Highlights

- In the same way that a swimmer can make the biggest splash by jumping off of a higher diving board, so too fixed income asset returns can appear prospectively most attractive after a prolonged back up in rates. We think the current environment presents fixed income investors with a profoundly compelling opportunity.

- Indeed, as we reach the end of this hiking cycle, we think the opportunities embedded in bond market dynamics, and the economic backdrop, are truly historic for investors.

- In brief, we anticipate that the yield curve is likely to eventually steepen, with a rally led by the front-end and belly, and the back end of the curve remaining more range bound.

- Therefore, we think it makes sense to utilize high-quality, front-end, assets as a ballast for portfolios, and we are increasingly comfortable taking on intermediate duration risk (in the belly of the curve) and credit risk, in order to participate in upside as well.

- In this commentary, we look at the economic backdrop, which we believe strongly argues for a period of more stable rates, followed by lower rates later in 2024. Then, we will examine some of the technical factors that we believe can be supportive to the bond markets, even in the face of worrisome government bond issuance.

You can only make a big splash off of a high diving board

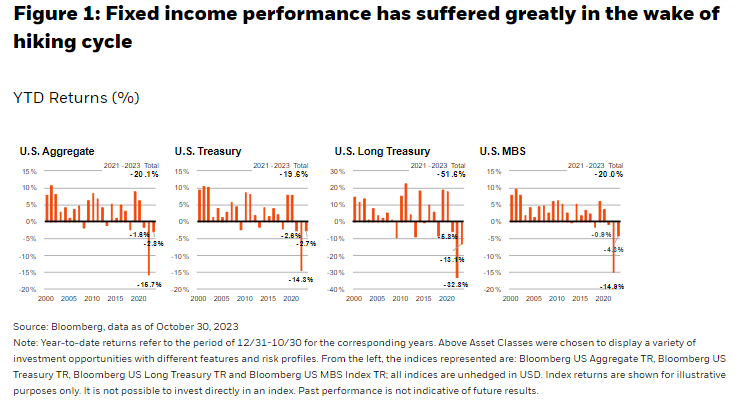

It is a well-known axiom that while financial markets are clearly related to the economy, they are not equivalent things. That proposition could be seen amply well from 2021 to 2023, when the economy displayed remarkable resilience to the most rapid policy rate hiking cycle undertaken by the Federal Reserve in decades, while the bond markets foundered on the back of high inflation and rapid rate hikes. Indeed, 2022 was the worst year on record for the return performance of the 10-Year U.S. Treasury bond, with 2021 and 2023 coming in close to the worst annual result as well. Since 1900, there has been only one other time that witnessed three consecutive years of negative performance in bond markets (the late-1950s), but that instance was not close to as bad as the present one. Further, the magnitude and pervasiveness of this bond market rout is truly astounding, as it has dramatically impacted the most heavily owned and traded segments of the fixed income markets (see Figure 1). Still, it is also well known that a swimmer can make the biggest splash (in positive return generation) off of a high diving board (after witnessing a dramatic back up in rates), so we think the current environment presents fixed income investors with a profoundly compelling opportunity going forward.

Indeed, as we reach the end of this hiking cycle, we think the opportunities embedded in bond market dynamics, and the economic backdrop, are truly historic for investors. In brief, we anticipate that the yield curve is likely to eventually steepen, with a rally led by the front-end and belly, and the back end of the curve remaining more range bound. Therefore, we think it makes sense to utilize high-quality, front-end, assets as a ballast for portfolios (as carry/volatility ratios appear attractive), and we are increasingly comfortable taking on intermediate duration risk (in the belly of the curve) and credit risk, in order to participate in potential upside as well. We will next look at the economic backdrop, which we believe strongly argues for a period of more stable rates, followed by lower rates later in 2024. Then, we will examine some of the technical factors that we believe can be supportive to the bond markets, even in the face of worrisome government bond issuance.

2024/2025 data will be different, with rates having backed up dramatically

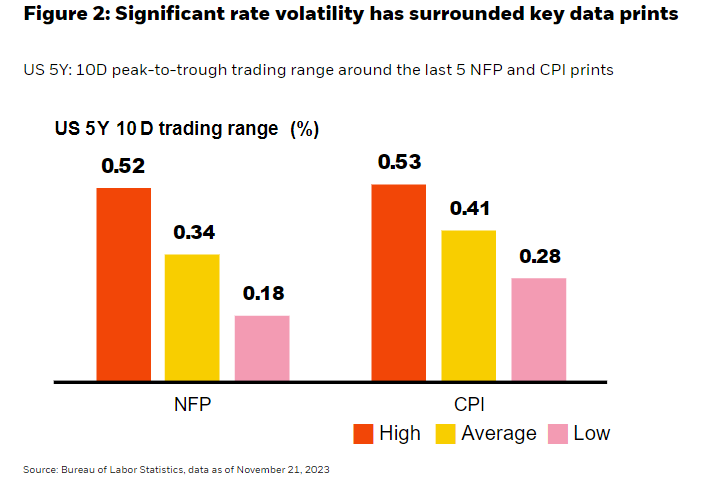

Recent months have witnessed extreme data dependency by markets, particularly around the CPI and NFP data prints, in which this short-term data can cause wild swings in sentiment, market prices and forecasts. Then, often, the extreme moves in either direction are quickly unwound, without much more clarity over the direction of the economy. In fact, the 5-Year U.S. Treasury has traded, incredibly, in a 20 to 50 basis point (bps) peak-to-trough range in the 10 days surrounding the past several CPI and NFP prints (see Figure 2). All of this excitement belies the fact that (broadly speaking) inflation has been making a durable downward trend, while at the same time the labor market has remained remarkably resilient. Obviously, all these market gyrations relate to the attempts at understanding the Federal Reserve policy reaction function, but we think the Fed is likely on hold for the time being, as it awaits more data, with the possibility of a discussion of rate cuts entering the dialogue over the coming few months.

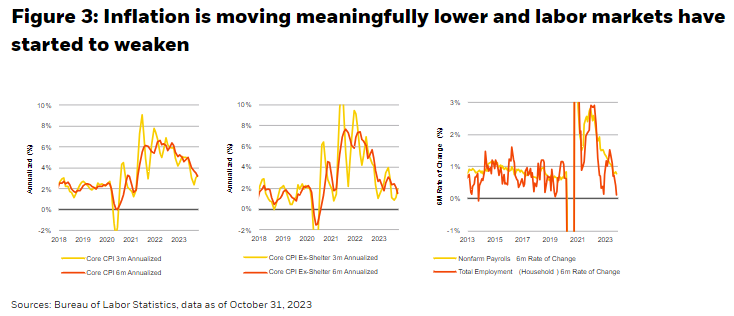

With the progress we are seeing on the inflation front, the question for Fed officials will shift from ‘how high should policy rates be’ to more of ‘how long should rates be kept at restrictive levels’ before bringing yields more in line with these lower inflation readings? As such, the Fed will certainly be paying close attention to the data feedback it is receiving from the more cyclical, and rate-sensitive, segments of the economy, such as regional banking institutions and the commercial real estate sector, which have come under immense pressure. In fact, Chair Powell even referenced the fact that the housing market has essentially frozen up in his November Fed policy meeting press conference. Thus, with inflation coming down meaningfully, the labor markets beginning to display signs of slowing, and certain rate-sensitive regions of the economy under considerable pressure, we think it is very likely that the extended rate pause the Fed undertakes now will eventually turn to rate cutting in 2024 (see Figure 3).

Bond market backdrop incredibly compelling

And maybe with an opportunity to generate a big splash (positive return generation)

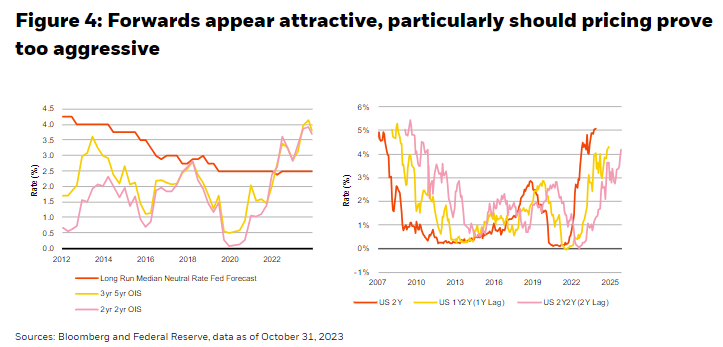

As the economic data is set to moderate and the Fed begins to take a more balanced (and eventually easier) policy stance in 2024, the backdrop for bonds appears extraordinarily compelling. Historically speaking, fixed income assets have tended to perform very well after the Fed has paused its rate hiking, when the Fed Funds rate has been greater than the rate of inflation, and when the yield curve has begun to de-invert. Whether looking at current yields relative to volatility, or at the pricing of forward markets, today’s starting point offers the opposite of what we saw heading into 2021, which creates the potential for very generous returns in the years ahead. Indeed, if we look at the forwards market pricing, after a decade, they today reside well above the Fed’s median estimate of the neutral rate, and history has often shown us that end-of-cycle pricing can prove to be too aggressive (see Figure 4).

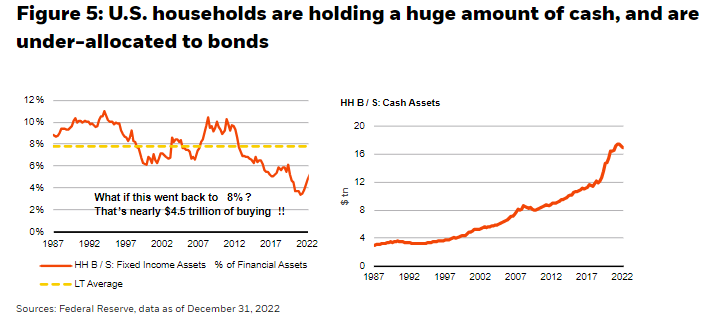

Moreover, from a supply/demand technical standpoint, while the massive amount of U.S. Treasury supply is quite concerning over the longer run, we think that there are good reasons to believe that the household sector in the U.S. (which has largely allocated to money market funds in the past year) might move more capital into bonds to lock in these attractive yields in the year ahead. In fact, U.S. households are sitting on around $17 trillion in cash assets at this point, and investors are historically under-allocated to fixed income at a time when the asset class appears to be set for a period of attractive returns (see Figure 5). So, all of this raises the question of how to best take advantage of the current environment in fixed income, and reallocate capital in the year ahead to attempt to achieve solid risk-adjusted returns for a portfolio.

The macro set-up for fixed income is strong, but how should one invest?

Investors have a rare opportunity to lock in historically high yields as the Fed reaches the end of its hiking cycle. We highlight three key strategies for investors who are ready to make the move out of cash and into fixed income securities:

1. Step out of cash: Cash has been a solid allocation while the Federal Reserve was hiking rates, but if market pricing is correct, policy rates could move lower next year. This means that the seemingly “risk-free” cash trade suddenly has a risk: reinvestment risk. By moving from cash to short duration bond strategies, investors can seek exposure to rates at the front-end of the curve where yields are currently the highest.

2. Ladder your bonds: By holding to maturity, investors can seek yield over the life of the investment. And by laddering the portfolio, investors can structure cash flows to match liquidity needs, avoiding sales ahead of maturity that might crystallize mark-to-market losses.

3. Follow us, Jump in: There is an abundance of yield in today’s fixed income markets, providing opportunities for active management outside of the Bloomberg Aggregate Bond Index. Investors can optimize portfolios to maximize key priorities whether it be capital preservation, equity diversification or income. Many clients want to outsource investment decision-making to a manager who can navigate the shifting landscape.

Investing involves risks, including possible loss of principal. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks may be heightened for investments in emerging markets. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks may be heightened for investments in emerging markets.

Shares of ETFs trade at market price, which may be greater or less than net asset value. The iShares® iBonds® ETFs (“Funds”) will terminate within the month and year in each Fund’s name. An investment in the Fund(s) is not guaranteed, and an investor may experience losses and/or tax consequences, including near or at the termination date. In the final months of each Fund's operation, its portfolio will transition to cash and cash-like instruments. As a result, its yield will tend to move toward prevailing money market rates, and may be lower than the yields of the bonds previously held by the Fund and lower than prevailing yields in the bond market.

The BlackRock Short Duration Bond ETF will invest in privately issued securities that have not been registered under the Securities Act of 1933 and as a result are subject to legal restrictions on resale. Privately issued securities are not traded on established markets and may be illiquid, difficult to value and subject to wide fluctuations in value. Delay or difficulty in selling such securities may result in a loss to the BlackRock Short Maturity Bond ETF. The Fund may invest in asset-backed (“ABS”) and mortgage-backed securities (“MBS”) which are subject to credit, prepayment and extension risk, and react differently to changes in interest rates than other bonds. Small movements in interest rates may quickly reduce the value of certain ABS and MBS.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of November 30, 2023, and may change as subsequent conditions vary. The information and opinions contained in this commentary are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents.

This commentary may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

© 2023 BlackRock, Inc. All rights reserved. BLACKROCK, iRETIRE, ALADDIN, CoRI, iBONDS and iSHARES are trademarks of BlackRock, Inc. or its affiliates in the United States and elsewhere. All other marks are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

More ETF Topics >