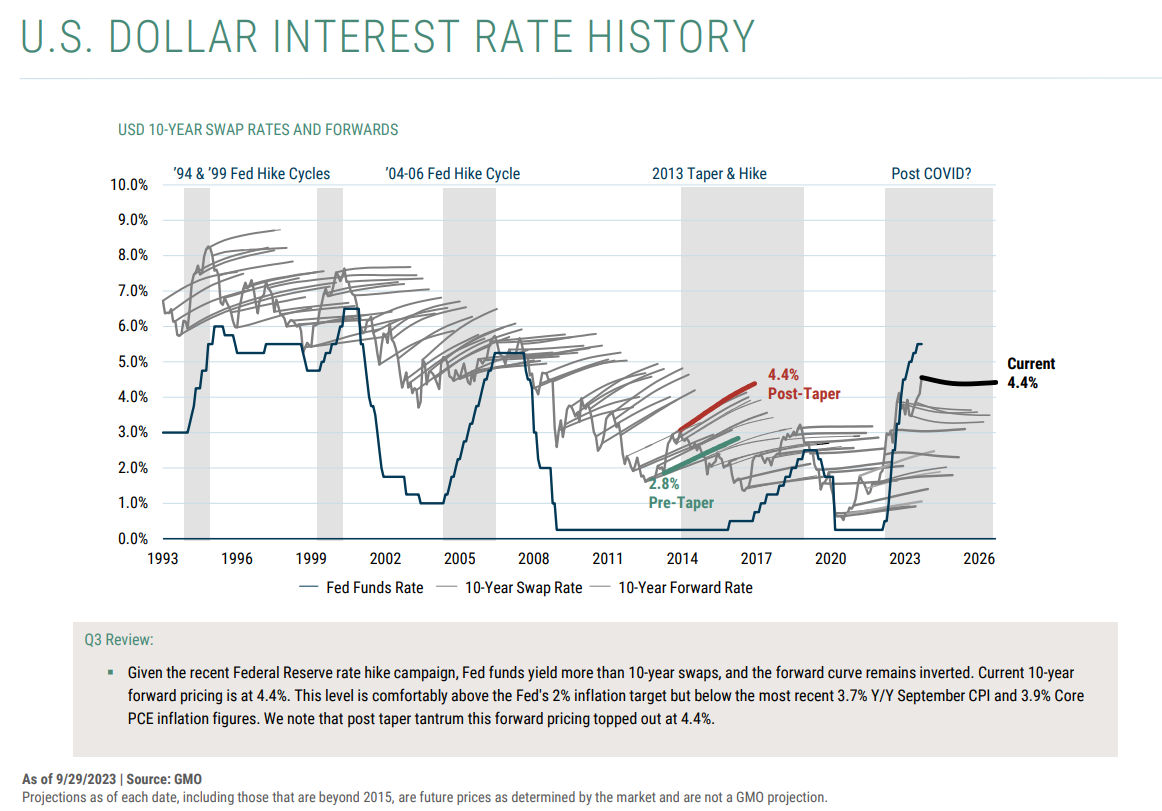

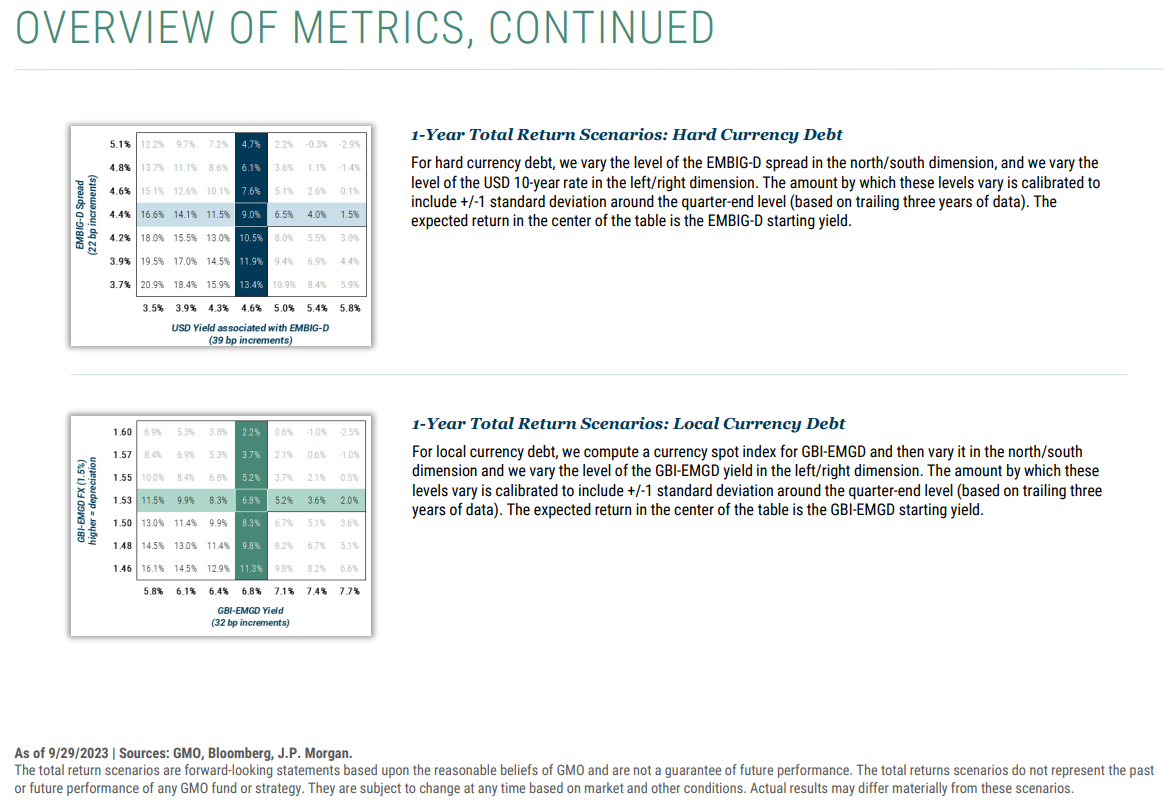

- As the Federal Reserve continues to raise U.S. interest rates, Fed funds yield more than 10-year swaps, and the forward curve remains inverted. The market is pricing 10-year rates to be 4.4% in three years' time, comfortably above the Fed's 2% inflation target but below the most recent 3.7% Y/Y September CPI and 3.9% Core PCE inflation figures. 4.4% is where the 3-year forward 10-year rate topped out after the "taper tantrum." We find this pricing somewhat ambiguous in generating a clear outlook, so we remain neutral.

Local currency debt valuations:

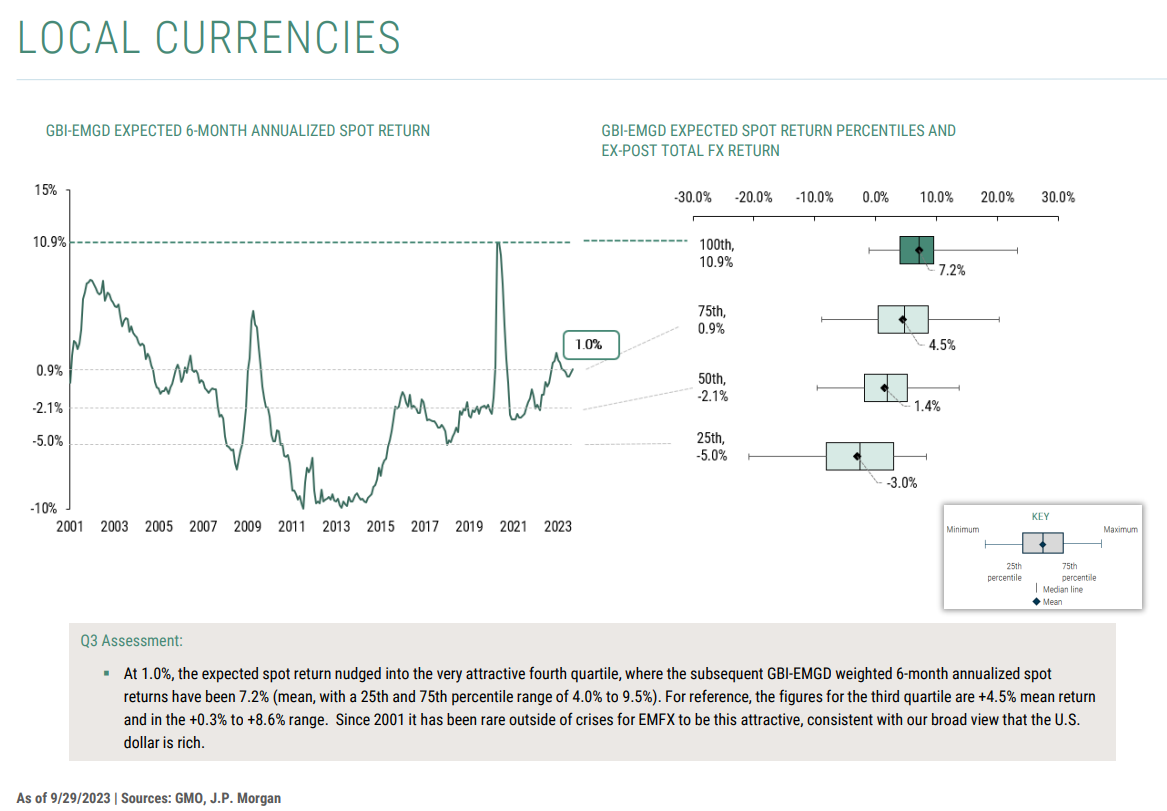

- In FX, our expected spot return indicator nudged into our very attractive valuation zone during the quarter, though still close to our third quartile, so our assessment remains attractive. At 1.0%, this is in our fourth quartile, where mean subsequent GBI-EMGD weighted spot returns have been +7.2%. Mean spot returns for the second quartile have been +4.5%.

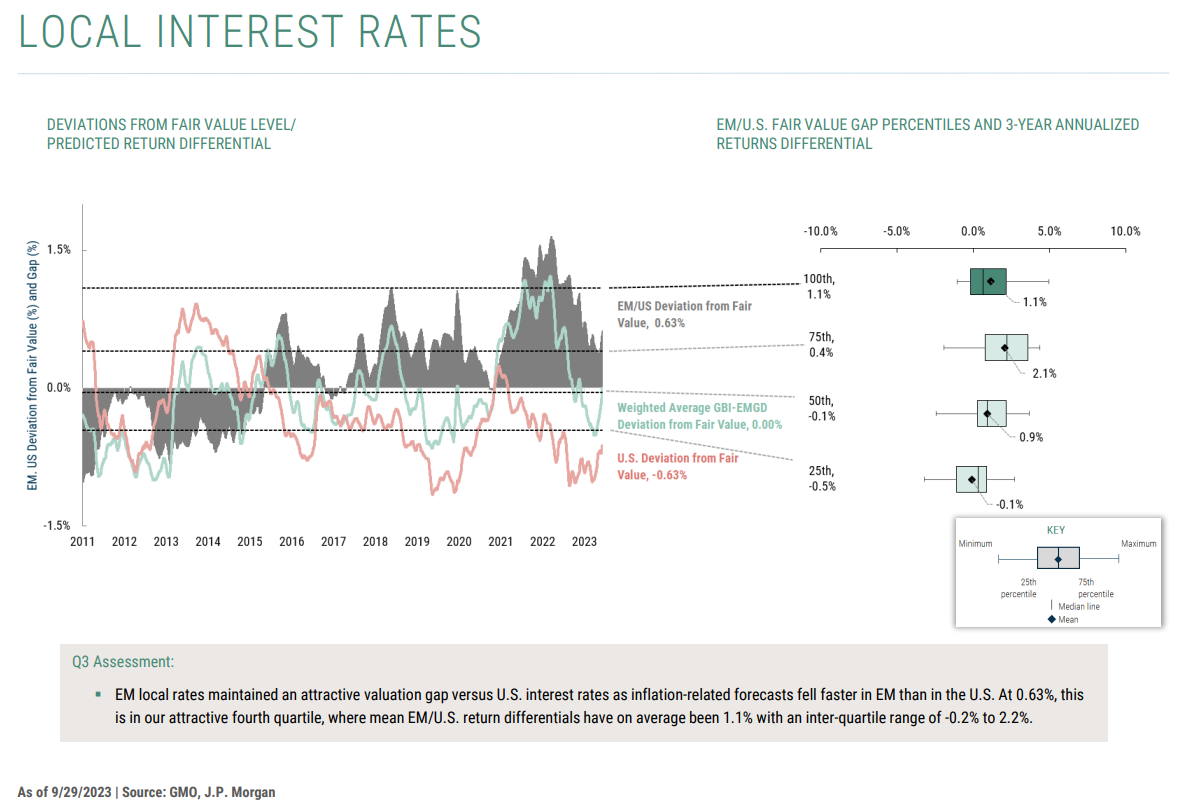

- EM local rates maintained an attractive valuation gap versus U.S. interest rates as inflation-related forecasts are falling faster in EM than in the U.S. At 0.63%, this is in our attractive fourth quartile, where the mean subsequent EM/U.S. return differential has been +1.1%.

Disclaimer:

The views expressed are the views and understanding of the Emerging Country Debt team through the period ending April 2023 and are subject to change at any time based on market and other conditions. While all reasonable effort has been taken to ensure accuracy, no representation or warranty for accuracy is provided nor should be assumed. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© GMO