Harnessing Income Opportunity in High Yield Credit

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey points

- Opportunities in high yield: High yield credit offers the potential for higher income and lower interest rate exposure than other fixed income asset classes. A resilient US economy and company earnings outlook helps to offset fears of credit stress from higher financing costs, leading to a more benign default rate outlook.

- A systematic approach to high yield credit: The iShares High Yield Systematic Bond ETF (HYDB) seeks to track an index seeking to outperform the broad high yield market by systematically managing credit risk and identifying issuers with attractive valuations.

Elevated all-in yields in high yield credit present an attractive opportunity for income-seeking investors to lock in higher levels of income. Of course, that comes with a much higher degree of risk as compared to sitting in cash. As a result, allocations to high yield in a portfolio context can be considered relative to both equity exposures (based on risk level) and cash and fixed income holdings (for income).

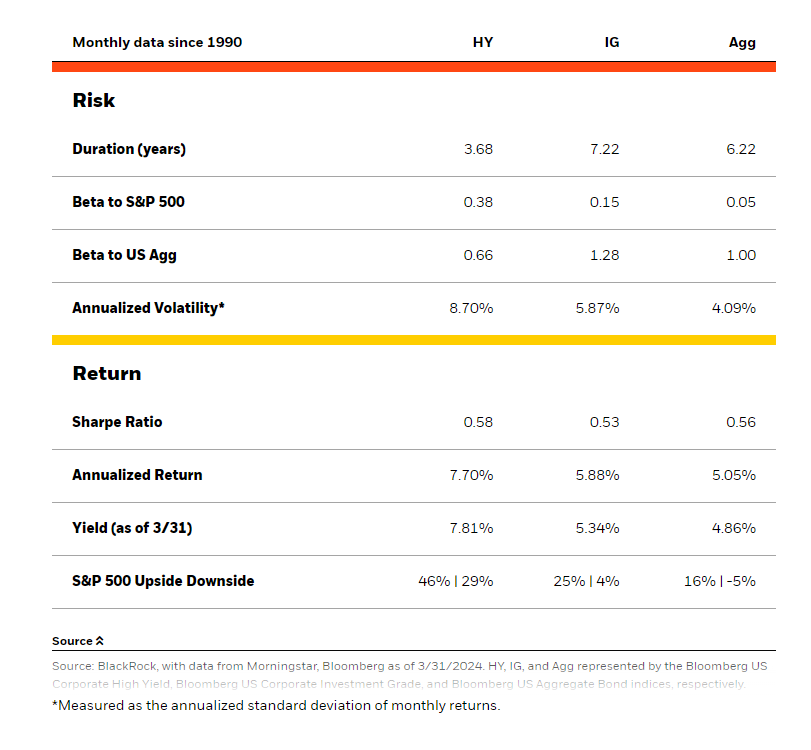

As compared to equity risk, high yield returns historically offer a degree of equity upside return capture with lower volatility and lower downside. But compared to fixed income risk, high yield has also exhibited lower interest rate sensitivity (Figure 1). High yield offers a combination of greater equity risk (and income) at the same time as it offers lower duration risk as compared to other fixed income alternatives.

Figure 1: High yield economic and interest rate risk vs. other fixed income assets

Out-of-sync cycles

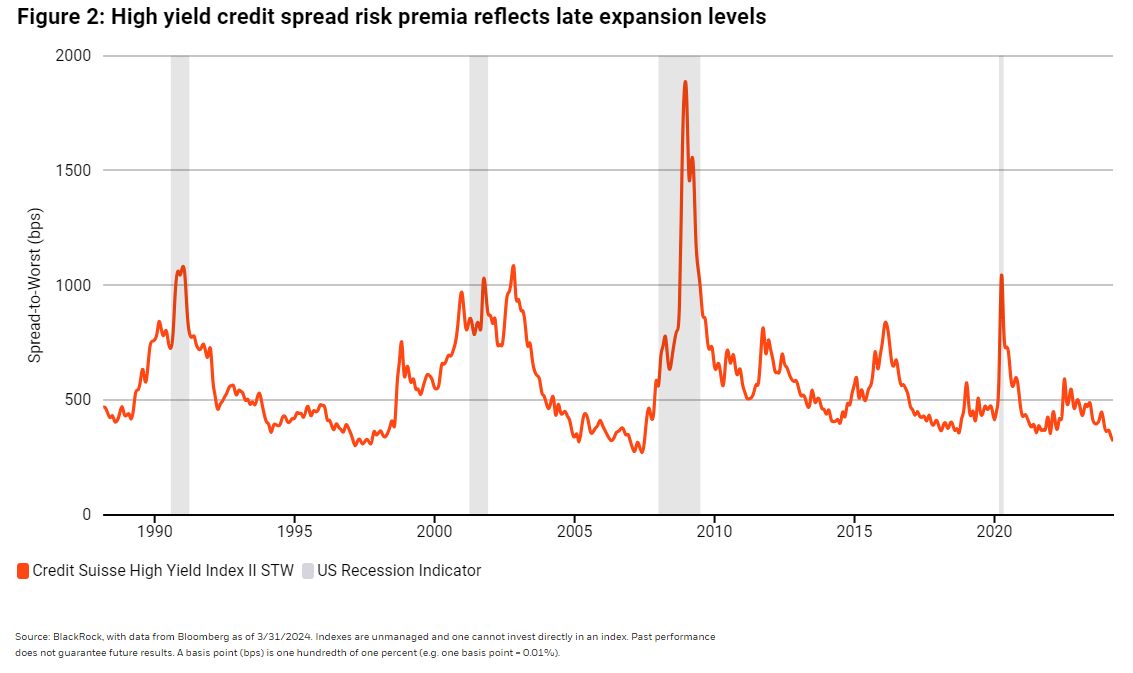

Recent economic performance not only avoided last year’s consensus expectations for recession, but recent strength in growth shows signs of a mid-cycle slowdown reverting back into expansion. This macroeconomic development supports the case for a benign default cycle and the outlook for considering an investment in high yield. Yet, while the economic cycle shows signs of expanding and all-in yields appear historically attractive, the pricing of credit risk shows very full valuations—more akin to late economic expansion levels of high yield credit spreads.

Managing the risks, reaping the rewards – a systematic approach

Managing the risks in high yield investing has long been about avoiding the downside of defaults. When faced with less accommodating valuations, managing these risks becomes even more important to forward looking returns. While passive investing in high yield offers benefits of low costs and transparency, actively managing default risks and considering relative valuations has the potential to lead to meaningful outperformance in higher risk asset classes like high yield—which is especially important at this point in the credit cycle and considering current credit risk premia valuations.

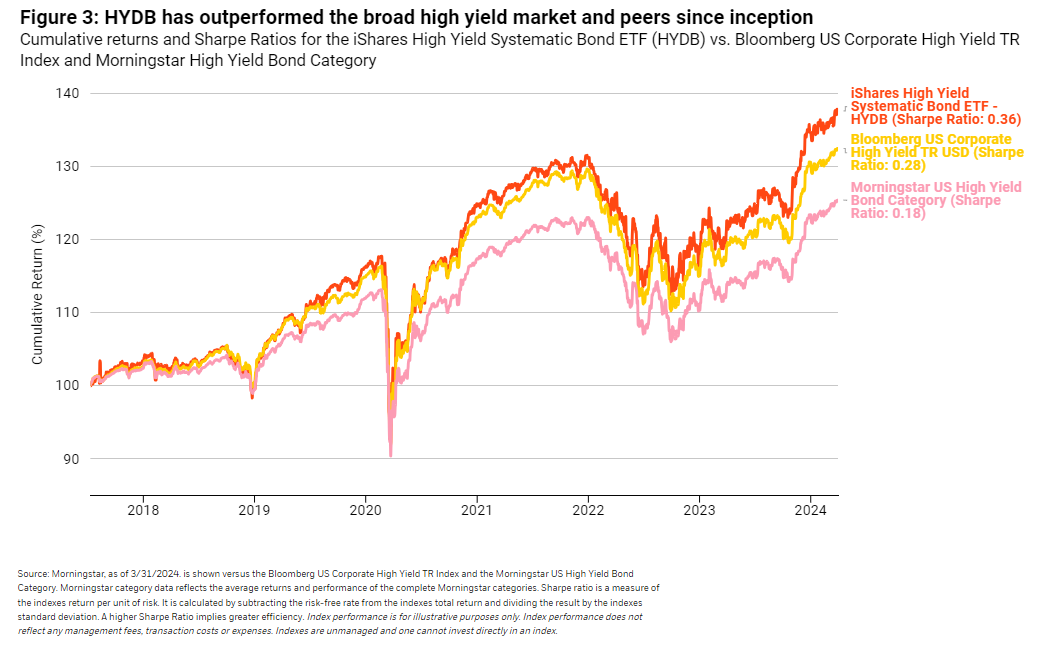

The iShares High Yield Systematic Bond ETF (HYDB) pursues income and enhanced total return relative to the high yield bond market through a systematic process designed to manage credit risk by avoiding the most default prone issuers while attempting to maximize returns by identifying issuers with attractive valuations relative to those risks. And though past performance does not predict future performance, throughout its nearly seven-year history, this combination of systematically screening on quality and selecting for value has delivered higher absolute and risk-adjusted returns relative to the Bloomberg US Corporate High Yield Index with average annual outperformance equaling 0.63% (Figure 3).

Performance data represents past performance and does not guarantee future results. Investment return and principal value will fluctuate with market conditions and may be lower or higher when you sell your shares. Current performance may differ from the performance shown. For most recent month-end performance and standardized performance, click here.

A systematic approach to capturing high yield opportunities and managing risks

The index strategy of mitigating risks and identifying attractive opportunities has resulted in outperforming the broad high yield market and active peer group in both absolute and risk adjusted terms—illustrating the long-run differentiation that HYDB has shown in practice.

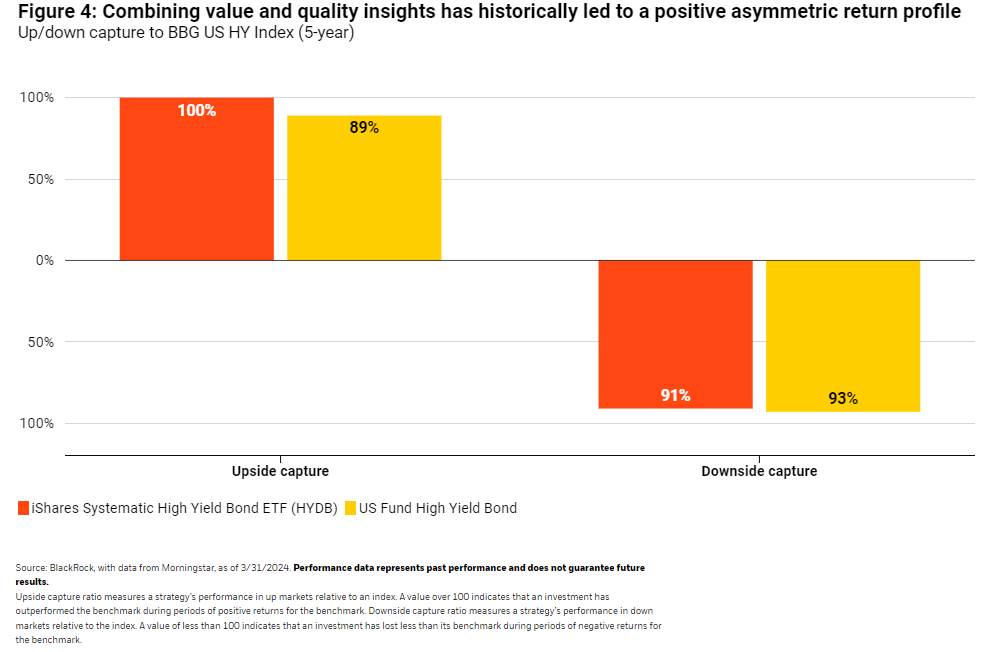

Through an investment process that focuses on avoiding companies with higher credit risk and prioritizing issuers with attractive valuations across the portfolio, HYDB seeks to manage the tradeoffs between upside participation, maximal income, and downside risk mitigation.

This is done first by seeking to reduce downside risk using a proprietary probability of default model. This screens out the riskiest bonds from the starting investible universe. Next, the remaining bonds are weighted to prioritize credits with the most attractive valuations. Finally, the portfolio is optimized to benefit from the diversification characteristics of the broader market with regard to credit quality, sector, and maturity. Shown in Figure 4, this has resulted in an asymmetric return profile compared to the average high yield fund, capturing greater market upside and generating more resiliency in down markets.

The bottom line

The potential for higher coupon income in a world where policy rates no longer lead to rising yields on holding cash can make locking in yield in fixed income more attractive. Yet doing so also entails adding duration risk—the risk to higher term interest rates. High yield bonds offer a combination of higher income through exposure to economic risk (at a time of decreasing economic risks) that also offers less sensitivity to rising interest rates than other fixed income assets. Investors allocating to high yield may want to consider the repeatable, rules based, investment process employed in HYDB that seeks to systematically screen out riskier companies while identifying issuers with attractive valuations to maintain upside participation. This time-tested approach has the potential to target better outcomes in the asset class as investors navigate a more volatile rate regime particularly at a time of historically low credit risk compensation.

Carefully consider the Fund’' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Fund’' prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.ishares.com or www.blackrock.com. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

This material contains general information only and does not take into account an individual's financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial professional before making an investment decision.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/ developing markets or in concentrations of single countries.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Index performance does not represent actual Fund performance. For actual fund performance, please visit www.iShares.com or www.blackrock.com.

The iShares and BlackRock Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

©2024 BlackRock, Inc. or its affiliates. All rights reserved. iSHARES and BLACKROCK are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

iCRMH1223U/S-3268809

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All