“Cultivate the habit of being grateful for every good thing that comes to you, and to give thanks continuously.” —Ralph Waldo Emerson

There Is A Lot To Be Thankful For

In the middle of October, Fed Chairman Jerome Powell stated, “Inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal.” I guess much has changed since then as just six weeks later the tone has altered significantly. “We’re getting what we wanted to get, we now have the ability to move carefully…we are well into restrictive territory,” suggesting that rates have peaked. Given the disruptions to the economy during the last few years of tight monetary policy, one might think that we got what we needed rather than what we wanted. The markets have taken a long and winding road but have reached the favorable destination of slow and steady economic growth, rising corporate profits, full employment, and moderating inflation.

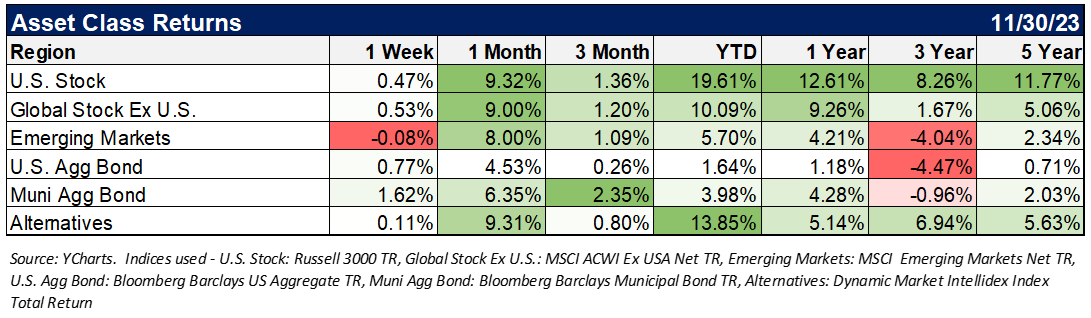

The S&P 500 approached the levels last seen at the end of July, prior to the 3-month downturn from August to October. However, all major equity indexes had strong Novembers with International Equities, Emerging Market Equities, and Small Cap stocks, all returning 8-9%. Bond investors were also rewarded, as the benchmark 10-year Treasury yield, which touched 5% in October, fell 63 basis points to end November at 4.37%, its lowest yield since early September. The 2-year Treasury rate which seemingly topped out around Powell’s comments in mid-October settled in at 4.73%. Gold continued to climb, passing $2,000/oz, while Crude Oil prices softened, and the Dollar was steady at a three-month low.

There was even a nice uptick in the Consumer Confidence Index last week, with the November reading bouncing back after three straight monthly declines. The consumer is still relatively healthy even with all the inflation seen in the last few years.

How Could The Consumer Still Be Healthy?

According to the Consumer Financial Protection Bureau (CFPB), pandemic relief improved many consumers’ finances in 2020 and 2021, but in 2022 financial stability and health deteriorated across a range of measures. Using survey data, we saw 2023 consumers were still on average somewhat better off financially than they were in 2019. While most families still live paycheck to paycheck and would have challenges should there be a disruption to income, there is still substantial liquidity in the system.

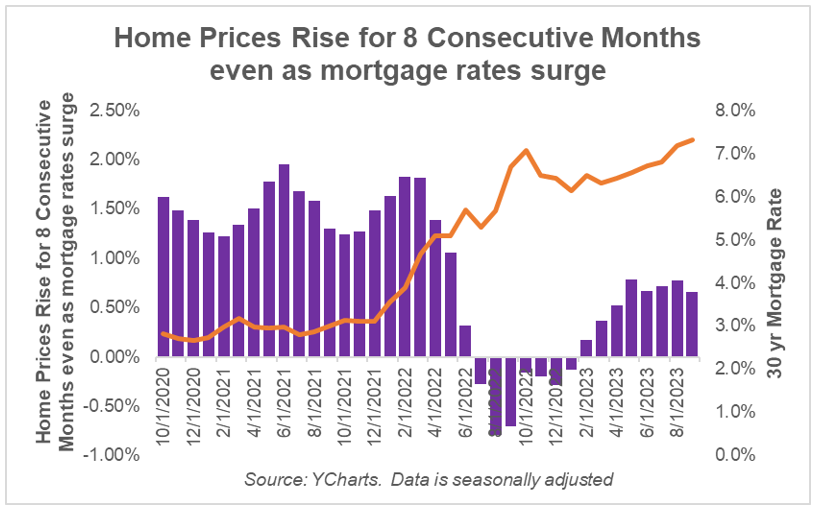

Also of note, many people point to housing costs such as mortgage rates not seen in over 20 years and sky-high home prices, as evidence that consumers might be in trouble. After all, Shelter is the largest percentage of the Consumer Price Index, outpacing food and transportation combined, and tends to make up roughly 30% of consumer spending.

However, it is important to recognize that fewer than 4% of American households bought a home in the last year. For the majority of families who either don’t have a mortgage or have a fixed-rate mortgage, the surge in mortgage rates and home prices has had no impact on their financial position. Today’s housing crunch, unlike the bursting housing bust of the mid-2000s, does not appear to be of a magnitude that will put the U.S. economy into a recession.

We are continuing to monitor consumer sentiment and consumer health. So long as the consumer is relatively healthy and continues to spend money. After all, consumption is 68% of GDP. If we want the economy to grow (and markets to rise), it’s critically important that consumption is strong.

Happy Holidays from the Investments Desk at Journey Strategic Wealth

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Journey Strategic Wealth

Read more commentaries by Journey Strategic Wealth