Maximizing Opportunities in Derivative Income

Membership required

Membership is now required to use this feature. To learn more:

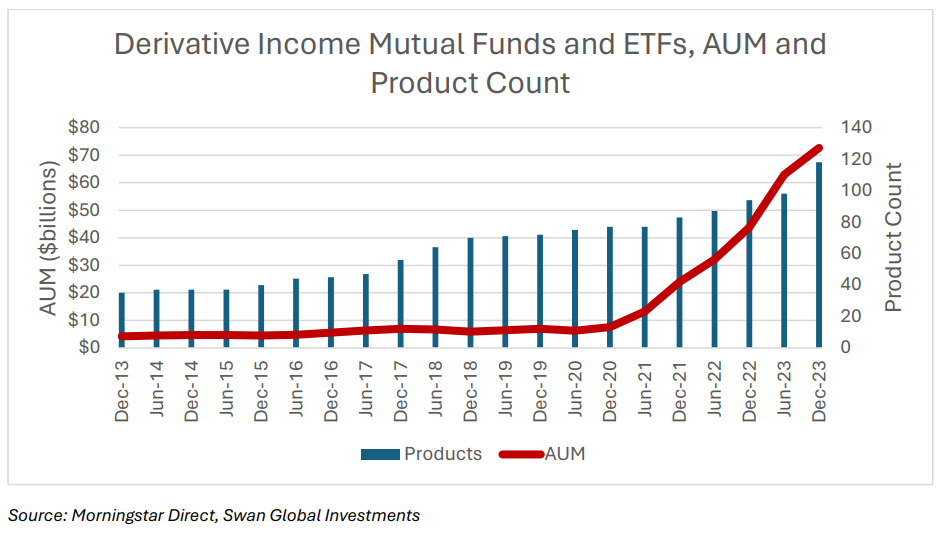

View Membership BenefitsThe derivative income space has grown tremendously over the last five years. Since the end of 2019 there has been a ten-fold increase in assets invested in derivative income ETFs and mutual funds, from $7bn to $73bn. Clearly, investors are seeking options to diversify their income sources to be less dependent on the Fed’s monetary policy.

Many of these derivative income products are based on a covered call options strategy and contain at least one, if not several elements, which can be described as “passive management.” These include:

- The underlying equity portfolio is based on an index, usually the S&P 500.

- The options traded are options on an index, again, usually the S&P 500.

- The way options are traded is very rote and systematic and does not adapt to market conditions.

Swan Global Investments strongly believes that investors are better served by active management in each of these three facets of a derivative income strategy.

Actively Managed Underlying vs. an Index

The first step in creating a derivative income strategy is the underlying equity portfolio. The easiest thing to do so would be to spend no time or effort on this step and simply invest in or replicate a popular index like the S&P 500.

However, the easiest thing might not be the best thing. Swan believes the strategic objective of a good derivative income strategy should be total return, with both sustainable income and capital appreciation.

To that end, dividend-producing stocks should be an obvious focus in a derivative income strategy. Option writing might not always be profitable and there may be periods when such trades fail to produce the returns required to generate the hoped-for yield. However, not all the stocks in the S&P 500 or the Nasdaq 100 issue dividends. By actively leaning into stocks with stronger dividend policies a derivative income strategy can diversify its sources of income.

In addition, some of the stocks in an index are better candidates for call-writing than others. If one is to write calls on individual names rather than a broad index (as discussed in the following section) it makes sense to actively choose stocks that have a rich, deep, liquid option chain to trade.

Finally, if the call options written are based on individual equity holdings, it makes sense to have a focused, manageable list of 50 or so names rather than 500 stocks. Writing and managing 500 call options on 500 stocks would be inefficient, impractical, and likely unprofitable.

Option Writing on Actively Selected Stocks vs. an Index

Many of the derivative income strategies write options on the S&P 500 index. S&P 500 options are the most widely traded equity options in the world; the chain of expiration dates and strike prices is robust and liquid. However, the flip side of the popularity of S&P 500 index options is that premiums are low. It is a much more efficient market, with tight bid-ask spreads and therefore less profit potential.

There is more “meat on the bone” when trading individual options. The premiums tend to be richer because individual equities are almost always more volatile than the broad-based index.

In addition, having a diverse portfolio of stocks presents more profit opportunities for an active options manager to exploit. If the strategy is trading options on a single entity like the S&P 500 index, the index will be up, down, or flat in any given period. This limits what the portfolio manager can do to collect premium.

Alternatively, if the portfolio contains 50 or so individual equities at any given point in time it is likely that some stocks will be up, some will be down, and some will be flat. Some might be breaking out to the upside, some might be crashing, etc. The dispersion of potential outcomes gives an active portfolio manager more opportunity to simultaneously apply a variety of trading strategies suitable for different scenarios.

Active vs. Passive Options Management

The biggest risk to a short or written call position is if the underlying asset increases past the options’ strike price. The party who has written (or sold) a call is obliged to either sell the underlying equity at the predesignated strike price or “make up the difference” and provide the holder of the call option the cash value of the gains past the strike price. Either way, the short call position surrenders the gains in the asset.

Given this is the primary risk to a call writing strategy, it would seem logical that anyone writing calls would attempt to close out or modify the trade before being on the hook for potential losses. However, that isn’t always the case.

Many call writing strategies follow a passive, systematic process where the call is written, the premium is collected, and then the portfolio manager simply sits back and waits to see what happens. If the underlying asset shoots past the strike price and the strategy forgoes the gains in the asset, well, so be it. A passive strategy does not trade out of these scenarios.

Moreover, a passive strategy might not change the terms of their trade. A theoretical passive call-writing strategy might simply write a call option 3% out of the money with a monthly expiration and just repeat that process regardless of market conditions.

A strictly passive strategy might not take into consideration:

- volatility conditions,

- price momentum,

- reversion to the mean,

- the relative value between puts and calls (i.e. bearish vs. bullish sentiment), or

- time horizons.

All these factors are important in determining the value of an option, but a passive strategy has made the strategic choice to ignore them.

An ‘Active-Active’ Approach to Derivative Income

Swan obviously believes these factors matter. These factors should dictate whether or not it is a good time to write calls, the expiration window of the call, the amount traded, and how long the position should be held. We believe actively managing these risks and profit opportunities adds value to a call writing strategy.

Swan Enhanced Dividend Income ETF [ticker: SCLZ]

All these design decisions were instrumental in the construction of the Swan Enhanced Dividend Income ETF. Swan follows an “active-active” approach where both the underlying equity and option positions are actively managed.

Underlying Equity Portfolio – Swan has partnered with O’Shares Investments to develop a focused index consisting of about 50 equities as the starting point for the ETF. These stocks have been selected for their quality growth metrics and have a history of growing their dividend distributions. Another factor driving the equity index is the option-writing potential of the stocks. All positions must have a healthy options chain so that Swan can write calls on those positions.

Options Written – Swan writes call options on the individual equities within the portfolio, not a broad-based index like the S&P 500 or the Nasdaq 100. While it is certainly more work to manage a portfolio of short calls on individual names rather than single calls on an index, Swan believes the profit potential of individual equity call options more than justifies the effort.

Management of the Options – Swan actively manages the short call positions. This is done to optimize the upside potential of the stocks held in the fund. This active management could mean:

- At any given point in time, there might be some positions without calls written against them.

- The strike prices will be of varying distance from the current prices.

- The time to expiration of the short calls will vary.

- The time that the trade is open will vary. Swan might close out a position quickly for either profit-taking or loss-mitigation purposes.

Swan fully acknowledges that no trading strategy, active or passive, will work better in every single environment. There will be periods when one will do better than the other. Also, a “set it and forget it” passive strategy is certainly easier to manage. However, Swan built the Swan Enhanced Dividend Income ETF upon the belief that the active management of equities and options better positions investors for total return, sustainable income, and capital appreciation.

Marc Odo, CFA®, FRM®, CAIA®, CIPM®, CFP®,

Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. His responsibilities also include producing most of Swan’s thought leadership content. Formerly Marc was the Director of Research for 11 years at Zephyr Associates.

Important Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The S&P 500 Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency). Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. Swan’s investments may consist of securities which vary significantly from those in the benchmark indexes listed above and performance calculation methods may not be entirely comparable. Accordingly, comparing results shown to those of such indexes may be of limited use. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 044-SGI-021723

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All