Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

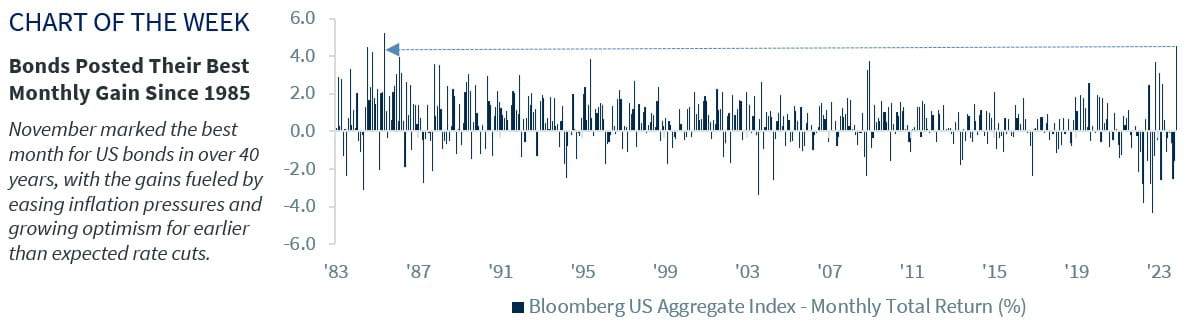

- Strong bond rally delivers best monthly return since 1985

- S&P 500 monthly gain was the seventh best in 30 years

- 60/40 portfolio posts second best monthly return in 30 years

November was a pivotal month for the financial markets. Despite concerns of higher for longer interest rates and 3Q GDP rising at its fastest pace (+5.2% YoY) in nearly two years, growing expectations of a Federal Reserve (Fed) pivot next year as the economy and inflation slow led to a broad-based rally across nearly all asset classes – ranging from Treasurys, to corporate credit, emerging markets and equities. In fact, November’s financial markets’ performance was one for the record books. The bad news: We do not expect the pace of these gains to continue. But the good news: We forecast that both equity and fixed income markets will move higher next year based on slowing inflation, Fed cuts, and a second half economic recovery. Here’s a quick recap of key market events in November:

- Fed’s tightening cycle is done | For much of 2023, the market has tried to anticipate a Fed pivot – only to be wrongfooted several times. However, sharply higher interest rates, cooling inflation pressures and moderating wages have the market convinced that the Fed’s current tightening cycle is over. While Fed officials want to maintain the flexibility to hike rates again should the progress on disinflation start to slow, comments from Fed Governor Waller (one of the more hawkish Fed members) this week was the strongest indication that a Fed pivot may not be too far away. In fact, the market is now pricing in that rate cuts could be coming – perhaps as soon as March 2024, with over 100 bps of rate cuts priced in by year-end 2024. With our economist only forecasting two interest rate cuts next year, the markets may have gotten ahead of themselves, which could lead to some near-term volatility.

- Bond rally gathers steam | After piercing the psychological 5.0% level just six weeks ago, the 10-year Treasury yield fell over 75 bps to an intra-day low of 4.25% during the month. The dramatic turnaround has been fueled by growing optimism that the Fed and other developed market central banks are done with their tightening cycles. The swift change in sentiment powered the Bloomberg US Aggregate Bond Index to a 4.5% increase MTD, on track for its best monthly gain in nearly forty years! Welcome news for bond investors who have been challenged by volatile swings in the market and the potential for a third consecutive year of losses. Other sectors of the bond market enjoyed strong returns, with investment grade corporates up 6.0% MTD, the biggest gain since December 2008, and munis posting their sixth best monthly return of 6.3% going back to 1980.** Looking forward, slowing job growth and further evidence of disinflation should drive yields modestly below 4.0% over the next 12 months.

- Equity market a standout | November is typically a strong month for the equity market from a seasonal perspective, as it is up 2.0% on average – the strongest month of the year over the last 30 years. This November was no exception, as the S&P 500 was up 9.1%, the best monthly performance since July 2022 and the seventh best performance over the last 30 years. Key drivers of the positive performance were resilient economic data and earnings, a sharp decline in interest rates and rising expectations for future Fed rate cuts. In fact, the more cyclical/interest rate sensitive areas were the strongest outperformers, as Info Tech, Consumer Discretionary, Real Estate and Financials all rallied over 10% during the month. Looking forward, given that S&P 500 earnings are likely to tread water in 2024, we expect the upward move in equity prices to be more muted than this year.

- Correlations remain positive | 2022 was a dismal year for the 60/40 portfolio, as positive correlations between both equities and bonds (with both sharply negative for the year), led the standard portfolio to its worst annual decline (-16%) since 2008. We have often said that we hoped that correlations would remain positive, as our expectation for resilient equity performance combined with falling interest rates would boost both equity and bond performance. And with the 12-month rolling correlation of equity and bonds at nearly the highest level since 1997, the strong gains this month led the 60/40 portfolio to its second-best monthly performance over the last 30 years. With equities and bonds expected to post positive performance over the next 12 months, positive correlations should boost the performance of the 60/40 portfolio in 2024.