The Fed poured cold water on a March rate cut, but the underlying message still has rates coming down—by a lot. Waiting for the starting point can be risky for investors.

At its January 31 meeting, the Federal Reserve didn’t change its target interest-rate range of 5.25%–5.50%. Chair Jay Powell also signaled that a March rate cut is unlikely. That result may not sit well with investors looking for an early start to the cycle. Should they be disappointed? Is the signal that a March rate cut won’t happen a good reason to stay on the sidelines?

We don’t think so.

As we see it, the Fed’s underlying message bolsters our view that the sidelines could be a risky place for investors waiting to get into the game. To understand the Fed’s thinking, we need to know what it’s aiming for: an equilibrium in the economy that leaves it most resilient against inevitable shocks.

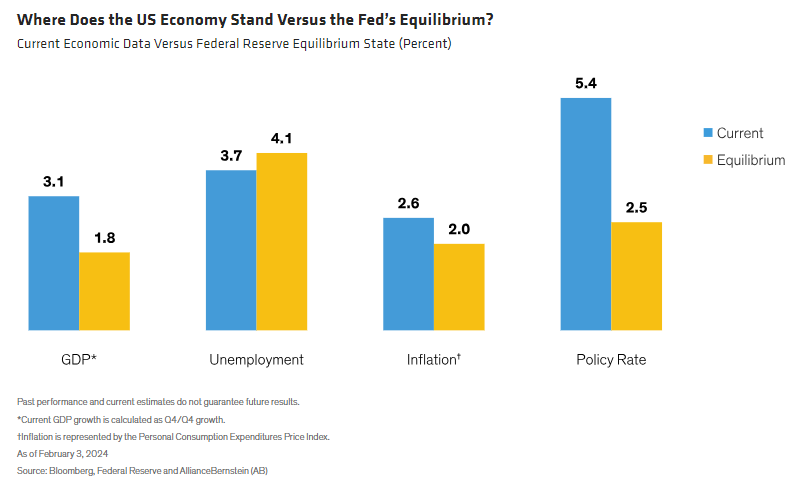

Tale of the Tape: Reality Versus Forecasts

The Fed’s quarterly summary of economic projections describes its view of equilibrium in terms of “long-term” forecasts. It spans three dimensions—growth, labor and inflation—and includes a forecast of the policy rate necessary to keep the economy in balance. To get a sense of where we stand versus the Fed’s target, we can compare these forecasts to the actual data over the past few months (Display).

One thing is clear: the US economy is still running a bit hot. Gross domestic product (GDP) growth for 2023 was above the long-term rate, which kept inflation somewhat warm. Still, growth slowed late in the year and will probably continue declining this year. Inflation fell sharply last year and is likely headed lower again in 2024. Neither number is at its target yet, but they’re close and headed in the right direction. In combination, they argue against the Fed immediately resetting the policy rate to neutral.

But we don’t think they argue against rate cuts altogether, because the policy rate is still more than double the Fed’s estimate of the neutral rate. That situation isn’t sustainable: it would make no sense to have an economy in equilibrium and a policy rate well above equilibrium.

Massive Scope for Rate Cuts Ahead

That, more than anything, is our takeaway from the Fed’s messaging. The policy rate will come down—and by a lot. We can’t say for sure when the first cut will happen, but with the rate almost three percentage points above neutral, the scope for rate cuts over the next few quarters is massive. Even if the economy enjoys a soft landing—as we expect—the Fed will still be making sizable cuts.

That aspect is much more important than whether rate cuts start in March, May or June. In our view, investors who stay on the sidelines and focus on timing the first rate cut risk could miss out: markets look ahead, and the Fed has told us that the path involves significant policy easing.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein