The Big Questions as We Begin a New Year

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits"As you go through life, there are thousands of little forks in the road, and there are a few really big forks – those moments of reckoning, moments of truth."

Lee Iacocca

Our business model has changed

As some of you will be aware, we have recently changed our business model, following an approach from a client who encouraged us to invest directly in listed securities on the back of the same seven megatrends that have formed the backbone of the fund investments we have made for years.

To cut a long story short, it all resulted in the launch of a new investment vehicle, which I cannot mention by name in this context, as it is only open to professional clients as defined by the FCA. If you click here, you can see how the regulator defines the term “professional client”, and whether you qualify as one. Allow me to provide a bit of guidance: if you work in the financial industry, zoom in on COBS 3.5.2 (per se professional clients). If you don’t, zoom in on COBS 3.5.3 (elective professional clients). That will make it a great deal easier.

The January format going forward

As long-term readers will be aware, for years, I have started the January letter with Saxo Bank’s (so-called) Outrageous Predictions. Saxo Bank mixes tail-risk forecasting with a healthy dose of fun; however, our new business model has made me realise it is time to move on.

Going forward, the January letters will continue to be somewhat different from other Absolute Return Letters. Overall, they will set the tone for the year to come, i.e. I will discuss what we, as a team, think will be the most important issues to focus on in the months to come.

The way it is going to work in practice is that, in December, I will ask the team what they think are the most important questions/issues to be addressed, assuming a time horizon of 12 months. I will then seek to answer those questions in the January letter. This year, four questions stand out:

1. Will 2024 be a good year to invest in risk-assets?

2. What is the outlook for commodities?

3. Will green stocks continue to rebound after having had a tough year?

4. How do you expect equities to react, if interest rates do not come down as implied by the bond market?

Let’s go straight to the first question.

Q1: Will 2024 be a good year to invest in risk assets?

The short answer to that question is that it depends on the behaviour of the US consumer. What do I mean by that? Here in Europe, analysts are largely aligned. Virtually everybody agrees that significant parts of the eurozone are already knocking on the door to recession. So is the UK, i.e. European financial markets are probably already discounting one.

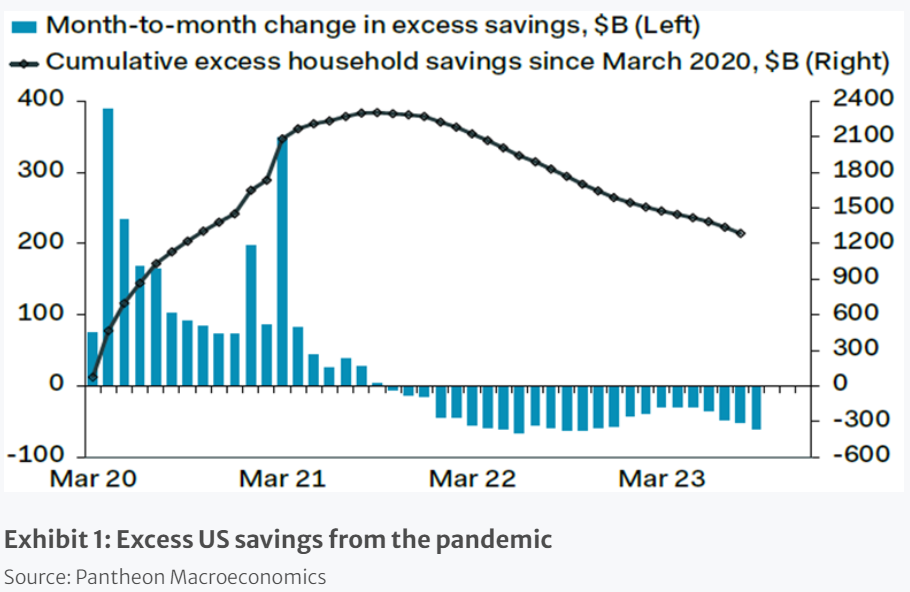

In the US, it is very different. Analysts are deeply divided whether the US economy will go into recession this year or not. Some believe so, whereas others argue a soft landing is the more likely outcome. I belong in the latter camp, and I do so for two reasons: i the spending power amongst US consumers, who make up 70% of US GDP, is still significant with meaningful excess savings aggregated in the early stages of the pandemic (Exhibit 1), and we know Americans love to spend; ii the recent increase in US unemployment is consistent with a soft landing – not a recession. The US labour market is still too strong (graph not shown here).

The reason a soft landing in the US is good for risk assets worldwide has to do with the prominent role of US financial markets. I do not expect more than a modest correction in European risk assets if US risk assets do well on the back of a soft landing over there. Having said that, I actually expect Japanese risk assets to outperform both US and European risk assets, but that is a story I will come back to over the next month or two.

Q2: What is the outlook for commodities?

To a significant degree, the outlook for commodities depends on whether the economy is going to go into recession or not. Many (but not all) commodities delivered poor returns in 2023, very much a function of slowing activities in China. Now, don’t believe those who argue China is in recession. It is not! Having said that, if you are used to 7-8% annual GDP growth and suddenly only grow by 3-4%, it feels like one, and that is where China is today.

If I combine the early signs from China that it has now turned the corner with my forecast that the US economy should escape the worst in 2024, commodities should actually do quite well. That said, commodities are many things – energy, industrial commodities, precious metals and agricultural commodities to name a few, and you are in danger of over-simplification if you argue that the picture is broadly the same for them all.

In my book, two types of commodities stand out at present. Firstly, if China has indeed turned the corner, and if a soft landing, not a full-blown recession, will be the outcome in the US, industrial metals offer good value at present. Secondly, capex amongst oil drilling and exploration companies is now less than one-third of what it was a decade ago (chart not shown). If history repeats itself, lower capex going into drilling and exploration will, in the foreseeable future, lead to a much lower output. In other words, demand may be on the decline, but supply may fall even faster, and that should lead to higher prices.

Q3: Will green stocks continue to rebound after having had a tough year?

The are many sub-groups of green stocks, but most of them have been through a dreadful couple of years after hitting new all-time highs in 2021 (+/-). Towards the end of 2023, most of them started to perform better, though, hence the question – are the bad times well and truly over?

Let’s begin with the bubble forming in 2019-21. At the time, green stock could do nothing wrong, and all (green) boats were lifted. Investors paid little attention to the earnings outlook, i.e. the rally was far too indiscriminate. Suddenly, the tone changed, as investors began to ask questions, and most green stocks have never fully recovered.

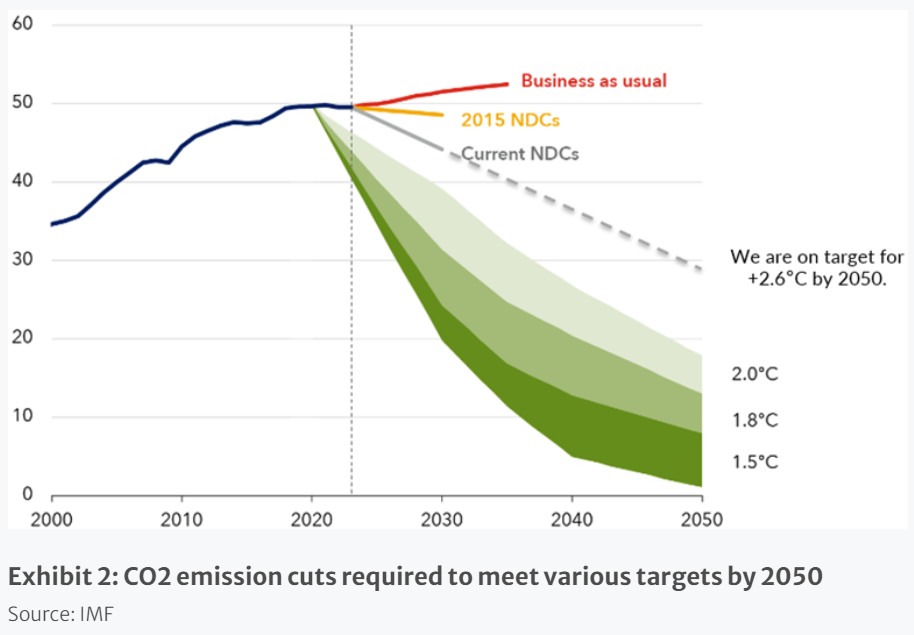

Now, a couple of years later, the outlook for the climate is worse than ever (Exhibit 2), i.e. the need for solutions is higher than ever. The short-term earnings outlook has not necessarily improved a great deal (these sorts of things take time), but green stocks are valued far more attractively today after undergoing a 2-year bear market.

Adding to that, it is indeed possible that the massive challenges that many green companies, particularly wind turbine manufacturers, have faced over the last couple of years could reverse in 2024-25. Profits on most green projects turned negative, as companies were caught out by a combination of significantly higher material costs and punishing interest rates.

Some of these contracts have now been renegotiated, as it was not in governments’ interest to see these companies go out of business. It is now possible that the new, renegotiated contracts will be followed by lower material costs and falling interest rates. i.e. many unprofitable companies could quite possibly turn profitable over the next few years. (See also Q4 below re unprofitable companies.)

On the back of that, I conclude that, yes, the rebounce should continue. That conclusion becomes even more affirmative if the economic slowdown in China is now largely behind us. Having said that, a recession anywhere will dampen demand for green solutions. Governments have a long and solid track record when it comes to letting the environment suffer in times of economic hardship.

Q4: How do you expect equities to react, if interest rates do not come down as implied by the bond market?

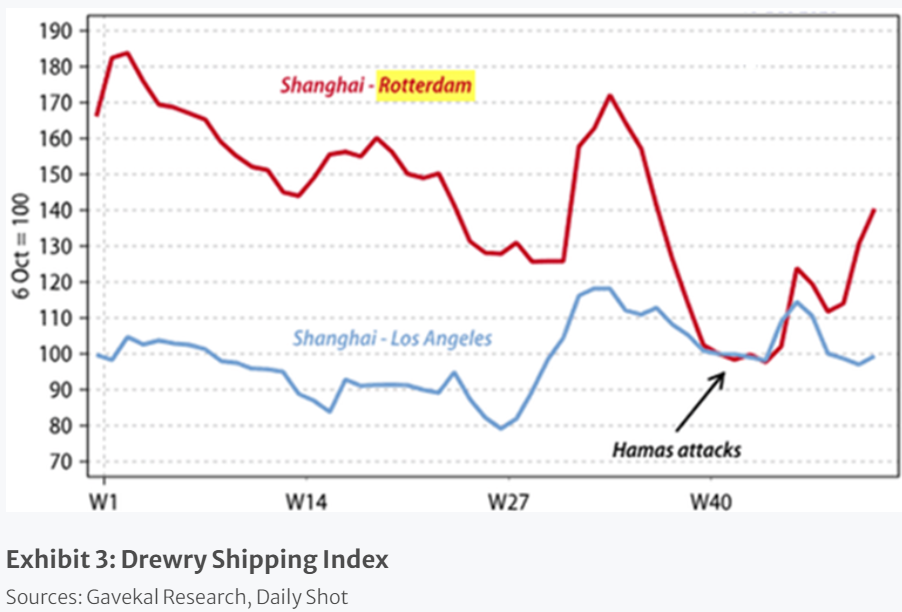

Let’s begin with the well-advertised supply chain problems that drove up inflation in the first place. Supply chain problems worldwide were one of the key reasons inflation suddenly became a major problem after having been dormant for years. After a few false starts, inflation finally appeared to be under control again, but then Hamas attacked and Israel responded in kind. To cut a long story short, it has had a significant impact on shipping rates through the Red Sea, i.e. it has had an inflationary impact on most goods shipped between Asia and Europe (Exhibit 3).

As I don’t expect the armed conflict in Gaza to end anytime soon, ships passing through the Red Sea will continue to be at risk for a fair bit longer. The only alternative route, around Cape of Good Hope at the southern tip of Africa, may be cheaper as far as insurance is concerned but much more expensive in fuel costs. You may argue that this is not a US but a European problem. Whilst partially correct, in today’s interconnected world, and as we learnt during the first supply chain crisis, rising inflation in one part of the world will quickly affect prices in other parts of the world.

Should this force the Fed to keep interest rates higher for longer, first and foremost, ‘junk’ stocks will be at risk. Allow me to explain. I define ‘junk’ stocks as:

As you can see in Exhibit 4 below, ’junk’ stocks performed exceedingly well, following Jerome Powell’s half-promise to lower interest rates at least three times in 2024. Having said that, as you can also see, unprofitable tech companies had a horrid time in Q3 as interest rates rose, thus raising the cost of capital, and so did the most shorted stocks. I assume short covering was a major factor behind them rallying in Q4.

If interest rates have to stay higher for longer, and that is indeed a big “if”, if one takes Jerome Powell’s recent comments into account, the recent Q4 rally is unsustainable. Therefore, the answer to the question is that ‘junk’ stocks are most at risk. That said, just like the ‘junk’ rally lifted all boats, the end of the ‘junk’ rally could sink all boats again.

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

In 2018, Harriman House published The End of Indexing, Niels' first book.

i listed tech companies with negative earnings, thus dependent on borrowed capital to finance the business; and/or

ii the most shorted, listed companies.

A message from Advisor Perspectives and VettaFi: Advisors: You're Invited to Exchange!Nothing would be a better start to the new year than if you joined us at Exchange, an in-person conference for members of the financial services community in Miami, Florida on February 11-14th. For a limited time, we're offering you a free Exchange ticket!* Register today with code WINTER24 to claim your pass.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All