November update

- Municipal bonds posted historic total returns of 5.90% in November.

- Rallying interest rates led the way, while strong demand aided outperformance versus Treasuries.

- Although valuations are tight, favorable seasonal dynamics still warrant optimism into the new year.

Market overview

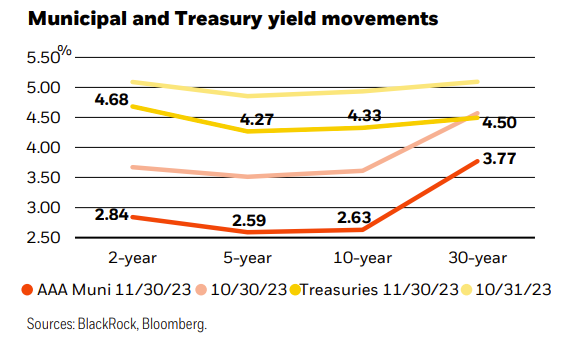

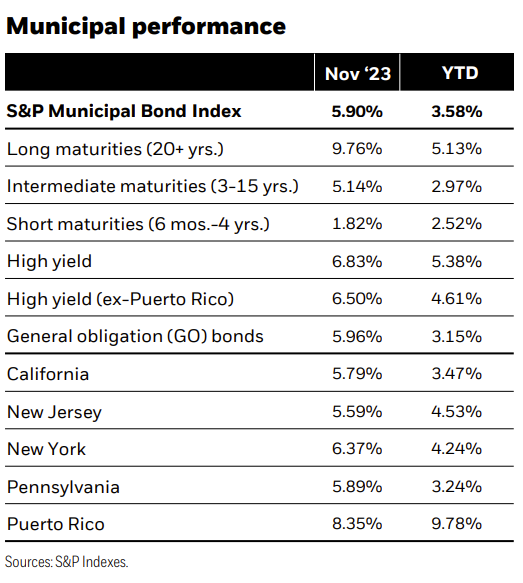

Municipal bonds posted their strongest month in over 40 years in November. Falling interest rates provided leadership as slowing economic growth, moderating inflation, and a second-consecutive pause from the Federal Reserve prompted more dovish forward monetary policy expectations and pushed 10-year Treasury yields lower by 61bps. The asset class further outperformed comparable Treasuries, as investors positioned for improved demand and a dearth of supply into the new year. The S&P Municipal Bond Index returned a whopping 5.90%, bringing the yearto-date total return to 3.58%. Longer-duration bonds (i.e., more sensitive to interest rate changes), lower-rated credits, and the tobacco, Puerto Rico, hospital, and housing sectors performed best.

Issuance remained elevated in November at $36 billion, 11% above the five-year average, bringing the year-to-date total to $337 billion. However, supply was easily absorbed as investors raced to lock in high absolute yields as opportunities dwindle. As a result, deals were oversubscribed 6.3 times on average, above the year-todate average of 4.2 times. At the same time, mutual fund outflows slowed as performance rebounded. Late in the month, the asset class posted its first weekly inflow since August — notable given that November typically contends with sizable tax-loss harvesting.

Although the trajectory of the rally is likely unsustainable, particularly given tight valuations, we believe municipals still provide opportunity. The asset class is entering a favorable seasonal period and will likely benefit from limited supply over the next few months. In addition, an improved outlook for fixed income should strengthen demand and promote more consistent inflows in 2024.

Strategy insights

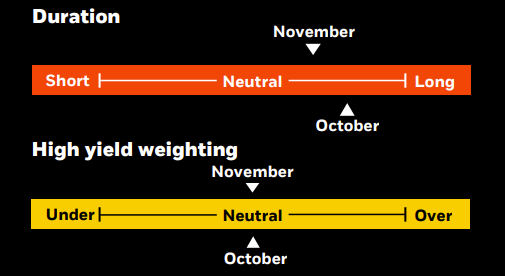

We have shifted back to a neutral duration posture overall. We prefer an up-in-quality bias and remain selective in noninvestment grade. We advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15-20-year part of the curve. We favor higher coupon structures.

Overweight

- Essential-service revenue bonds

- Select highest-quality state and local issuers with broadest tax support

- Flagship universities

- Select issuers in the high yield space

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

- Senior living and long-term care facilities in saturated markets

- Lower-rated private universities

- Stand-alone and rural health providers

Credit headlines

The outlook for U.S. states remains ‘stable’ in 2024, according to Moody’s. In a report published last week, Moody’s cited states’ “proactive fiscal management” and “strong reserves” in its assessment. The agency expects aggregate state reserves to decline but remain near historically high levels, as spending pressures grow while federal pandemic aid ends. As a testament to states’ overall solid credit fundamentals, 47 of the 49 states rated by Moody’s are in the highest ‘Aaa’ and ‘Aa’ rating categories, while two (New Jersey and Illinois) are in the ‘A’ category. Five states have ‘positive’ outlooks, while 43 states are ‘stable’. The only state with a negative outlook is the largest – California (‘Aa2’) – due principally to a significant decline in revenue receipts, although reserves are still projected to remain high in 2024.

It was recently announced that the city membership of Utah Associated Municipal Power Systems opted for a strategic “off ramp” exiting what was to be the first small modular nuclear reactor (SMR) project built in the U.S. The so-called Carbon Free Power Project is a partnership with NuScale Power and was to be built on the site of the Department of Energy’s Idaho National Lab. NuScale’s SMR technology received final design approval by the Nuclear Regulatory Commission in 2022, but is currently uneconomic, relative to renewable, storage, and natural gas-fired options, to be part of a serious solution for clean energy (2025) and carbon-free (2050) goals. Budget cost escalation from $4.1 billion to $9.3 billion has rendered it too expensive. Given the recent troubled history of nuclear construction, namely Summer and Vogtle plants, the market would be skeptical in funding nuclear projects unless the federal government was a substantial financial partner. President Biden’s Inflation Reduction Act, with $369 billion in climate provisions, incentivizes advanced nuclear deployment, but away from the obvious single-site project risk, the related production or investment tax credits are a tricky hurdle for tax-exempt public power.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of December 7, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© BlackRock

Read more commentaries by BlackRock