Q3 Earnings Reveal Big Dispersion, Bigger Need for Stock Selection

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsQ3 earnings season had many familiar refrains relative to the year’s first two quarters. One difference was a return to positive earnings growth for the first time since Q3 2022. Still, the market wasn’t unanimously cheering the results. Fundamental Equities investor Carrie King looks at two areas where earnings dispersion may be creating opportunity for stock pickers.

Familiar refrains

Not unlike the first two quarters of the year, earnings for S&P 500 companies largely came in better than expected for Q3, with 62% of companies beating on sales (top line) and 83% on earnings (bottom line). And like the two quarters before, the market had a fairly muted reaction to the better-than-expected results, while the share prices of companies reporting misses were more deeply punished.

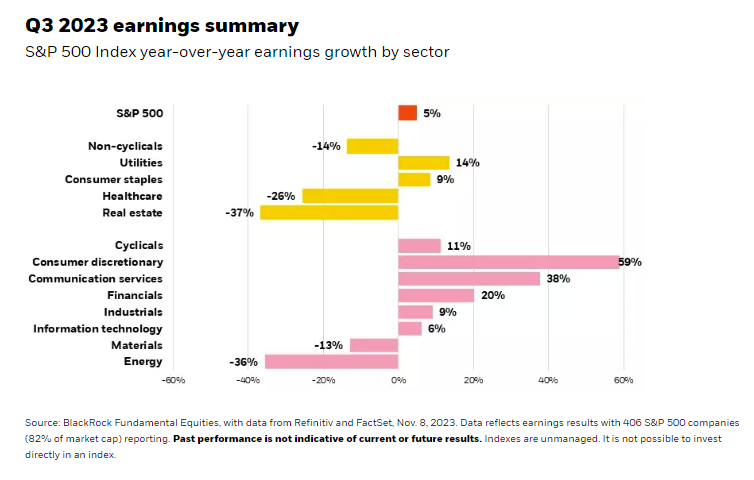

But this quarter was different for one key reason: The S&P 500 is set to notch its first quarter of earnings growth in a year, estimated at nearly 5%. That the index may have seen and surfaced from its earnings recession is positive, but the market cannot be painted with a broad brush.

As shown in the chart below, dispersion is evident across sectors, with cyclicals broadly doing better than non-cyclicals despite fears of an economic recession. We also see growing dispersion at the individual stock level and highlight two areas where this may be creating opportunity for stock pickers.

New consumer pains

The concerns we discussed last quarter around the fragility of the American consumer remain firmly in place. While both the discretionary and staples sectors posted positive year-over-year earnings growth, signs of consumer lethargy continue to mount and could cloud the future earnings picture. Company comments suggest the consumer is “pulling back,” “value-seeking” and growing more “discerning.” Some of this is manifesting in reduced pricing power, or the ability of companies to pass on higher input costs to the end buyer.

Fatigue is most pronounced among low-end consumers, and we are seeing this reflected in underwhelming performance from dollar stores. Results from financial institutions also exposed some cracks, showing an uptick in credit card delinquencies among lower-end consumers. While overall delinquencies are still below normal, we believe the direction of travel bears watching.

At the same time, the higher-income consumer is growing sheepish amid higher rates. We’re seeing this play out in the reporting of companies involved in such big-ticket discretionary items as boats and motorcycles, where higher rates are affecting affordability and deterring or delaying purchases.

Key takeaway: Sector-level results still look good, but it is worth noting that consumer discretionary is largely underpinned by some of the top mega-cap stocks that have powered the market this year. The opportunities and risks in consumer sectors are actually quite idiosyncratic. Omni-line business models, for example, may make some discounters more resilient than others. And we still see consumers prioritizing experiences over goods, with brighter rhetoric coming from the hotel, restaurant and leisure categories. As fundamental stock pickers, we are sharpening our pencils to pinpoint those companies best positioned to weather a potential consumption slowdown and protect share as buyers grow more guarded and discriminating in their spending.

Gains and losses in healthcare

Gains and losses in healthcare have entered a new dimension with the breakthrough in so-called GLP-1 agonists, a class of drugs used to treat diabetes and obesity. At the overall sector level, earnings were challenged for the quarter. Yet healthcare remains a favored area across our global Fundamental Equities platform for its defensive characteristics, long-term growth prospects amid aging populations, and record of innovation. We see ample opportunity to identify potential winners and losers as the new weight-loss therapies continue to make their impact known.

While makers of the GLP-1s have seen strong earnings and stock price appreciation, speculation around areas that might suffer because of their effectiveness is hurting other industries within healthcare and beyond.

Because these drugs have been shown to solve for many health issues, we’ve seen reactions in med tech such as insulin pumps, devices such as hip and knee replacements, sleep apnea machines, and even dialysis equipment as diseases that lead to kidney failure are addressed. The market has extrapolated other potential impacts, such as on snack and beverage companies that might see a decline in sales as the drugs curb not only appetite but demand for their products.

Key takeaway: GLP-1s are relatively new and some of the early reactions to their potential impact may be overdone ― or misconstrued. We see this creating opportunities not only in healthcare but elsewhere among consumer products companies. Our analysis found GLP-1s are unlikely to present a significant headwind for staples companies, with minimal earnings detraction across time even for those companies most exposed. Our healthcare team is also beginning to observe early indications of indirect beneficiaries of the new drugs, such as companies that might see increased volumes for injectors required to administer the medicines.

While the consumer sectors and healthcare offer just two examples, Q3 earnings confirmed to us that dispersion abounds in the market today. This points to the important role that fundamental analysis and skilled stock selection can play in driving portfolio outcomes.

Earnings figures cited herein are from BlackRock Fundamental Equities, with data from Refinitiv and FactSet. Figures are as of Nov. 8, 2023, with 406 companies (82% of S&P 500 market cap) reporting.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All