“Knowledge has to be improved, challenged, and increased constantly, or it vanishes.” -Peter Drucker

Off The Top Rope!

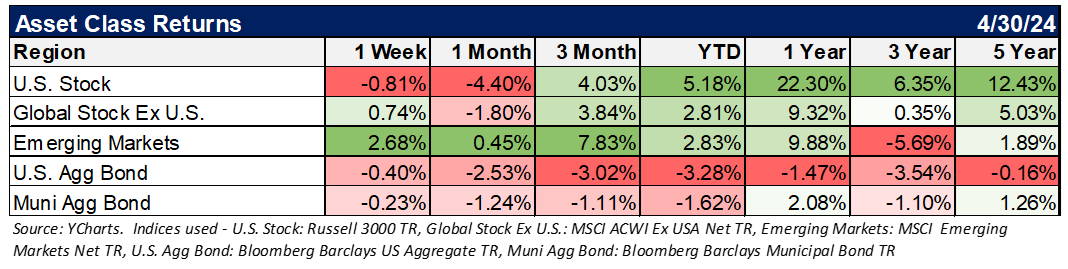

In trader speak, a “correction" is defined as a decline of 10%, and in this latest episode, there was only a slightly more than 6% drop from the top. The stock market recovered some of those losses the last two weeks of the month, but the benchmark indexes have continued to trend higher over the last year and a half. This market’s “steady climb higher” has referred to the S&P 500, while the other market cap sectors have experienced a rockier ride.

U.S. Small Capitalization stocks (Small Caps) are around -13% below the level from three years ago, while mid-caps are only modestly positive. We have been underweight to the Small and Mid Caps (SMID) for the last three years and attribute this disparity in return to the perception that more prominent companies are better positioned to withstand the widely anticipated challenging economic environment, including higher interest rates and the possibility of a recession. The rationale is that smaller companies rely more on floating-rate bank lines of credit, while large corporations more frequently issue fixed-rate bonds. The higher interest rates, in turn, compress the profitability of these smaller companies.

While we anticipate that the inflation data will be “lumpy” (we prefer the term “sticky”, as there will be ebbs and flows), with some factors concurrent to reports and some lagged, we are generally sanguine about the overall market backdrop. We continue to view the economy as steady, with the price level high but a reasonable inflation rate running in the 2.5-3% area.

Over halfway through the first quarter earnings season, the S&P 500 is on track to show +3.5% growth. The improvement came across multiple sectors, with Big Tech providing the latest push. Energy is the sector leader, while large growth in style and Momentum are the best-performing factors. We maintain our preference for large-cap U.S. companies, specifically high-quality companies.

While inflation is a bit lumpy, it has been on a downward trend for some time. Unemployment remains below 4%. The Fed has backed off a bit in cutting rates, but the next rate move is still expected to be down. This isn’t exactly “Goldilocks” territory, but we are not in bad shape domestically.

What Keeps You Up At Night?

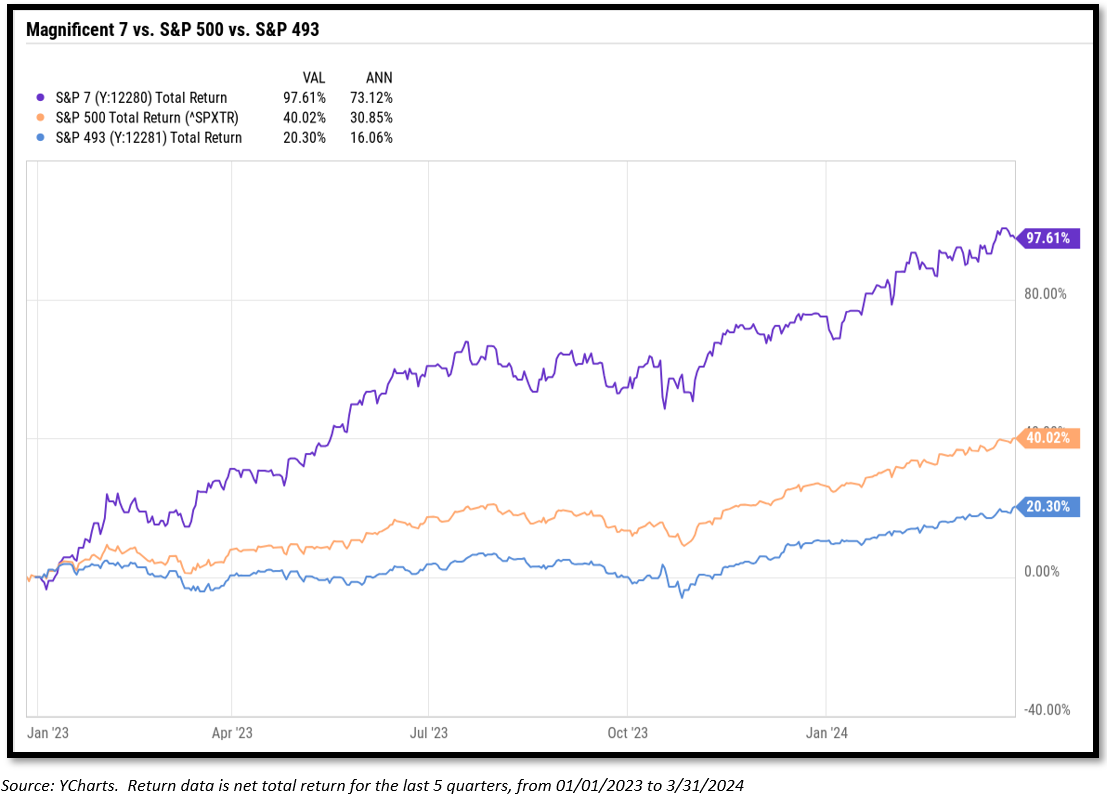

The Magnificent 7 (we’ll call them the S&P) currently accounts for roughly one-third of the S&P and has a market cap larger than the Japanese, Canadian, and UK equity markets combined. The breadth of market returns is a concern, and we can’t hope that a few companies control the fate of investor returns. If you compare that Magnificent 7 to the overall S&P 500 and the S&P 500 without those stocks, you can see a stark comparison in performance.

REPEAT - We Are NOT In The Prediction Business.

We’ve often said that we are not in the prediction business and we are not trying to pick the next stocks that will outperform. Having broad allocations, (which start with the benchmark allocations), allows us to participate well with markets instead of trying to pick the next Maginificent 7 as the drivers of returns change over time. If you didn’t own Disney stock or IBM stock in the 70s/80s/’90s, you probably didn’t perform very well. Fast forward to today, and if you didn’t own Alphabet, Apple, Amazon, Meta, Microsoft, Nvidia, and Tesla, you also probably didn’t perform well. Who will be the next batch of outperformers?

From the Investments Desk at Journey Strategic Wealth

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Journey Strategic Wealth

Read more commentaries by Journey Strategic Wealth