Key takeaways:

- Markets have pushed back the timing and pace of rate cuts, but this has generated fresh opportunities to lock in attractive yields in fixed income.

- Core inflation is approaching central bank targets, and a recognition that policy acts with lags should steer major central banks down the rate-cutting path.

- Fixed income markets are broadly pricing in a soft landing, and investors should look for areas that offer value but do not get severely battered in a harder landing.

There is a renowned joke about a lost tourist in Ireland who asks one of the locals for directions to Dublin. The local farmer frowns and replies, “Well, sir, I wouldn’t start from here if I were you.”

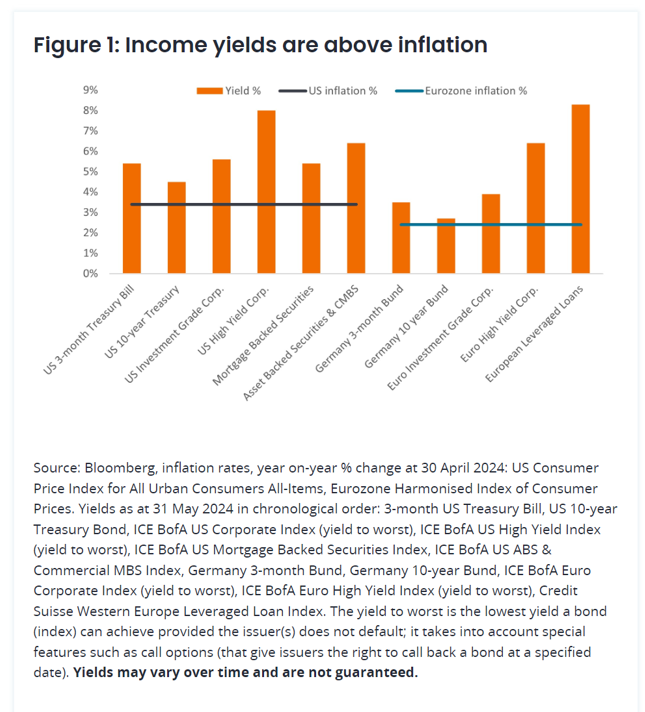

Fixed income investors a few years ago would have sympathized. Yields were near all-time lows and vulnerable to upward moves, and bonds were offering little in the way of income. Today’s fixed income market looks very different. Yields are at levels that currently pay above inflation and offer the prospect of capital gains if rates decline.

Thus, for those seeking attractive returns, you can start from here. We see strong prospects for both healthy income and some additional capital appreciation in the next six months.

False starts, but easing is underway

Fixed income markets have been fixated on the timing of interest rate cuts. This requires not just a focus on economic and inflation data, but on the policymakers themselves. No one is looking to central banks for their forecasting acumen, which has been deplorable. Rather, markets look to central banks because they set policy.

In a clear admission of their lack of clairvoyance, central banks have become highly “data-dependent” and reactionary. The issue is that the key metrics they fixate on – inflation and employment – are lagging indicators. This is compounded by the fact that their policy tools also work with a lagged effect. Sticky inflation has led to markets pricing out expected rate cuts, with the US Federal Reserve (Fed) forecast to do one or two rate cuts this year, down from six to seven at the beginning of the year.1 This approach is a recipe for a policy mistake if inflation does not behave over the coming months.

The corollary of delayed rate cuts has been an extended opportunity for fixed income investors to lock in some attractive yields. Investors are being paid to wait for rate cuts to emerge.

Outside the US, a global rate-cutting cycle is already underway. Rate cuts in emerging markets started in the second half of last year and have since gathered pace. In the developed world, the Swiss National Bank fired the starting gun on rate cuts in March 2024, followed by Sweden’s Riksbank in May and the Bank of Canada and the European Central Bank in June. The regime is shifting.

Is the decline in inflation stalling?

The holdup on rate cuts in the US is due to inflation. Whether it is airline tickets, motor vehicle insurance, or rents, there have been many reasons why the decline in inflation has stalled. In accounting, there comes a time when a company uses the ‘exceptional items’ term a little too often and investors grow skeptical of the strength of a company’s earnings. Should similar cynicism be applied to the Fed and its fight against inflation?

We think not. First, the stalling has occurred at the all-items level, which includes volatile food and energy prices. Core inflation remains on a downward trend. Second, inflation does not move in a straight line, so we should expect the occasional volatility. Third, inflation data is notorious for lags, and at current levels, it is not too far off the Fed’s target. In fact, if the US reported inflation using the Harmonized Index of Consumer Prices measure (as is common in Europe), US inflation would be running at 2.4%.2 Moreover, inflation expectations among consumers remain well anchored at around 3% for the coming year in both the US and the Eurozone.3

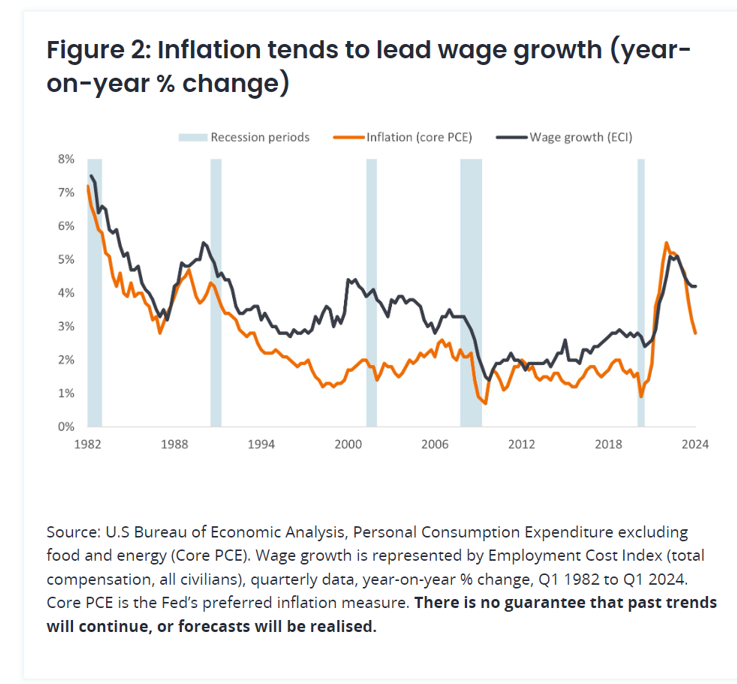

Wage demands are also moderating in most economies. Research suggests that wage growth tends to be a symptom of inflation rather than causing it.4 The decline in inflation is therefore likely to underscore the trend down in wage demands. Patience may be required for a few more months, but the trend remains intact.

Doing nothing is still doing something

As the UEFA Euro 2024 soccer tournament unfolds this summer, one is reminded of some research on goalkeepers and penalty shootouts. Goalkeepers have a tendency to dive in a particular direction to save a penalty, when they would actually save more penalties if they simply stayed in the middle of the goal. This is because goalkeepers feel worse about a goal being scored following inaction (staying in the centre) than following action (jumping to either side).5

Central bankers may be thinking that if the economy is growing modestly, labour markets are healthy, and inflation is contained, why not stay put? After all, central bankers risk a greater reputational loss from allowing inflation to rise than they do from causing economic weakness or unemployment. Yet, they are conscious that their policy also works with lags, so the longer rates are held at current levels, the more financing pressure builds.

We have already seen problems exposed among regional banks last year and more recently among companies with excessive debt levels. Sub-investment grade default rates have only risen modestly, however, and are expected to stay around the low mid-single-digit mark of between 3% to 5% in Europe and the US for the remainder of this year.

The reason defaults have been low is because investors have been willing to lend to companies. The technical backdrop of debt issuers finding ready buyers has been supportive, but part of that rests on the expectation that rates will be lower in the coming year. This encourages investors to lock in yields on issued bonds now while they are relatively high, while taking comfort from the fact that lower rates in the future should be supportive for the economic and corporate backdrop.

Everything in moderation

Outside of a major growth surprise or inflation shock, we struggle to see major central banks raising rates. The risk to rates markets therefore is that cuts are fewer and slower than expected. As such, we prefer European markets over the US where Europe’s relatively weaker economy offers more visibility of a lower rates trajectory.

For many fixed income assets, a slower rate-cutting path is not necessarily a bad thing if engendered by strong – but not too strong – economic growth, which is supportive for earnings and cash flows. With an economic backdrop of resilient, albeit moderating, growth in the US, a reviving European economy, and less bearishness towards China’s economic outlook, there is the potential for credit spreads to grind tighter. Among corporate sectors, we continue to prefer companies with good interest cover ratios and strong cash flow and see value opportunities in some of the areas that have been out of favour, such as pockets of real estate.

We recognize, however, that credit spreads in aggregate are near their historical tights, leaving little cushion should the corporate outlook take a turn for the worse. With that in mind, we see value in diversification, particularly towards securitized debt, such as mortgage-backed securities, asset-backed securities, and collateralized loan obligations. Here, misconceptions towards these asset classes, combined with a hangover from rates volatility, have meant spreads and yields on offer look compelling. Yields in the securitized sectors are more attractive on a historical basis and more likely to stay out of trouble in a more severe slowdown.

The elephant in the room

It would be remiss not to mention politics, given the second half of the year will see the defining event of numerous elections, including one for a US president. This could shine a spotlight on government debt levels and fiscal profligacy – where France has become the latest sovereign bond issuer to suffer a downgrade.6 It could also reawaken concerns around protectionism and tariffs on trade, given that easing of supply chain bottlenecks has been instrumental in helping to bring down inflation from its post-COVID highs.

Similarly, the conflicts in Ukraine and the Middle East could take unpredictable turns. Elevated political risk in the second half of 2024 should draw investors to assets that are traditionally lower risk, such as bonds, which offer some protection against a more pronounced slowdown or escalation in geopolitical risks.

In summary, the narrative of 2024 being a year of policy easing remains intact, even if some central banks have kept markets waiting. Rate cuts offer the potential for capital gains from fixed income, but investors should not overlook the second word in the name of the asset class. Right now, there is plenty of income on offer.

IMPORTANT INFORMATION

1Source: Bloomberg, World Interest Rate Projections, 1 January 2024 and 1 June 2024. There is no guarantee that past trends will continue, or forecasts will be realised.

2Source: Bloomberg, Eurostat United States HICP All Items, at 31 March 2024 (latest available figure).

3Source: New York Fed Survey of Consumer Expectations (April 2024), one year ahead inflation expectations, European Central Bank Consumer Expectations Survey (April 2024), median inflation expectations over next 12 months.

4Source: “Do higher wages cause inflation?”, Magnus Jonnson and Stefan Palmqvist, Sveriges Riksbank Working Paper Series no 159, April 2004, “How much do labour costs drive inflation?” Adam Shapiro, San Francisco Fed, 30 May 2023.

5Source: “Action bias among elite soccer goalkeepers: The case of penalty kicks”, Bar-Li, Michael, and Azar, Ofer H. and Ritov,, Ilana and Keidar-Levin, Yaelr and Schein, Gailt, Ben-Gurion University of the Negev and Hebrew University of Jerusalem, Israel.

6Source: S&P Global Ratings, France downgraded from AA to AA-, 31 May 2024.

3-Month US Treasury is U.S Treasury bill that will mature 3 months from the date of purchase.

10-Year Treasury is a U.S. Treasury bond that will mature 10 years from the date of purchase.

The ICE BofA US Corporate Index tracks US dollar denominated investment grade corporate debt publicly issued in the US domestic market.

The ICE BofA US High Yield Index tracks US dollar denominated below investment grade corporate debt publicly issued in the US domestic market.

The ICE BofA US Mortgage Backed Securities Index tracks US dollar denominated fixed rate mortgage pass-through securities publicly issued by US agencies Fannie Mae, Freddie Mac and Ginnie Mae in the US domestic market.

The ICE BofA US ABS and CMBS Index tracks US dollar denominated investment grade fixed and floating rate asset backed securities and fixed rate commercial mortgage backed securities publicly issues in the US domestic market.

3-Month German Bund is a German government bond that will mature 3 months from the date of purchase.

10-Year German Bund is a German government bond that will mature 10 years from the date of purchase.

The ICE BofA Euro Corporate Index tracks EUR denominated investment grade corporate debt publicly issued in the eurobond or Euro member domestic markets.

The ICE BofA Euro High Yield Index tracks EUR denominated below investment grade corporate debt publicly issued in the euro domestic or Eurobond markets.

The Credit Suisse Western European Leveraged Loan Index is designed to mirror the investable universe of the Western European leverage loan market. Loans denominated in US%$ or Western European currencies are eligible for inclusion in the index.

Asset-Backed Securities (ABS): A financial security that is backed (or collateralised) with existing assets (such as loans, credit card debts or leases), usually ones that generate some form of income (cash flow) over time.

Cash flow: The net amount of cash and cash equivalents transferred in and out of a company. Or a general term for the movement of money from one account to another.

Commercial Mortgage-Backed Securities (CMBS) are fixed income investments backed by mortgages on commercial properties rather than residential real estate.

Core Personal Consumption Expenditure (PCE) Price Index is a measure of prices that people living in the US pay for goods and services, excluding food and energy. It is a measure of inflation.

Credit rating: A score given by a credit rating agency such as S&P Global Ratings, Moody’s and Fitch on the creditworthiness of a borrower. For example, S&P ranks investment grade bonds from the highest AAA down to BBB and high yields bonds from BB through B down to CCC in terms of declining quality and greater risk, i.e. CCC rated borrowers carry a greater risk of default.

Credit spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Fiscal policy: Describes government policy relating to setting tax rates and spending levels. Fiscal consolidation or discipline is when a government seeks to reduce its borrowing by spending less or raising taxes, fiscal easing or largesse is the opposite.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Inflation: The rate at which prices of goods and services are rising in the economy. Core inflation typically excludes volatile items such as food and energy prices. A common measure for inflation is the Consumer Price Index (CPI).

Interest cover ratio: This ratio reflects how well a company can pay the interest due on outstanding debt. It is typically calculated by dividing a company’s earnings before interest and taxes but its interest expense during a given period.

Investment-grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Leverage: This is a measure of the level of debt in a company. Net leverage is debt (minus cash and cash equivalents) as a ratio of earnings (typically before interest, tax, depreciation and amortisation). A leveraged company is typically one with high borrowings.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. Shorter-dated bonds generally mature within 5 years, medium-term bonds within 5 to 10 years, and longer-dated bonds after 10+ years.

Monetary policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money. Monetary loosening refers to central bank activity aimed at reinvigorating the economy by cutting interest rates.

Mortgage-Backed Securities (MBS): A security which is secured (or backed) by a collection of mortgages. Investors receive periodic payments derived from the underlying mortgages, similar to the coupon on bonds.

Recession: A significant decline in economic activity lasting longer than a few months. A soft landing is a slowdown in economic growth that avoids a recession.

Refinancing: The process of revising and replacing the terms of an existing borrowing agreement, including replacing debt with new borrowing before or at the time of the debt maturity.

U.S. Treasury securities are direct debt obligations issued by the U.S. Government. The investor is a creditor of the government. Treasury Bills and U.S. Government Bonds are guaranteed by the full faith and credit of the U.S. government, are generally considered to be free of credit risk and typically carry lower yields than other securities.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For equities, a common measure is the dividend yield, which divides recent dividend payments for each share by the share price. For a bond, at its most simple, this is calculated as the coupon payment divided by the current bond price.

Yield to worst (YTW) is the lowest yield a bond can achieve provided the issuer does not default and accounts for any applicable call feature (i.e., the issuer can call the bond back at a date specified in advance). At a portfolio level, this statistic represents the weighted average YTW for all the underlying issues.

Volatility measures risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Janus Henderson Investors

Read more commentaries by Janus Henderson Investors