The Asian high-yield market is evolving faster than investor perceptions.

After a turbulent few years caused by the shakeout in China’s property sector, the Asia high-yield bond market has found a new equilibrium based on sound fundamentals, attractive valuations and strong returns. We think it’s time for investors to consider its growth potential and diversification benefits.

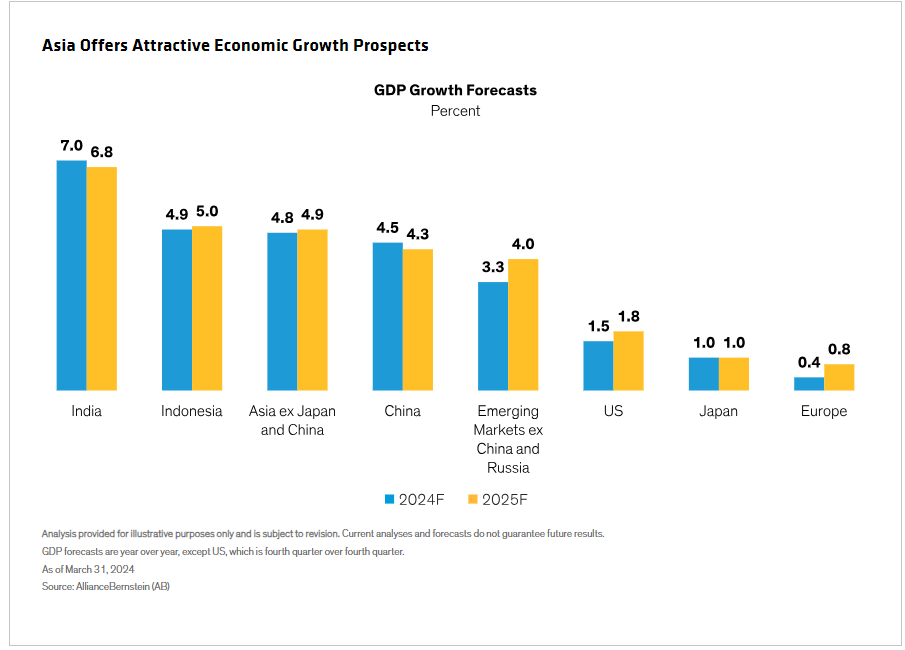

China may no longer be the global growth powerhouse it once was, but its GDP growth—for now and the foreseeable future—remains well ahead of Western economies’, as does the growth of India, Indonesia and Asia generally, presenting a significant opportunity for global investors (Display).

High-yield bond investors may view the prospect with mixed feelings, given the Asia high-yield market’s poor performance after Chinese real estate companies began defaulting on their debt in 2021. But the market has made a remarkable recovery, outperforming its counterparts with a year-to-date (through May 31) return of 9.1% compared with 1.6% for the US high-yield market, 3.2% for European high-yield, and 2.8% for the global high-yield market.

But returns tell only part of the story. The Asia high-yield market has changed structurally, offering investors a much-improved risk-reward profile. To understand these changes and what they mean, it helps to know a little about the market’s recent history.

China’s Presence in the Index Has Shrunk

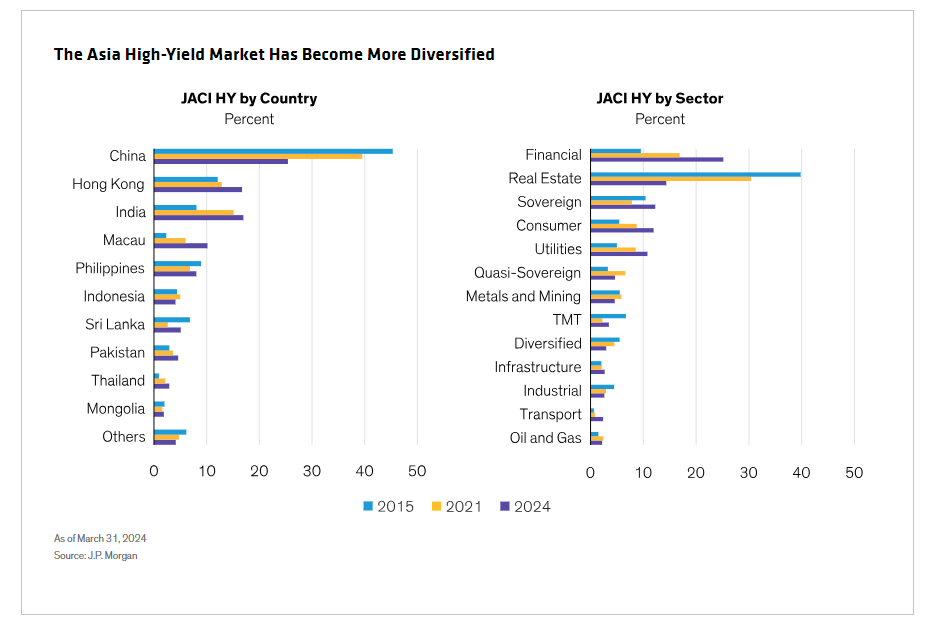

Until a few years ago, investors seeking exposure to high-yielding debt issued by Chinese companies saw the Asia high-yield market as a logical inclusion in their portfolios. At one stage, Chinese companies accounted for as much as 45% of the noninvestment-grade corporate component of the JP Morgan Asia Credit Index (JACI HY). Most of these (35%) were real estate companies.

That all changed in 2021, when China Evergrande Group, one of the country’s biggest property developers, began a series of debt defaults, triggering an industry-wide crisis. The level of Chinese government support for the industry fell short of investors’ expectations, and the attraction of the market evaporated—as did much of the country’s presence in the index. Mainly because of property-company defaults and liquidations, China’s share of the JACI HY fell from 38% in 2021 to 25% by March 2024, while its share of the index’s real estate sector fell from 23% to slightly more than 7%.

Today, the market has a more even balance of countries and sectors. China still dominates, but much less than it used to, and other countries—notably India, Pakistan, Thailand and the special administrative regions of Hong Kong and Macau—now account for more of the index. Among sectors, financials have displaced real estate as the index’s biggest component, and sovereigns, consumer and utilities have increased their shares too (Display).

The increased share of financials in the index—the proportion of financial credits to corporate credits has risen from 11% in 2015 to 22% in March 2024—implies greater stability, as Asian banks have generally high credit quality, many being either owned or supported by their governments. The greater exposure to India, which is expected to lead the region’s growth over the next few years, helps to underpin the market’s outlook for positive returns.

Valuations Compare Favorably with Non-Asia Markets

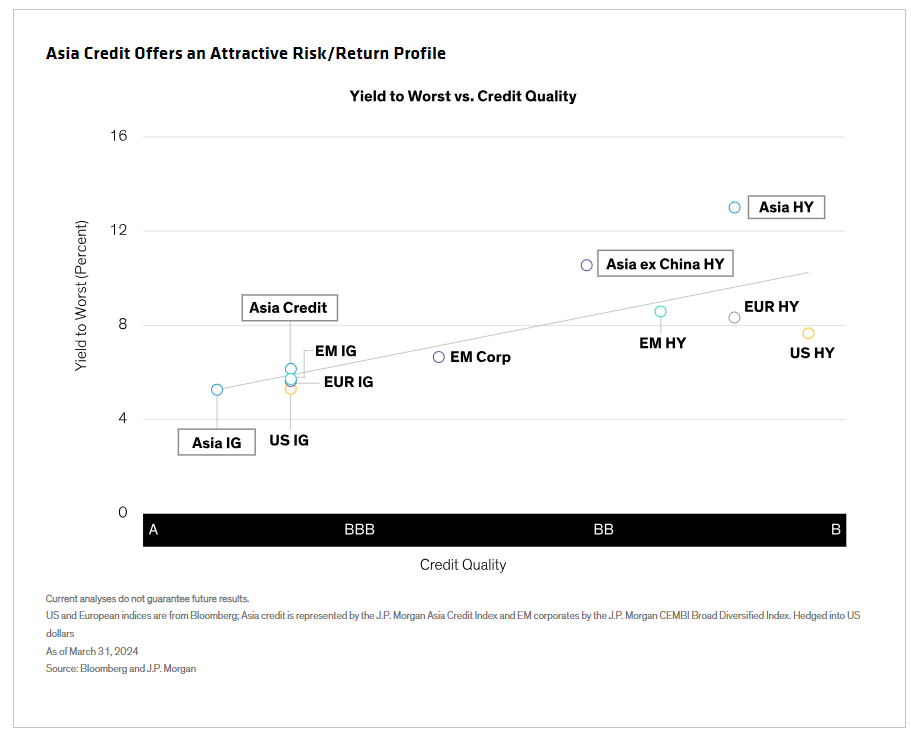

Asia’s high-yield market compares favorably with its global peers on a several measures. From a valuations perspective, its current yield to worst is 13%, significantly higher than emerging-market, US and global high-yield markets (6.7%, 7.7% and 8.1%, respectively). These returns also compare well on a risk-adjusted basis, with credit ratings in each of these markets ranging between BB and B (Display).

After 2019, credit metrics in Asia came under pressure because of COVID, but they remain sound. Earnings before interest, tax, depreciation and amortization (EBITDA) and net income margins fell, while net debt-to-EBITDA rose, from 2.1 times in 2019 to 2.8 times in 2023. The ratio of EBITDA to interest expense also fell but, at 5.6 times, remains healthy. Liquidity (cash to total debt) is lower but remains adequate, in our view, at 30%.

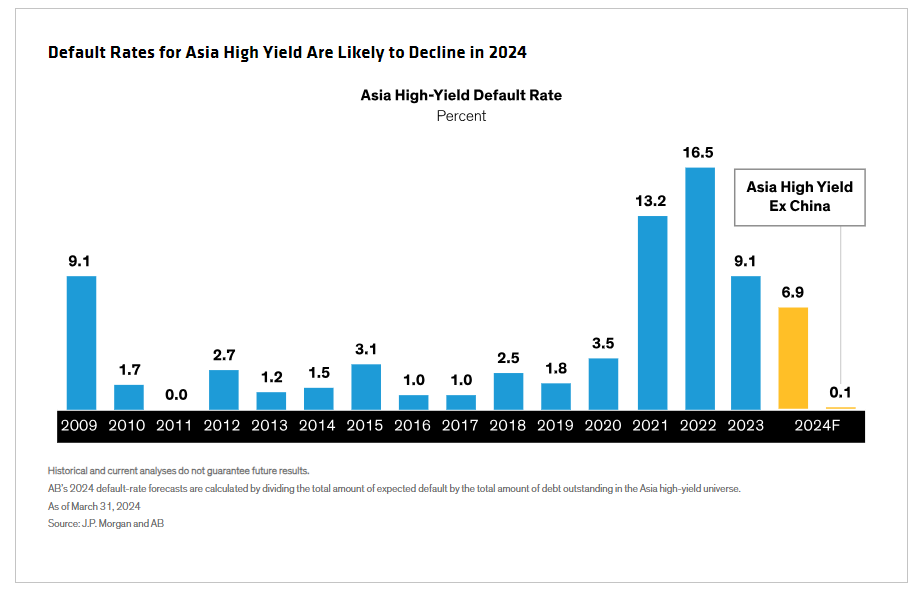

Except for the 2007‒2009 global financial crisis and Chinese real estate defaults from 2021 to 2023, the historical default rate for Asia high-yield has mostly been low. Now that China’s presence in the JACI HY is smaller, and with fiscal and monetary-policy settings supporting Asia’s growth outlook, we expect defaults to continue to fall (Display).

There are other reasons, besides structural changes, for investors to take a fresh look at Asia high yield, in our view.

Diversification and Positive Return Potential

The market’s 13% yield is well above its historical average of 8%, suggesting that current valuations are a good entry point. For now, the high yield provides a cushion against any potential increase in yields and corresponding decline in bond prices; once US rates begin to fall, we expect high-yield markets to attract more attention from fixed-income investors, with the Asian high-yield market among those in the spotlight.

In our view, the Asia high-yield market should continue to grow, despite the past 12 months’ lull in issuance. Asian companies are capital constrained, and as they grow—many of them at rates likely to be several percentage points above the forecast nominal growth rates for their countries—they will need to access US dollar funding through the Asia high-yield market.

With a more balanced risk/reward profile and strong growth prospects, we think the Asia high-yield market offers investors the benefit of diversification and the potential for positive returns.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: Here is the latest news on the bond market, interest rates, and other fixed income sectors.

© AllianceBernstein

Read more commentaries by AllianceBernstein