Equity Insights offers research and perspectives from Putnam’s equity team on market trends and opportunities.

Financial markets have changed dramatically since balanced portfolios were introduced to investors decades ago. As markets evolve and grow more complex, active management plays a greater role in the success of these strategies, which offer a mix of 60% equities and 40% fixed income. For many investors, this time-tested approach to asset allocation continues to be a solid offering. We believe investors can benefit from tenured portfolio managers who conduct rigorous research, continuously monitor a portfolio’s holdings and risk characteristics, and adjust its positioning for changing market environments.

The benefits of diversifying across asset classes

A portfolio that includes a mix of stocks and bonds is designed to manage volatility while delivering current income and consistent returns over time. Typically, there is relatively low correlation in equity and fixed income performance, so a combination of both can help dampen the impact of weakness in either asset class. The bond portion of the portfolio, which provides income potential, also serves as the ballast — aiming to bring a measure of stability and downside protection, particularly when equity markets are turbulent.

Last year’s challenges in perspective

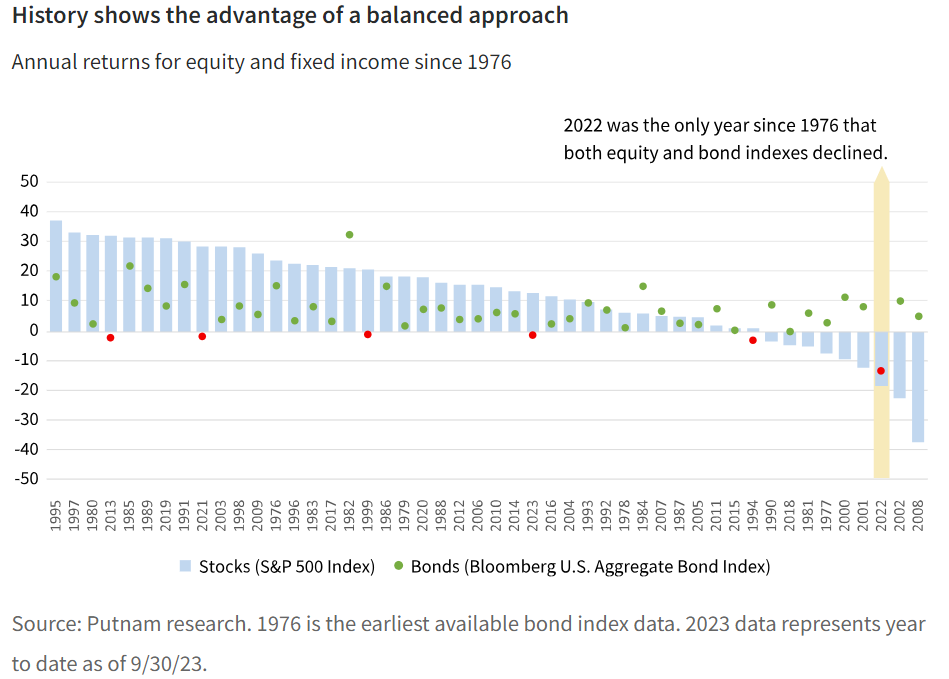

In 2022, balanced portfolios encountered challenging conditions, as equity and fixed income markets largely moved downward in tandem. Based on historical returns, the 2022 declines in both equities and fixed income appear to have been an anomaly. In the 47 years of available data for the Bloomberg U.S. Aggregate Bond Index, 2022 was the only instance in which both asset classes had an annual decline. In all other years, the returns of one asset class helped soften the impact of a decline in the other.

This is the case this year, as bonds are down while stocks have rebounded, and balanced fund returns have benefited from the equity market rally. And although the spike in bond yields in 2023 has been a headwind for fixed income markets, going forward, those higher yields can provide higher levels of income for investors in balanced portfolios.

Our research suggested that the 2022 decline in balanced portfolios presented an opportunity for investors. In an analysis of traditional 60/40 portfolio performance since 1926, Putnam analysts looked at how these portfolios performed following periods of underperformance similar to that of 2022. Their analysis found that in the nine instances when both stocks and bonds were trading below their 36-month moving averages, the average forward one-year return for a 60/40 portfolio was 19%. Also, stock returns were positive in only seven of the nine instances, yet the balanced portfolio returns were always positive. So far this year, a balanced approach has also been positive, with a year-to-date return of 7.34% for the George Putnam Blended Index as of 9/30/23.

A delayed rebound for fixed income markets

All in, the Bloomberg U.S. Aggregate Bond Index has delivered negative total returns for the past three years, making this the longest losing streak in nearly 50 years. We believe this sell-off has created an attractive yield environment for fixed-income investors. Investment-grade corporate bond yields are now greater than 6%, which surpasses the S&P 500 earnings yield for the first time in over a decade and represents a positive “real” yield.

At the same time, we believe the Federal Reserve is nearing the end of its monetary tightening cycle, which could benefit fixed income total returns going forward. In this environment, active portfolio managers can position the bond portion of a balanced portfolio to take advantage of a potential recovery. Historically, the last rate hike in a cycle has been a harbinger for declining U.S. Aggregate yields. This has occurred in both soft-landing environments such as 1994/1995, when inflation cooled, and during downturns that precipitated a Federal Reserve policy pivot.

Market uncertainty makes the case for balanced funds

With heightened economic uncertainty, inflationary concerns, and geopolitical tensions, we believe it is an attractive time to invest in balanced funds, thanks to uncorrelated asset class returns and the ballast provided by the fixed income portion of the portfolio.

With the George Putnam Balanced Fund, we offer tenured managers for both the equity and fixed income components of the portfolio. On the equity side, we have a team of sector experts investing across industries to create a sleeve of the portfolio that drives performance from stock picking while limiting factor exposures. It includes the best ideas from analysts across our U.S. equity research organization. For bonds, we assemble a mix of government and investment-grade securities, backed by the expertise of over 80 fixed income professionals across specialized teams.

"With heightened economic uncertainty, inflationary concerns, and geopolitical tensions, we believe it is an attractive time to invest in balanced funds."

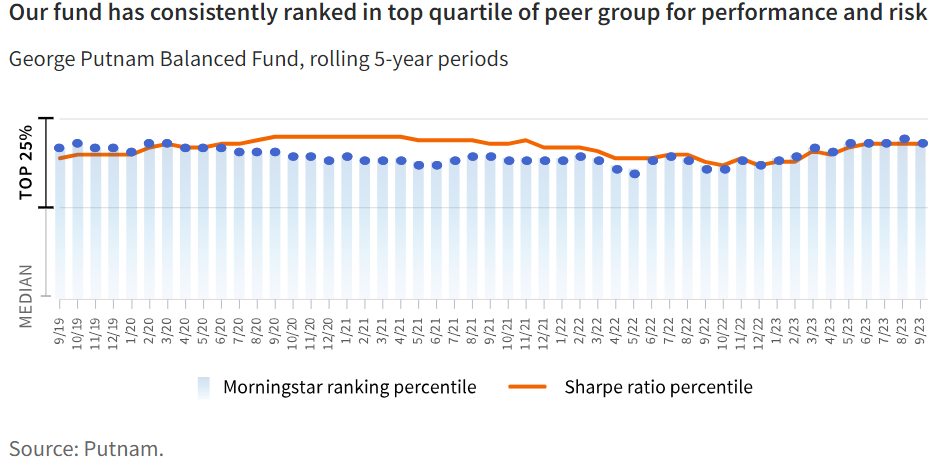

We believe the benefits of our active management are evident in the fund’s performance and risk profile. For every rolling 5-year period since 2019, the fund ranked in the top quartile of its peer group, in terms of both returns and Sharpe ratio — a measure of risk-adjusted performance.

As of 9/30/23, the fund has a five-star overall Morningstar rating out of 689 funds in the Moderate Allocation category based on total return. In all market environments, we remain focused on delivering alpha — above-benchmark investment returns — with lower volatility than the broader stock market and attractive income potential.

The George Putnam Blended Index is an unmanaged index administered by Putnam Management, 60% of which is the S&P 500 Index and 40% of which is the Bloomberg U.S. Aggregate Bond Index.

The views and opinions expressed are those of the authors, are subject to change with market conditions, and are not meant as investment advice.

Our investment techniques, analyses, and judgments may not produce the outcome we intend. The investments we select for the fund may not perform as well as other securities that we do not select for the fund. We, or the fund's other service providers, may experience disruptions or operating errors that could have a negative effect on the fund. You can lose money by investing in the fund.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Putnam

Read more commentaries by Putnam