Charting a Course in Choppier Waters

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey points

- Another wave of wage pressures? Despite progress on bringing down inflation from mid-2022 highs, data from online job postings suggests that wage pressures may be reaccelerating. Beneath the surface, growing divergence in wage gains across occupation categories may be adding a layer of complexity to the outlook for labor markets.

- Less stimulus to buoy growth? Alternative data measures point to a largely stable outlook for economic growth, suggesting that the likelihood of a near-term recession remains low. But the end of stimulus initiatives like student loan relief could be a headwind for consumer spending.

- Alpha over beta: If a recession is avoided, equity beta could still face bouts of pressure due to higher discount rates as the yield curve normalizes. But increased dispersion may create opportunities for skillful active managers to generate alpha through security selection.

At the start of 2023, consensus expectations were decisively negative and reflected a high likelihood of a recession. A string of positive economic surprises, along with excitement around artificial intelligence (“AI”), fueled strong equity market performance throughout the first half of the year. By July, a soft-landing scenario for the economy had become the dominant narrative priced into equity markets.

Now, market focus has started to shift towards concerns over policy rates remaining higher for longer. While avoiding a recession still appears achievable, alternative indicators suggest that economic surprises may become more two-sided and could pose challenges to equity investors in the months ahead. This also means that the ability to accurately forecast the direction of those surprises may be increasingly valuable for harnessing alpha opportunities as they surface. In this quarter’s Systematic Equity Outlook, we explore the data-driven insights shaping our views and potential opportunities to generate alpha amid a choppier environment for investors.

Another wave of wage pressures?

Easing inflationary pressures and resilient growth measures were among the string of positive developments that strengthened the case for a US soft-landing earlier this year. Despite acknowledging progress on inflation, the US Federal Reserve (“Fed”) continues to look for further evidence that policy is sufficiently restrictive to fully restore price stability. The Fed raised the bar for rate cuts and signaled they may keep rates higher for longer with the September Summary of Economic Projections (“SEP”), prompting a repricing of policy expectations.

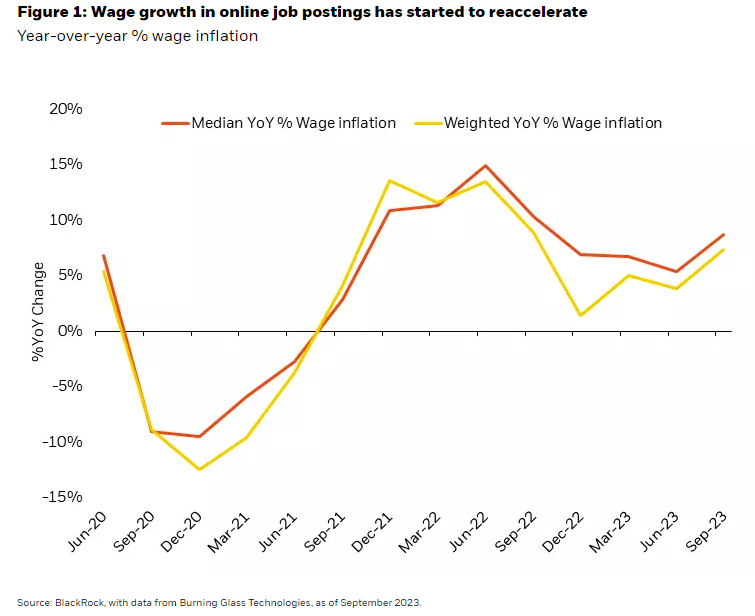

So can inflation continue to decline and provide the evidence needed to satisfy the Fed? To answer this question, we monitor a wide range of alternative datasets that provide a timely and granular view of inflation ahead of official reports. For example, we use data from online job postings to track wage inflation in real-time. Figure 1 shows a reacceleration of wage growth that we started to observe near the end of August. Some official data releases like the September Jobs Report and JOLTS data have since shown signs of increased labor market strength, and we expect other lagged measures to reflect higher wage growth in the coming months.

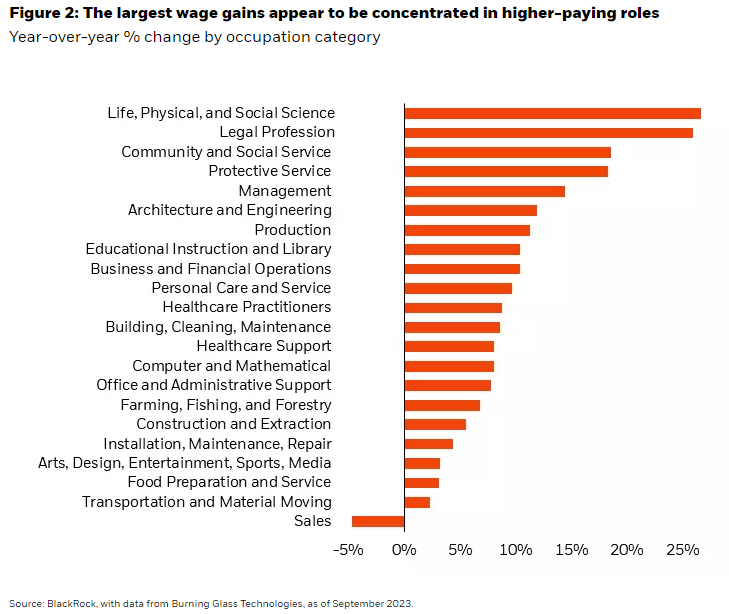

Beneath the surface of high-level wage increases, our job postings data also reveals an important shift in the distribution of wage inflation. Figure 2 shows that the largest wage gains are concentrated in higher-paying occupations while wage gains for lower-paying roles have been more muted. This suggests that declines in wage inflation highlighted in many aggregate measures may be masking a more nuanced story of ongoing tightness in the labor market. Our data shows that along with potentially reaccelerating in aggregate, the wage inflation picture is becoming increasingly complex with growing divergence across occupation types.

It’s important to note that the reacceleration of inflationary pressures appears to be confined to wages, as alternative data measures across several other price components are showing continued progress on disinflation. But given wages have been a key driver of stubborn services inflation (especially the so-called “super-core” core services ex-shelter inflation now running back above 5%), the Fed may feel added pressure to keep rates higher for longer.

Less stimulus to buy growth?

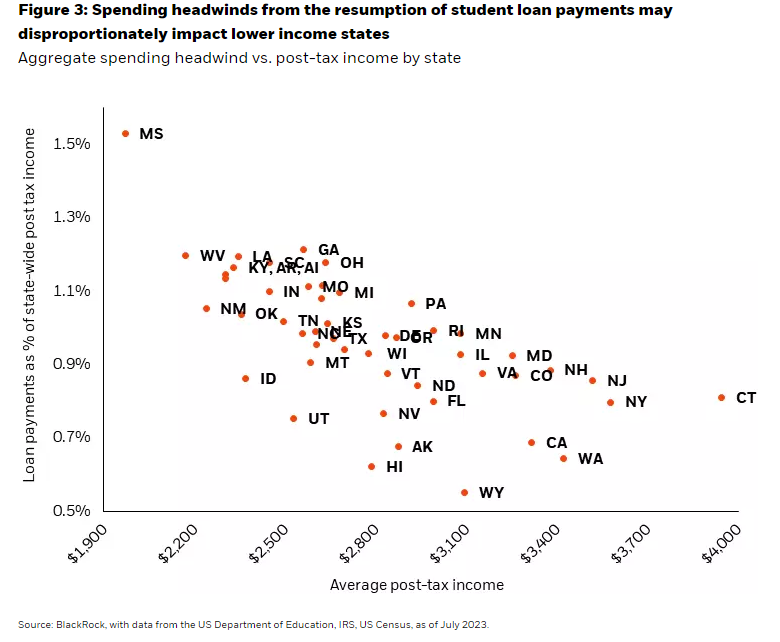

The strong job market is just one characteristic of the post-pandemic economy that’s contributed to resilient economic growth (and inflation) throughout the Fed’s hiking cycle. The unprecedented level of pandemic stimulus is another factor that’s bolstered household savings and supported strong consumer spending. Among a wide range of stimulus initiatives, student loan payments were paused from nearly the start of COVID-19 through September 2023.

Now, the resumption of student loan repayments could have the opposite effect on consumer activity. To gauge the magnitude of potential impact, we leverage US state-level student loan and income data. Figure 3 illustrates the aggregate student loan burden for each state, suggesting that the resumption of repayments will likely have the largest impact on household balance sheets in lower-income states.

The resumption of student loan payments also has the potential to drive increased labor participation as households face higher debt obligations. The aggregate participation rate of higher-educated cohorts remains below pre-COVID levels, suggesting that there’s room for more normalization to occur.

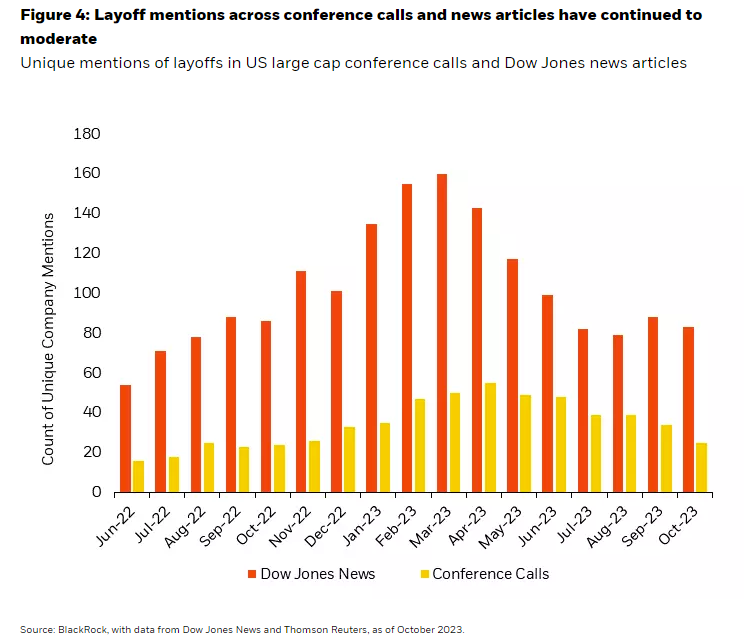

If this is the case, the unemployment rate may increase due to rising labor participation, as we saw in August. While higher unemployment is typically perceived as a negative for the economy, it may be viewed positively if it’s driven by an uptick in labor supply rather than broad-based layoffs. This is because it could relieve wage pressures by further restoring balance between labor supply and demand without requiring widespread job losses and economic pain. As shown in Figure 4, corporate layoff mentions across earnings calls and news articles have continued to moderate in recent months. The absence of severe layoffs is one of several indicators suggesting that economic growth in the US remains stable enough to avoid a recession in the near-term.

Equity market outlook: alpha over beta

In recent months, yield curve steepening has largely dominated equity returns, putting downward pressure on valuations given higher discount rates. Looking ahead, it’s possible that equity beta could face some additional headwinds even if a recession is avoided. This is because as the yield curve normalizes (un-inverts), further curve steepening would take place. Given that equity market pricing still reflects a largely optimistic growth outlook, the effect of higher discount rates could once again dominate broad equity performance in the absence of a significantly positive growth shock.

At the same time, the alpha opportunity set for equity investors has become increasingly compelling. Macroeconomic and market uncertainty is contributing to increased security dispersion, or divergence in returns across individual stocks. Active managers with the ability to rapidly uncover security selection insights and recalibrate portfolios may be well-positioned to harness alpha opportunities amid heightened volatility. This environment particularly enhances the opportunity set for managers who can invest both long and short, as they can exploit performance differences across stocks and target returns in the cross-section of markets with reduced dependence on overall market direction.

AI: rising tide recedes?

The AI theme is one area where we see cross-sectional opportunities emerging. In the first half of the year, AI could be thought of as a rising tide that lifted most boats, particularly in the mega-cap tech universe. Now, the surge in long-term rates has dampened the initial broad AI rally, making individual company characteristics a more relevant return driver. Some of the early AI leaders have differentiated themselves by starting to monetize the opportunity and delivering strong earnings results. On the opposite end of the spectrum, we’ve seen a reversal in the performance of certain companies who initially benefitted from the rising ride but haven’t shown evidence of sustained leadership potential.

It's worth noting that within BlackRock Systematic, we leverage AI and machine learning to help inform these security selection insights. One example of this is our use of transformer-based models to analyze unstructured text at scale, which provides a higher level of precision and accuracy than more traditional methods of analysis.

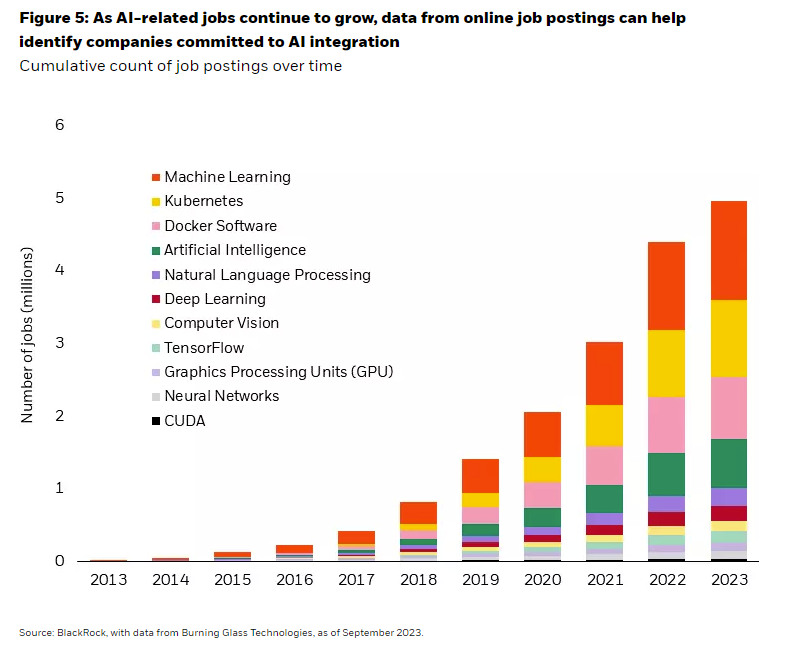

For example, we can analyze corporate earnings call transcripts from previous quarters throughout history to determine which companies were genuinely focused on AI long before the recent wave of hype. From a broader industry perspective, Figure 5 illustrates the acceleration of AI-related job postings across the economy. We can use the text from these online job postings to understand how companies across industries are integrating AI into their business models, and the potential enhancements to productivity and efficiency that may follow.

Conclusion

After a string of positive surprises in the first half of 2023, our outlook is becoming slightly more balanced as we look ahead. Wage pressures and consumer spending headwinds may be emerging, and equity markets could face periods of pressure from further curve steepening even if a soft-landing is achieved. Despite these risks, increased security dispersion is enhancing the opportunity set for active managers to generate alpha amid choppier waters.

This material is prepared by BlackRock and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of October 2023 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is intended for information purposes only and does not constitute investment advice or an offer or solicitation to purchase or sell in any securities, BlackRock funds or any investment strategy nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction.

Stock and bond values fluctuate in price so the value of your investment can go down depending upon market conditions. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments.

Index performance is shown for illustrative purposes only. Indexes are unmanaged and one cannot invest directly in an index.

Investing involves risk, including possible loss of principal.

©2023 BlackRock. Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates.. All other trademarks are the property of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All