Stronger economic growth is allowing the Fed to stay patient. That means a likely delayed start for expected interest-rate cuts.

The US economy powered ahead in the first quarter, as strong hiring activity and gradually waning inflationary pressures boosted consumer spending, keeping growth on solid footing. In our view, much of that strength will last, supported by changing demographic trends, leading us to increase our 2024 full-year GDP growth forecast to 1.5% in real, or inflation-adjusted, GDP terms.

Robust economic activity has caused inflation to cool more slowly, though we still expect price pressures to ease as the year progresses. But the process will likely be slower than previously forecast, and that will likely affect the path of Federal Reserve policy—including rate cuts. We now expect policy rates to stay where they are for several months, before cuts eventually start late this year.

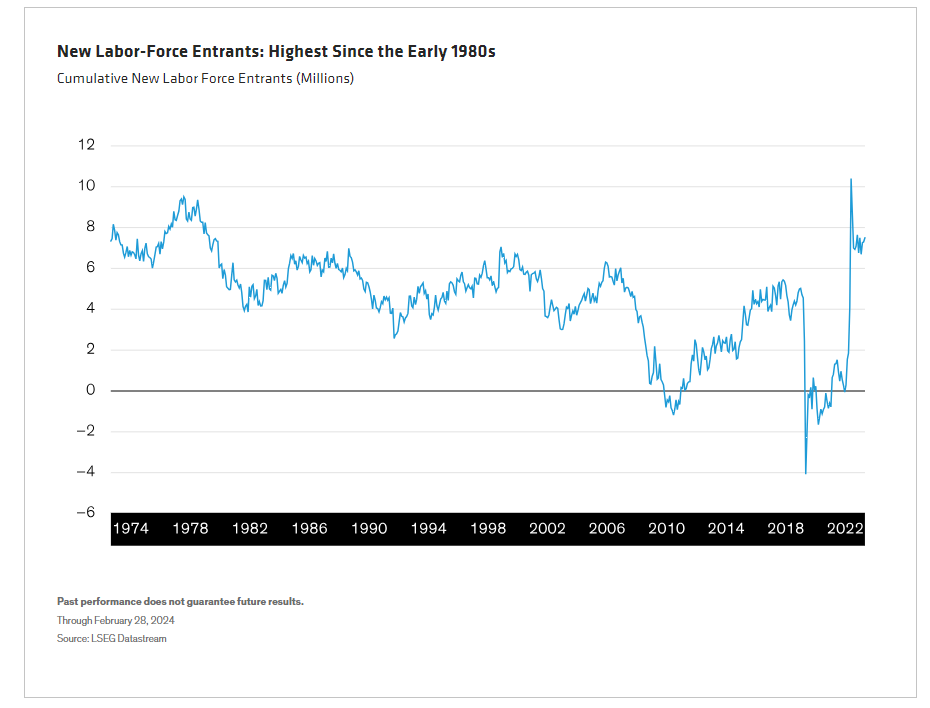

Larger Labor Pool Is Providing Economic Support

What’s driven the last few quarters’ strength, and how does it affect the outlook? Many factors that stoked growth last year, including fiscal stimulus, savings stockpiles and rapid inflation cooling, are fading. But net migration flows surged in 2023, which appears to be behind a significant increase in the supply of available workers: over the last three years, the number of new labor-force entrants has been its highest since the early 1980s.

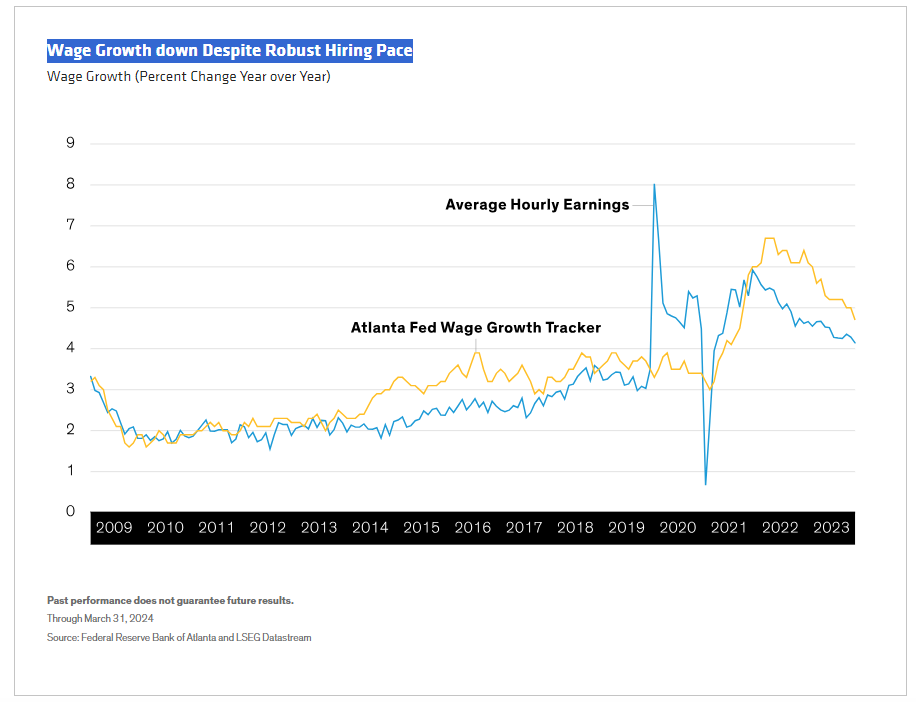

With more workers available, businesses have been able to hire more without ratcheting up wages. Indeed, while wages are growing faster than in the pre-pandemic period and are keeping pace with inflation, wage growth has slowed despite robust hiring. That situation helps the US economy grow more rapidly without too much worry about a wage-price spiral that could de-anchor inflation.

Higher Growth, Low Concern over a Wage-Price Spiral

In 2024, net migration flows seem likely to boost growth again, which, as we mentioned, bumped up our real GDP forecast to 1.5%. That level is just slightly below most estimates of long-run US potential growth. And if we’re right, it would represent a very, very soft landing indeed.

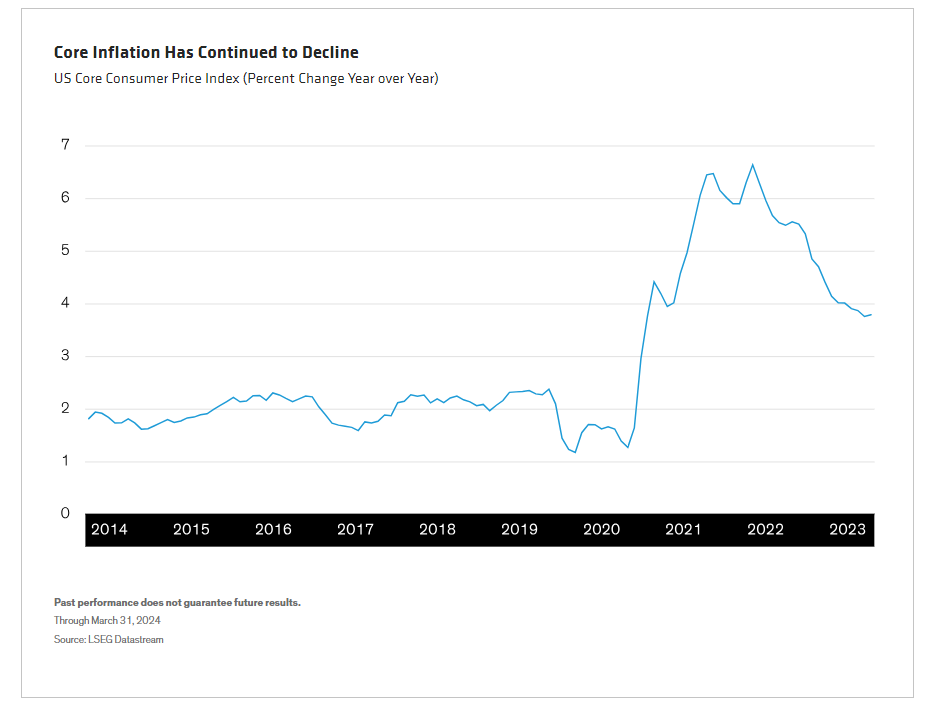

Of course, growth is only part of the equation. A larger labor supply helps tamp down long-run inflation, and the continued deceleration in wage growth suggests little reason for long-term concern about a wage-price spiral. Inflation continued to decline in the first quarter, albeit more slowly than we expected. We think it will take until 2025 for core inflation to fall back to 2.0%. That shouldn’t alarm investors: few would welcome the sharp recession that would be needed to get there quicker.

A Patient Fed Means Delayed Rate Cuts

As long as inflation expectations remain anchored—as they have so far this cycle—we believe that the Fed can afford to take the long view. That means exercising patience, not forcing inflation down immediately. However, patience works both ways: when inflation decelerates more slowly, as it did in the first quarter, the Fed is likely to respond by delaying rate cuts.

That scenario is exactly what we expect. Instead of four rate cuts starting in the second quarter, which we initially forecasted, we now expect only one cut of 25 basis points in the fourth quarter. That may disappoint markets, which have looked for more aggressive easing, but it shouldn’t make a big difference for most investors. As we see it, it’s more important that the Fed be ready to cut rates when inflation falls or growth wobbles than for investors to know exactly when the first cut will happen.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein