Executive summary:

- Investment taxes can have a real impact on a portfolio

- Investors should be aware of four key tax realities they currently face

- Without a plan to manage these taxes, investors may find their ability to retire comfortably could be compromised

- The impact of these tax realities can be mitigated

It's important to stay realistic. Sounds obvious, like the advice mom or dad would give us in our younger years. But let's be real – Real-istic! Sometimes, distinguishing between what is real, and what is realistically attainable can be quite challenging. As such, many individuals – and in the context of this article, investors – are either un-realistic or think about things in an alternate reality. Taxes are real, and they have a real impact on portfolio wealth. For most investors, trying to sidestep the tax issue without a well-thought out strategy remains an elusive aspiration. Let's take a look at Four Tax Realities to see which taxes are real and have a real impact, and therefore where we should practically direct our attention.

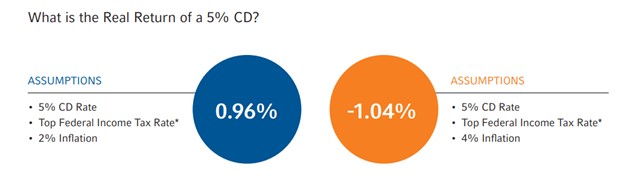

1. Most interest is taxed

Absolutely, interest income falls under the umbrella of taxable income. Even when it's labeled as "Tax Free Interest", there can still be some tax implications. You might be aware of this if you’re a financial professional, but here's the reality—many investors don't always know that interest from bank accounts, money market funds (MMFs), and certificates of deposit (CDs) are all taxable as income.

Moreover, most bond interest is taxable as income. Depending on the type of bond, various tax levels may come into play, and in some cases every tax level is involved. Consider these examples:

- Tax Free Municipal Bonds escape Federal income taxes and often local income taxes if the investor resides in the bond's state of issue.

- Treasury Bonds are exempt from state and local income taxes but are subject to Federal income taxes.

- Corporate Bonds’ income faces taxation at Federal, State, and Municipal levels

- Private Activity Municipal Bonds avoid Federal income taxes but may be subject to taxation under AMT rules – a potential concern for higher-income earners.

- Non-US bond interest is generally fully taxable in the U.S., with foreign taxes, withholding rules and additional record-keeping potentially entering the picture.

Since interest income is typically taxable, it's imperative to factor in the tax cost. In our current inflationary environment, it's equally vital to acknowledge the impact of inflation on the spending power of after-tax interest income.

Notes: CDs offer a fixed rate of return, and the interest and principal on CDs will generally be insured by the FDIC up to $250,000. Municipal bond fund investing is subject to the risks associated with debt securities including, but not limited to, credit, liquidity and interest rate risks. It may be adversely impacted by economic conditions, market fluctuation, and regulatory changes. * Based on maximum tax rate of 40.8% for Married Filing Jointly, including 3.8% Net Investment Income Tax.

2. Let's not forget capital gains taxes

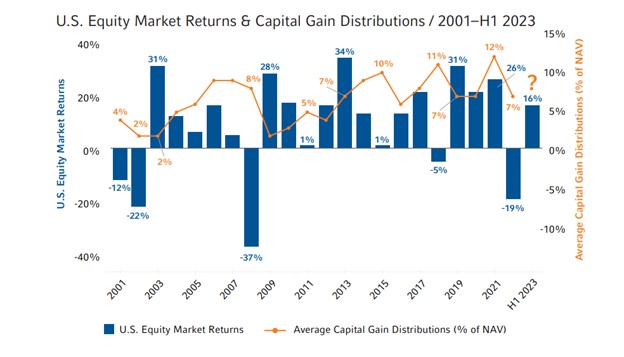

Every year, mutual funds add up their realized gains and losses for the fund's fiscal year. If the gains surpass losses, that excess is distributed to investors as a capital gain. This is an unavoidable reality. Mutual funds (including ETFs) are required to pay out 98.2% of net realized capital gains to shareholders. This happens every year, regardless of how the overall market has performed. That means capital gain distributions happen in both up and down markets.

Last year, the market was down and yet the vast majority of funds distributed capital gains. The distribution rates varied widely, but the average stood at 7%. So the question lingers: How substantial will the capital gain distribution be? Based on historical data, one thing seems almost certain – it's likely to more than zero and probably higher than many investors anticipate.

The chart below provides tangible evidence of this reality. Capital gains have been distributed by U.S. mutual funds in every year since 2001. And in that 20-year period there have been good years, bad years and meh years. The irony is that some of the largest distributions were made in some of the worst years in that period (for example, 2008, 2015 and 2018). It's important to take the opportunity to educate investors on the reality of capital gains and their tax implications. And fall is a really good time for those conversations.

Source: Morningstar Direct. U.S. stock market represented by Russell 3000® Index. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

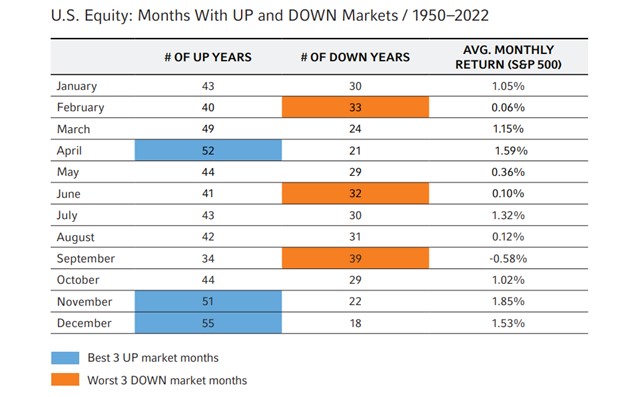

3. Tax-loss harvesting – All. Year. Long.

Consider this a reminder of the reality that procrastination rarely leads to success in most aspects of life. If you procrastinate planting a fruit tree, you’ll have to wait longer to harvest the fruit. Procrastinate in watering it, you’ll extend the wait for healthy fruit. Procrastinate in fertilizing it, you’ll wait longer for it to produce robust amounts of large, juicy fruit.

The same principle applies to managing a taxable investment portfolio. Waiting until year-end to "tax- loss harvest" will result in many missed opportunities. The "tax fruit" you eventually harvest may be meager and unsatisfying. The reality is that financial markets operate on distinct cycles, and as investors, we need to be vigilant at all times to reap the benefits. Harvesting losses is a crucial aspect of this process.

Tax-Loss Harvesting isn't something you reserve for the final months of the year when market conditions might be less favorable for such activities. As illustrated in the chart below, the last two months of the year historically yield some of the best average returns over a long period of time. It's far more prudent to cultivate these valuable tax assets throughout the year because the market can offer opportunities to create value at any time.

Source: FactSet, Morningstar Direct. As of 12/31/2022. U.S. Equity: S&P 500® Index. For months from January 1950 through January 1988, used price returns. February 1988 forward, used total returns. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

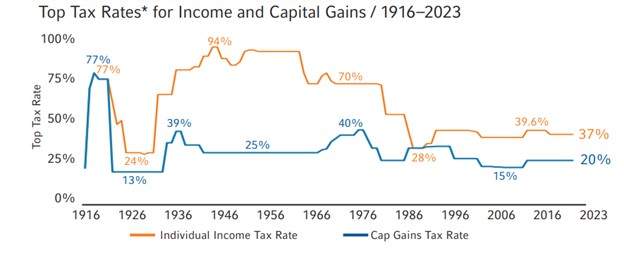

4. Tax rates are not likely to decline. The harsh reality.

Where do tax rates go from here? Up is the likely answer! Taxes don't have much room to decrease. Only a few times in history have taxes on investment gains been lower than where we are today. With the expiration of the 2017 Tax Cuts and Jobs Act (TCJA) on the horizon, it's probably prudent for investors to prepare for a new reality, one in which tax rates, including those on investment income, are likely to rise.

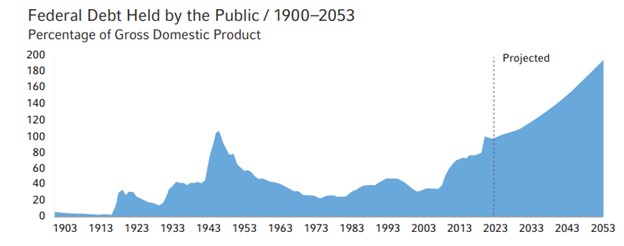

You might be wondering, "Why can't taxes go down further, and why should we expect an increase?" The answer lies in a simple but striking fact illustrated in the chart below. Currently, the Federal Debt outstanding is nearing parity with our Gross Domestic Product (GDP), meaning that we owe as much as we collectively produce in an entire year here in the U.S.!

Considering our anticipated and necessary expenditures and assuming the current rate of tax revenues, our national debt is projected to double within 30 years. By 2053, the U.S. is expected to be burdened with an outstanding debt that is nearly twice the size of its GDP. That's a lot of pennies! The pressing question is: how are we going to pay for this? The answer, as you might have guessed, lies in the inevitable reality of higher taxes.

What's real is real

Reality isn't always what we want it to be, but it's real. We really need to be real about it, especially when it comes to our investments, the way they are taxed, and how the combination of the two impacts our ability to retire comfortably.

That's the reality. Seeing them listed here may help you realize how much you as an advisor can do to demonstrate your value to your clients now and in the future. Request our Four Tax Realities flyer to share these insights with investors. Begin the conversation about the reality of taxes on their investment portfolio and the real ways you can help your clients minimize their impact.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Russell Investments

More Exchange-Traded Products Topics >