The second half narrative remains dominated by the path of interest rates, inflation, and the looming election. Morgan Stanley recently discussed key investment themes and opportunities in the second half on their blog, The BEAT.

Emerging Market Debt Opportunities

Many investors currently underweight emerging market debt (EMD) in their portfolios. Current valuations, a macro environment that includes a likely weakening U.S. dollar, and higher funding in emerging market countries than developed markets creates a compelling case for EMD in the second half.

See also: “A Second Half Investor’s Guide: Fiscal Policy and the U.S. Dollar”

“While EMD does not necessarily need a weaker dollar to perform well, the absence of persistent strength is likely to support the asset class,” the authors wrote.

Many emerging market economies currently operate with a reduced debt-to-GDP ratio than their DM counterparts. This is partially attributed to the rapid response of EM central banks to inflation at its initial onset. Early and aggressive policies now leave many EM countries on a potential rate cutting path ahead of DM economies.

What’s more, EMD currently offers attractive valuations and a variety of credit spreads, providing diversification and opportunity. An increase in investor flows into EMD strategies last year and this year could also prove beneficial for bonds.

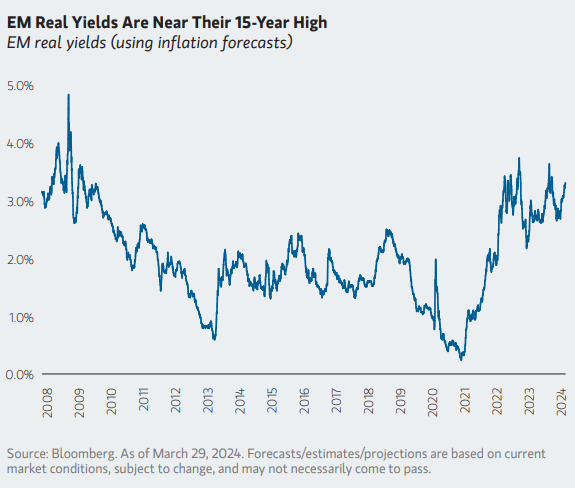

“Perhaps more compelling are the real yields available in the local market segment which remain near their highs of the past 15 years,” noted the authors. “We’ll just add that an environment characterized by high starting real yields, falling inflation and easing monetary policy is usually a good one for bond investors.”

Image source: Morgan Stanley

Second Half Equities

While the U.S. election looms large later this year, Morgan Stanley does not believe it will lead to elevated volatility. Historically, stocks face a challenging time only when an incumbent fails to lead polls coming out of summer conventions. As both candidates have been president previously, familiarity may result in less equity strain.

“Reelection years are good for stocks normally for a reason that certainly applies this year as well,” wrote the authors. “Presidents running for reelection prime the economy with fiscal spending.”

Beyond the election, broad indexes are generally predicted to end the year higher. That rise will likely not be without volatility, however.

Predicting earnings with any degree of accuracy remains a complicated affair for strategists, particularly in the last two years. That said, 2025 consensus earnings projections rose from the beginning of year to now, from $275.19 to $278.87 as of the end of May according to FactSet data. This upward trend leads to a likelihood of “a year-end for the S&P 500 closer to 6,000 than 5,000 while using 2025 estimates,” the authors predicted.

However, investors should keep an eye to volatility in the second half. Equities generally fall approximately 10% at least once a year and the S&P last dropped 10% or more in the fall of 2023. Morgan Stanley predicts a possibility of this as early as late summer.

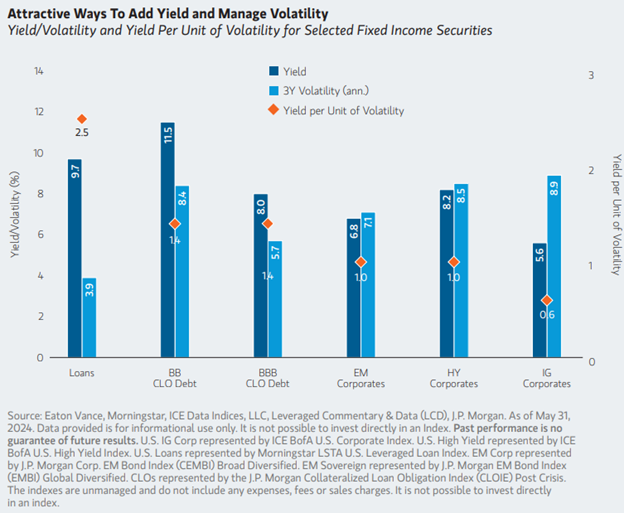

Bank Loans and CLOs

Companies largely weathered interest rate hikes, relying on locked-in, lower interest loans as well as the ability to pass on costs to consumers. A rate cutting regime will certainly boost margins, but “today’s all-time-high stock market and all-time-low credit spreads in many bond asset classes already reflect the positivity,” the authors noted.

Investors looking for pockets of opportunity would do well to look to bank loans in the second half. With absolute yields that rival long-term equity returns alongside collateralized loan obligation (CLO) yields higher still, it’s an asset class worth consideration.

While much of the credit market currently offers tight spreads, CLOs and bank loans sit only slightly above average.

“When combined with a historically high base rate, distributable income from loans is at levels we haven’t seen in over a decade,” the authors explained.

Image source: Morgan Stanley

Continued Rise of Alternative Investments in the Second Half

Alternatives proved attractive in the wake of stock and bond underperformance in 2022. As volatility and uncertainty persisted, these low correlation asset classes continue to draw investors.

Private credit initially proved popular as borrowers sought out private lenders in the wake of public market new issuance challenges. Inflows as investors seized the opportunity brought prices closer to historical averages.

“However, all-in yields in today’s market, especially with the potential for a higher-for-longer rate scenario, are considered attractive,” explained the authors. Should rates decline, leverage will likely improve as equities boost recovery.

Hedge funds also benefited in the market environment of the last year. Dispersion amongst single stocks creates alpha opportunity for long and short positions. Derivative strategies will likely continue to capitalize on alpha generation from equity dispersions and credit fundamentals.

Of particular note, Morgan Stanley sees opportunity within the middle market of private equity and real estate looking ahead.

“Valuation adjustments in these asset classes have been significantly slower, as deal volumes have been very low,” the authors noted. “When transaction volumes recover more broadly, we expect to see further evidence of price correction and attractive entry valuation.”

For more news, information, and analysis visit The ETF Yield Channel.

A message from Advisor Perspectives and VettaFi: Join us on July 25 for the Q3 Fixed Income Symposium, where advisors will gain insights into essential fixed income strategies and market trends to navigate 2024's challenges.

Read more commentaries by VettaFi