Is the “Vibe-cession” for US Consumers on Its Way Out?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFalling inflation hasn’t yet translated into good feelings among US consumers. Based on the latest data, that might be changing.

Over the past few months, analysts have coined a new term to describe this confounding US economic environment: a “vibe-cession.” It seems there’s a wide disconnect between economists’ optimistic assessments based on incoming data and a stubborn pessimism among consumers. To put it bluntly, consumers just aren’t feeling the vibes.

We think there’s a fairly simple reason for the gap. What’s more, we think it’s starting to close.

By most economic metrics, 2023 was an exceptionally good year. Growth in headline inflation, as measured by the Consumer Price Index, cooled markedly, and it did so without the recession many forecasters viewed as necessary to recalibrate inflation only a year ago. The unemployment rate stayed under 4%, wage growth outpaced inflation and the stock market ended the year at an all-time high.

Despite all the good news, most measures of consumer confidence remained subdued at best, which poses something of a puzzle. But we do see an explanation—and a solution.

With Inflation, It’s a Matter of Perspective

For starters, economists and policymakers view inflation much differently than households do.

Monthly inflation data measures the percentage change in price levels. So, when inflation falls from 9.1% to 3.4%, as it has over the past 18 months, prices are still rising but more slowly. There’s good reason for policymakers to focus on the rate of change rather than the level of prices, because they can’t do anything today to address yesterday’s prices. They can only influence tomorrow’s—and that requires looking at how much prices are changing; not how high they are.

Financial markets, not surprisingly, look at inflation over an even shorter time horizon. Markets have rallied in recent weeks largely because the three- and six-month inflation rates have fallen back to the Fed’s target inflation rates. This progress suggests that rate cuts should turn up in the next few months.

Households experience inflation in a very different way.

Some inflation categories—rents and housing in particular—matter more to households than they do as contributors to the overall price index, and those components have been particularly lofty. Also, while markets may only look back a few months and policymakers perhaps a year, consumers have made it very clear in the past few months that they have a much longer memory.

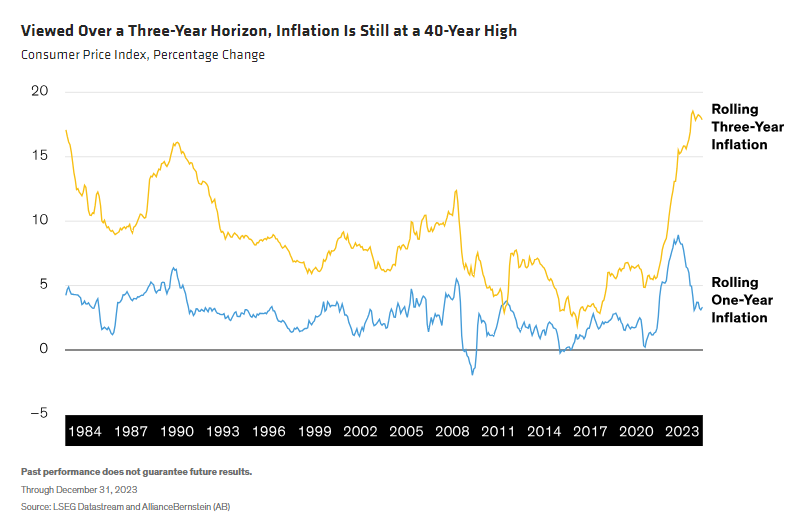

That distinction creates a much different perspective on prices. Inflation may look more or less normal today looking back over a one-year time horizon, but over a three-year time horizon, prices have risen more than at any time since the early 1980s (Display). It’s no wonder households remain skeptical of the market’s belief and policymakers’ growing confidence that inflation has already been defeated.

Signs of Improving Consumer Spirits Are Encouraging

Going forward, here’s the question that matters most to the economic outlook: How long is the consumer’s memory?

Policymakers have no interest in pushing prices down; deflation would almost certainly require a nasty recession and, over the long run, be more disruptive to economic growth than inflation would. The best they can do is restore inflation to normal rates but doing that hasn’t yet made households feel good about the situation. Alleviating that pessimism is critical to stoking economic growth, since household consumption represents roughly two-thirds of gross domestic product.

Recently, there’s been encouraging news on that front.

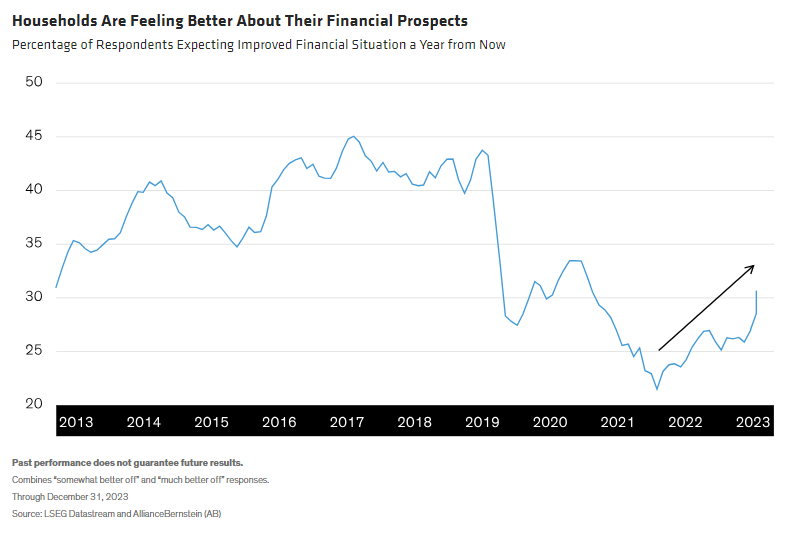

Readings on consumer confidence have climbed, particularly when it comes to households’ assessments of the future state of the economy and their own finances. The percentage of households that expect their financial situation to be better in the next six months, while still below pre-pandemic levels, is up nearly 10 percentage points in the past few quarters—a post-pandemic high (Display).

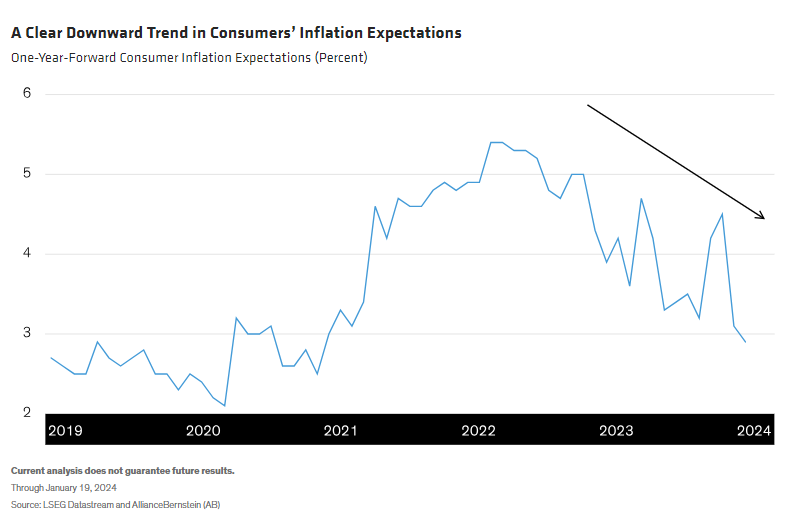

That increased optimism has coincided with a clear downward trend in consumers’ expectations for future inflation rates (Display), which suggests that the statute of limitations on past inflation rates may be ending. Increasingly, it seems that households are focusing on the rate of price changes based on the “new normal” price level.

Falling inflation expectations offer news that’s just as positive as rising overall consumer sentiment. That’s because inflation expectations tend to be self-reinforcing: actual future inflation is heavily influenced by what individuals, businesses and governments expect inflation to be, because expectations guide their economic decisions.

How should we think about all this? We’re clearly not quite at the end of the inflationary road just yet. However, recent data suggest that our forecast that inflation will continue falling through 2024 and into 2025 is still the most likely outcome. If that scenario plays out, consumers’ spirits may improve further, and the “vibe-cession” may be on its way out. That would be a good thing for the US economy.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All