Investors have seemed transfixed lately by endless news headlines on the path of monetary policy. But fiscal policy outcomes have far-reaching impacts on long-run growth and fundamentals in the world’s economies. On that score, many regions continue to wrestle with the challenges of deficits and debt.

Persistent US Deficit Poses Growth Headwinds

The US economy has exceeded all expectations over the last few years—a global standout, with fiscal policy an unusual driving force. Typically, economic cycles feature large budget deficits in bad economic times, as governments stoke demand to avoid a more sinister outcome than recession. After the recession, fiscal policy retrenches as tax revenues pick up and emergency-support programs expire.

This cycle in the US has played out a bit differently.

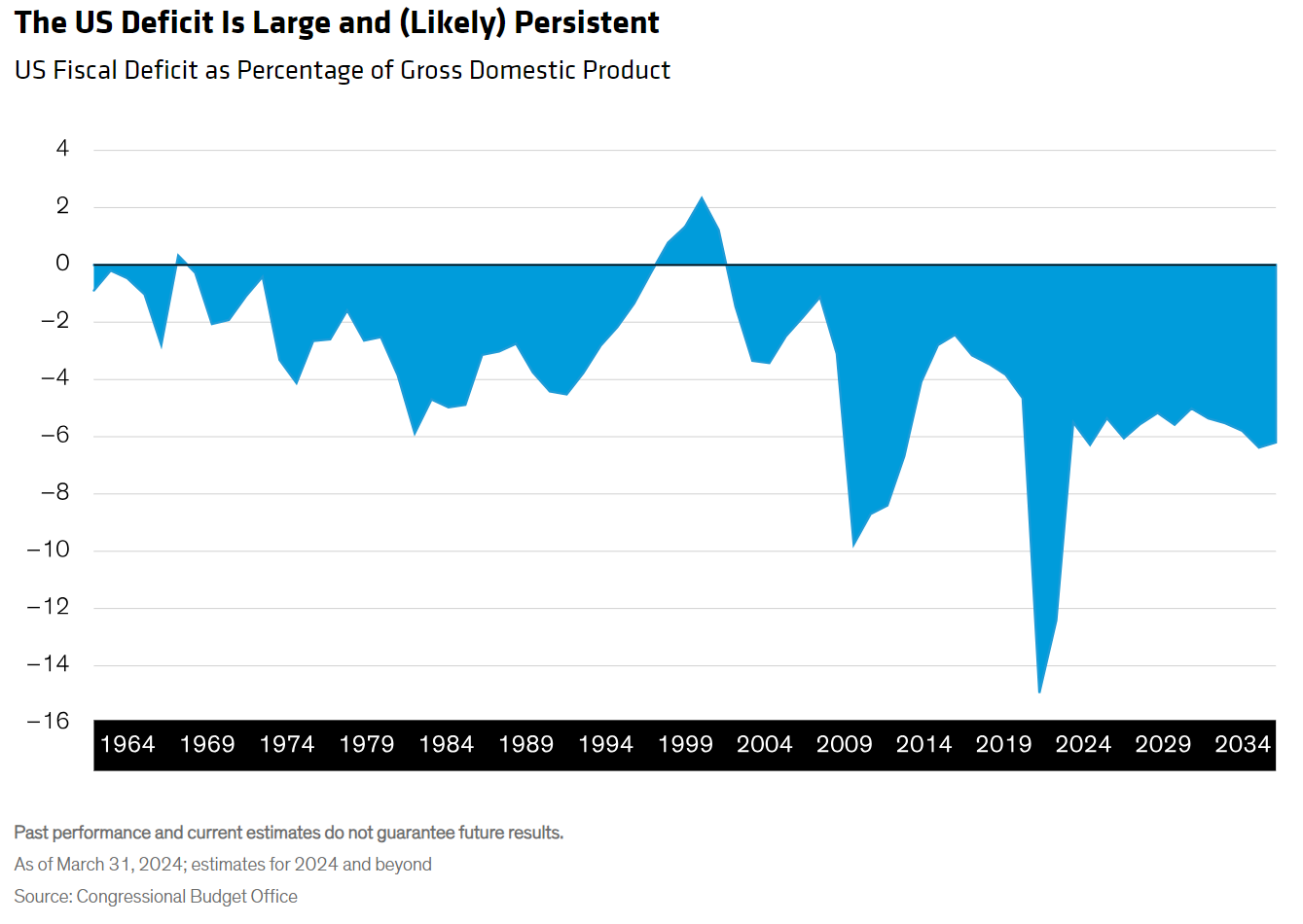

Demographic trends are elevating entitlement spending, and higher spending on infrastructure and other pandemic-era priorities has kept overall government outlays above pre-pandemic levels. At the same time, past tax cuts have constrained revenues. The resulting deficit is roughly 6% of gross domestic product (GDP) (Display), and that level seems set to continue for the next decade, as per Congressional Budget Office (CBO) forecasts. That’s a bigger deficit than would be expected outside of a war or recession.

Is the deficit supporting growth? Yes and no.

Incremental deficit change is what influences growth rates, so a stable deficit for the next several years wouldn’t meaningfully impact GDP growth. Still, the absence of a fiscal-spending pullback has played a role in the expected soft landing. The landing would likely have been harder—maybe even a recession—if fiscal policy had tightened as much as is typical post-recession. The average US budget deficit in “normal” times is around 3.5% of GDP—about 2.5% below the current run rate—which would have been a bigger drag on economic growth.

While larger deficits may have helped keep growth stable, they do come with a cost: rising debt. The ratio of Treasury debt to GDP is over 100% today and is set to rise in years ahead barring a major change in fiscal policy. We don’t think this will cause a near-term crisis, but the combination of rising debt and rising interest rates will boost the government’s debt-service ratio—the cost of repaying existing debt. That’s money that can’t be spent on more productive investments, and it may limit fiscal flexibility the next time the US economy stumbles.

Flexible Fiscal Discipline: Europe’s New Normal

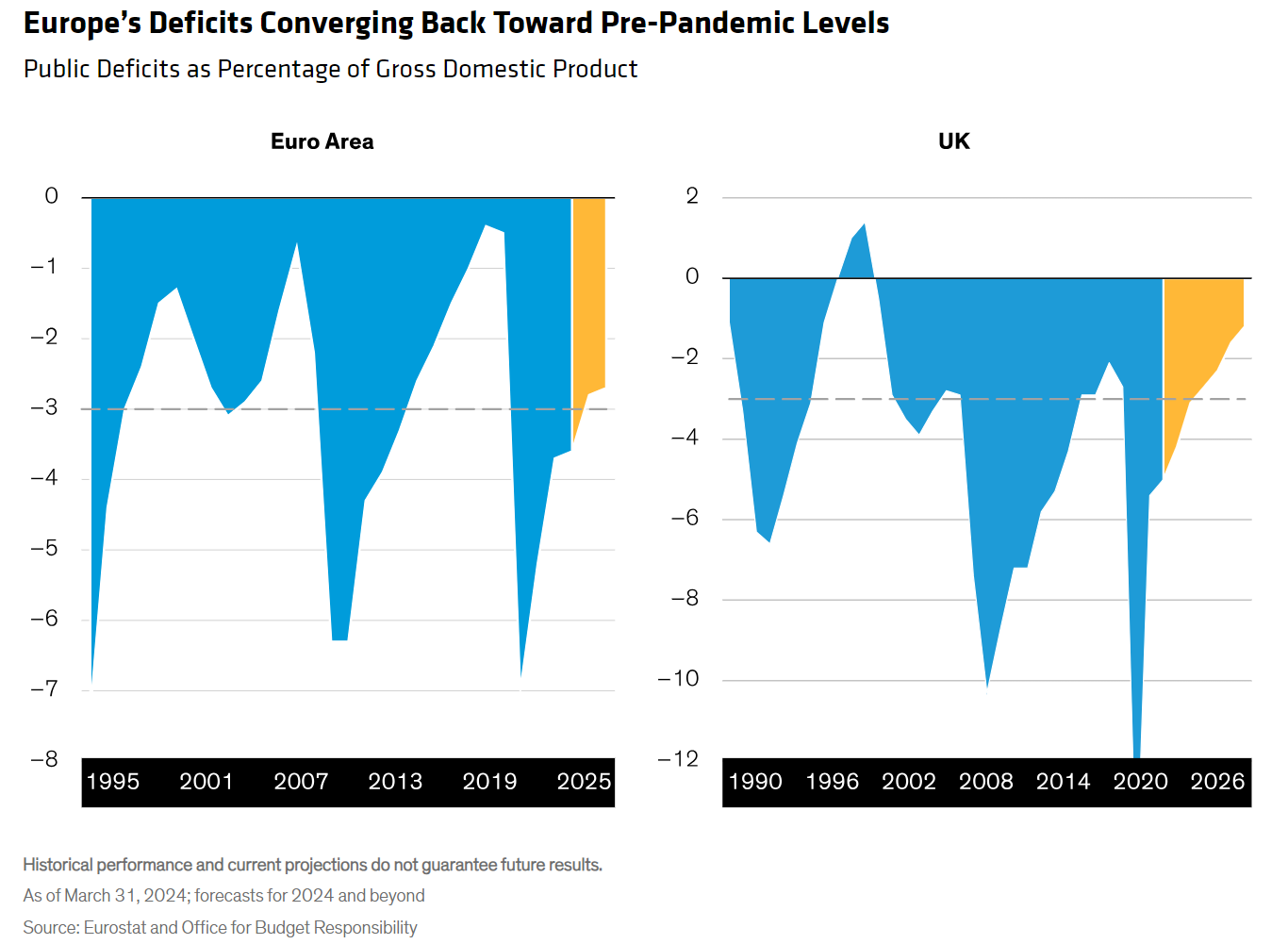

European fiscal policy has helped limit the economic downturn from successive shocks, pushing the budget deficit to an average of 5.3% from 2020 to 2022. Discrepancies are sizable: Italy and France still run large deficits, while Spain and Germany are positioned much more sustainably. The overall eurozone debt/GDP ratio, declining before the pandemic, has risen to 88% and is expected to remain high.

As it stands, both the fiscal deficit and debt/GDP levels exceed limits under the Stability and Growth Pact (SGP), which are 3% and 60%, respectively. But the fiscal impulse—the impact of government spending and tax policies on economic growth—turned negative in 2023 and should stay there in 2024, as countries continue to phase out all energy-related support. Also, the SGP, which was suspended in 2020 to enable member countries to deviate from imposed fiscal constraints, has been reactivated for 2024.

Among the implications of the SGP’s reactivation is that countries planning to exceed the 3% deficit limit in 2025 risk an excessive deficit procedure (EDP) that could stoke short-term volatility. That said, the SGP’s aim is to foster fiscal discipline, and countries that trigger an EDP will be forced into steeper fiscal adjustments. However, these adjustments will likely be smoother than under previous SGP versions; they take country-specific characteristics into account, permitting a more flexible path toward fiscal targets.

Ultimately, fiscal consolidation remains the main end goal of the new SGP. The European Commission expects to pare the deficit to 2.8% of GDP in 2025; a similar trend could play out in the UK (Display), despite a potentially challenging election year. As in Europe, the UK fiscal impulse will turn negative and stay there for several years. The government must also meet fiscal rules, namely to bring down debt and deficit ratios in five years; both objectives are expected to be achieved.

So, from our perspective, the big picture for Europe’s economies seems to be a new normal, highlighted by flexible fiscal discipline.

Mixed Fiscal Progress Across Emerging Economies

Debt distress, delays in sovereign-default processes and debt dispersion have driven the narrative in emerging markets (EM) over the past few years. Aggregate government debt, excluding China’s, is projected to stabilize around current levels just below 60% of GDP—roughly 7% above the pre-pandemic level. Africa, Asia and Europe have struggled to regain solid fiscal ground in the wake of the pandemic, while Latin America and the Middle East have been relatively successful in rebuilding fiscal buffers.

Latin America’s fiscal improvements reflect prudent fiscal policy but also strong economic growth—derived in part from US exceptionalism. The Middle East’s debt dynamics improved largely because of higher oil prices. Economies more integrated with the US business cycle (or that derive large shares of revenues from oil) have been relatively successful in consolidating debt; stronger ties to Europe and China have been less helpful during this cycle.

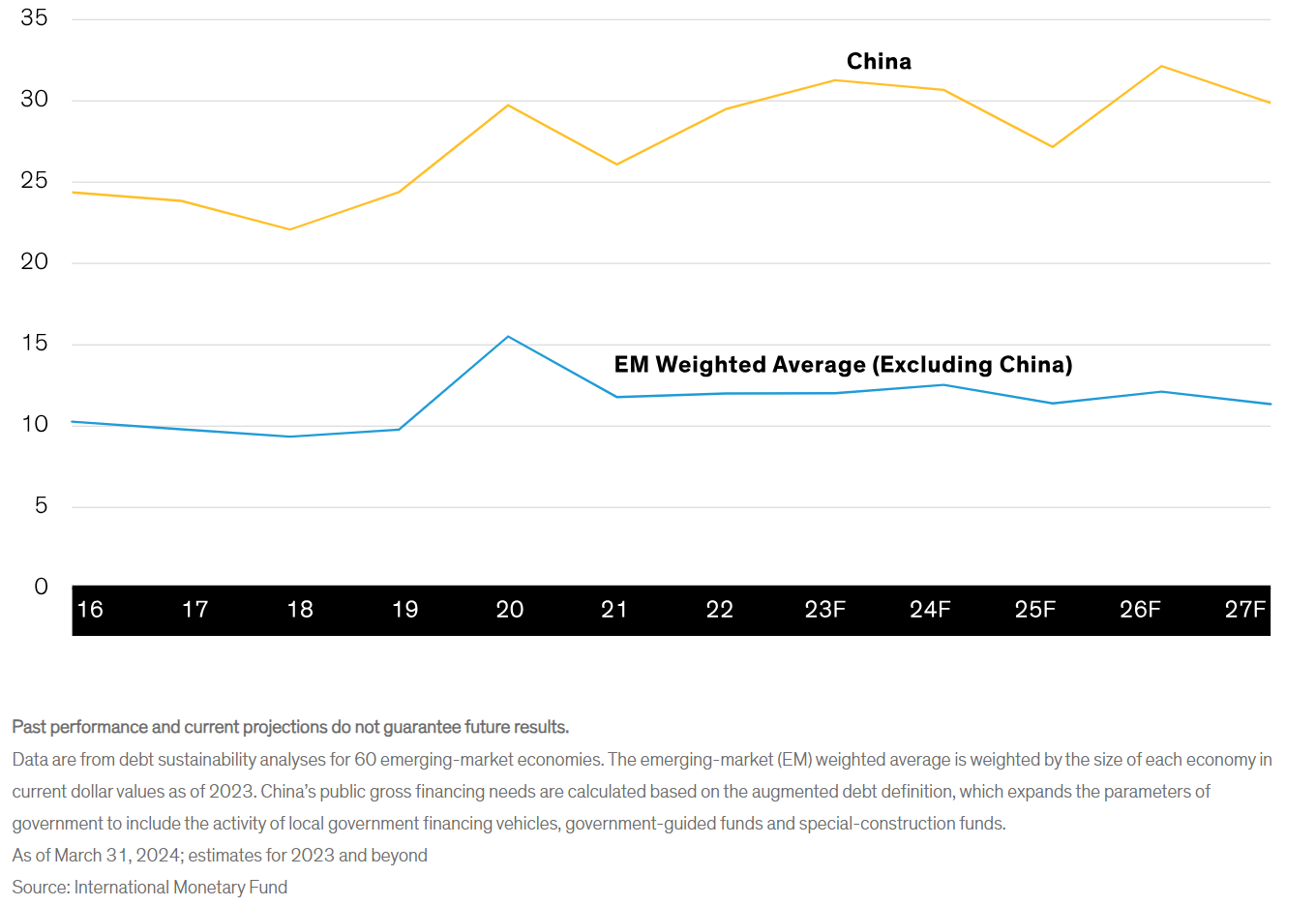

Asia’s rising debt trajectory has been driven largely by China. An expansive view of its government debt that includes activities of local government financing vehicles, government-guided funds and special-construction funds reveals a debt surge to about 120% of GDP from around 50% a decade ago. International Monetary Fund projections call for debt growth in China to outpace debt growth in the US for the foreseeable future.

The lack of fiscal belt-tightening in the world’s two largest economies might limit downside risks to global GDP growth, but it could also crowd out EM financing. Scarcer financing sources amid an upward shift in financing needs would require even more fiscal restraint (Display).

What might help ease the pressure? The speedy resolution of sovereign defaults is important, and the recent financial support and policy signals from multilateral agencies could also help. The use of state-contingent factors for debt restructuring and frontier markets regaining market access—could reduce medium-term financing costs if targets were met.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© AllianceBernstein

Read more commentaries by AllianceBernstein