As banks continue to pare back financing activities, consumer lending is taking up more space in investors’ private credit allocations. Known as asset-based financing, this form of lending is the engine that powers the real economy, and we believe it has the potential to boost portfolio returns, reduce volatility and diversify existing exposure to corporate credit—both public and private.

But with interest rates set to stay higher for longer, is now the right time to add exposure to consumer debt? It’s a fair question—particularly in the US, where a recent Federal Reserve survey showed that some borrowers were falling behind on auto and credit card payments.

We think the answer is “yes,” and here’s why: Not all loans are alike—even when they’re made to borrowers with comparable credit scores and against similar collateral. For investors, the key consideration isn’t the type of loan or the near-term economic outlook, but the quality of the underwriting—a private lender’s assessment of a borrower’s creditworthiness and the quality of the loan.

In this sense, private credit investors are underwriting the underwriters.

Asset-Based Financing: A Burgeoning Market

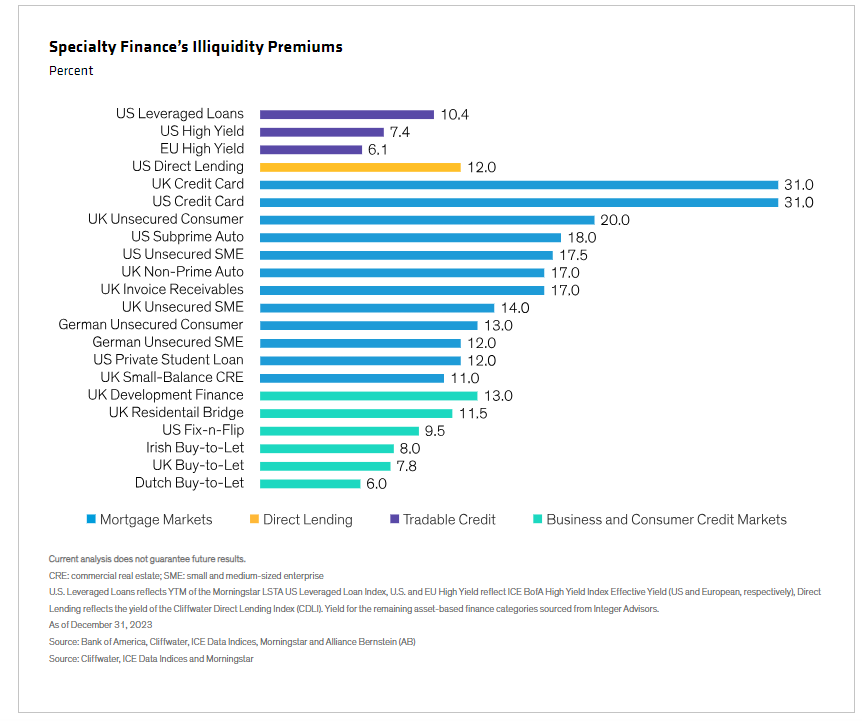

Also known as specialty finance, asset-based financing has grown over the last two decades into a $6.3 trillion market that provides much of the financing for residential and commercial properties, cars, credit cards, small business loans, commercial equipment and a variety of niche sectors—including revenue streams tied to intellectual property royalties. Most loans are made against collateral—typically financial assets or hard assets, such as autos or business equipment.

Of course, banks in the US and Europe once did much of this lending themselves, but stricter regulations have forced them to cut back. Private lenders have filled the gap. Now, many banks sell a sizable portion of the loans they originate to private credit investors, often through forward-flow arrangements in which the buyer agrees to purchase a certain amount of loans over a specific time frame.

Because these assets tend to be less liquid and more complex, they typically offer a yield premium over high-yield bonds, leveraged loans and other forms of public credit (Display).

North America is the more mature market given its scale, depth and availability of data. But Europe’s smaller size, different legal regimes and varying degrees of data quality create inefficiencies that can lead to opportunity for private credit investors capable of navigating these younger markets.

With Loan Vintages, a Year or Two Can Make a Big Difference

But the wide variety of private lenders means that underwriting standards on originated loans may vary considerably. In our view, how soundly a loan is underwritten is one of the most reliable indicators of performance. And it doesn’t take long for lax underwriting to cause problems.

When the COVID-19 pandemic ended, many nonbank lenders were eager to boost growth by maximizing the amount of loans they originated, so underwriting standards plummeted. At the same time, hefty onetime stimulus checks fed consumer spending. Many consumers splurged on big-ticket items, including new or used cars that had undergone sharp price inflation. It wasn’t uncommon to see buyers put 20% or more down. However, because the money financing the purchases was a onetime payment, it wasn’t as reliable an indicator of performance.

The distress or delinquency in the US auto, credit card and other loan markets that is dotting the headlines today is driven in large part by loans that were originated in 2022, when lax underwriting was common.

The 2023 loans, on the other hand, have been performing better, thanks to tighter standards and interest rates that are more in line with the market. In our view, now looks like a good time (for those who can look past the headlines on the 2022 vintages) to acquire newly originated loans, which are generally higher-quality ones. What’s more, fewer investors are actively buying whole loans after the post-COVID weakness. We believe that those with the ability to be selective can isolate quality assets and originators and increase their return potential.

Sourcing Loans: Skin in the Game Matters

The ability to source loans is still important, and there are multiple lenders and platforms from which investors can do this. To build in diversification and a potential downside cushion, investors can also require that loan originators hold a certain percentage of all loans—colloquially known as “keeping skin in the game.” This creates incentives to keep underwriting standards tight.

A typical portfolio might include hundreds or thousands of loans with varying types of collateral and cash flows, which may provide diversification. Typical portfolios also exhibit a low correlation to public equities and bonds, as well as to direct corporate lending, a segment that dominates many investors’ private credit allocations.

Lenders have far less control over the direction of the economy than they do over loan underwriting. If growth slows and unemployment increases, losses may rise. But analyzing historical data and asset performance at different stages of the economic cycle may help managers identify the attributes that make a loan most likely to hold up well in varying credit environments.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi:more about this and other topics, check out some of our videos.

© AllianceBernstein

Read more commentaries by AllianceBernstein