The Drivers of Active ETF Adoption

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe’ve been marveling at the traction actively managed ETFs are enjoying this year. As a category, we’ve seen active ETFs take in about 1/3 of all net asset inflows year-to-date. That is an impressive haul by historical standards. Active management in the predominantly passive ETF market – only about 7% of all U.S.-listed ETF assets today sit in active ETFs – is becoming more and more entrenched, especially in some categories and asset classes.

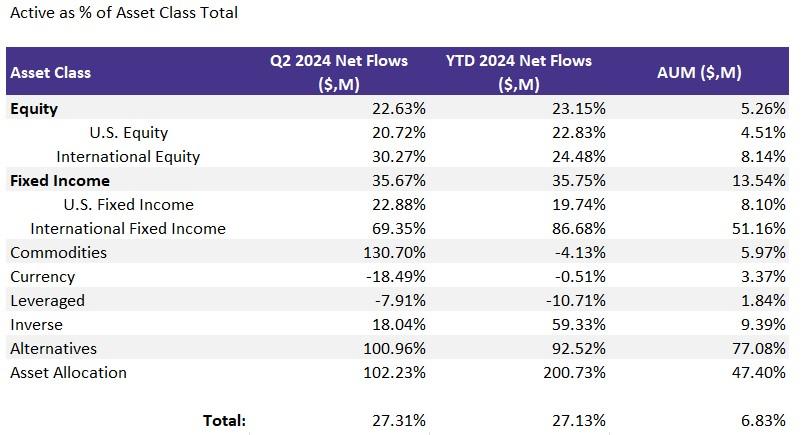

Consider the table below:

This looks at asset flows for both the second quarter and the first half of 2024. It shows that demand for active management in ETFs as a percentage of asset class totals is robust. However, it’s not uniformly dispersed.

Asset Class Adoption Dispersion

Today, the majority of assets sitting in alternative ETFs are in funds run by active managers. More than half of assets invested in international fixed income ETFs are in actively managed strategies. Fixed income, as a broad asset class, has a bigger active management footprint than equities, broadly speaking.

Earlier this week, I had the opportunity to dive into some of this data and explore the 20 most popular active ETFs this year – the ones that are leading the asset creation haul – with ETF Store’s Nate Geraci. You can listen to that conversation in this episode of the ETF Prime podcast here.

Where Active Adds Value

But as we ponder the future of active management in ETFs, let’s consider where investors are finding real value in active management today.

From a flows perspective - if we follow the money - the data suggests that active is delivering value on three fronts:

- Income generation.

- Focused risk management.

- Alpha at a low cost – cost is key.

The pursuit of alternative sources of income, be it in the form of options premium, flexible income portfolios, and unique categories like CLOs, has been a big story in the past year. An uncertain interest rate environment and still-fresh scar tissue associated with poor performing fixed income assets have been strong catalysts in the hunt for “other” types of income. A roster of active ETFs has delivered just that, and providers like JP Morgan, Janus Henderson, and Fidelity, among others, have shined in this space.

On that same note, targeted risk management tools have found a following in a market of narrow leadership and uncertain risks. Take, for instance, the amount of product development we've seen in the structured protection, defined outcome space by providers such as Calamos Investments and Innovator ETFs, among others. These active ETF solutions have made capital preservation an easy thing to implement. Market participation even for the most loss-averse among us is easily done with active ETFs.

The alpha generation story has been a little trickier. We have seen big asset-gathering success stories where big name-brand expertise meets low-cost active management. Firms like Dimensional and Avantis (American Century), for example, are offering active ETFs that are building block, core-type funds that are growing quickly because they bring to the table their well-known portfolio management expertise at attractive prices.

Dimensional’s active ETF lineup comes with a weighted average expense ratio of 22 basis points; Avantis’ comes in under 25 bps, ETF Think Tank data shows. That’s competitive in an active category where the weighted average ER sits around 40 bps – or $40 per $10,000 invested. Capital Group is another powerhouse in this space. The "high expertise for a low-cost" approach has been working well for those looking to gather assets among alpha seekers.

U.S. Large Cap Growth – An Example

But, more broadly, active adoption is still challenging in some asset classes, such as the U.S. equity category. Only about 4% of the $5.75 trillion invested in U.S. equity ETFs today sits in actively managed ETFs. It hasn’t been easy to displace the dominance of cheap passive access. Some of it has to do with persistence of performance, as SPIVA reports remind us every year. And some of it has to do with the market environment. It's been hard to beat market-cap-weighted equity benchmarks this year.

Consider U.S. large-cap growth. Everyone loves growth right now, but it's been a big story about a few names. Market leadership has been narrow, to put it mildly. Classic market-cap-weighted large-cap growth funds have delivered the goods. A sampling of low-cost market-cap weighted index growth ETFs shows us exactly that. The performance of the Vanguard Growth ETF (VUG), the iShares Russell 1000 Growth ETF (IWF), the Schwab U.S. Large-Cap Growth ETF (SCHG), and SPDR Portfolio S&P 500 Growth ETF (SPYG) has been stellar, and very similar.

These four ETFs each have about 35% of their respective portfolios tied to three stocks: Nvidia, Microsoft, and Apple. Their top 10 holdings – and their allocations – look nearly identical.

Returns in Percentage (%)

When owning the market – or in this case, the large-cap growth category – in low-cost passive wows the bottom line, investors have little incentive to look elsewhere for the typically pricier actively managed fare.

That said, active large-cap growth ETFs are offering unique value add and could make for interesting opportunities going forward.

For example, performance has been strong too among some. The JP Morgan Active Growth ETF (JGRO) and the T. Rowe Price Growth ETF (TGRT) are two examples of big active managers delivering big results. These funds have only narrowly missed the performance of SPYG so far this year.

Returns in Percentage (%)

The narrow disparity among these ETFs is in part due to smaller allocations to market leaders Microsoft, Apple, and Nvidia in both JGRO and TGRT vs. SPYG. Both JGRO and TGRT are also more heavily allocated to financials, healthcare, and consumer discretionary sectors relative to SPYG’s sector tilts.

To be sure, these funds look very similar and are delivering closely aligned results, but their differences in stock and sector allocations lead to disparity in returns and could become meaningful if there’s a change in market leadership and/or a broadening of the rally.

Overlap of JGRO, TGRT, and SPYG – A Lot of Common Ground but Not Identical

Data Source: VettaFi PRO

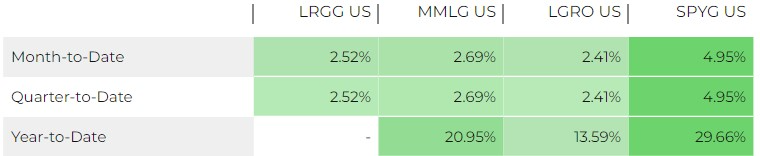

When we take a step further away from market-similar exposures, the bigger the return differences become. For example, consider a random sample of unique active views on U.S. large-cap growth: the Macquarie Focused Large Growth ETF (LRGG), the First Trust Multi-Manager Large Growth ETF (MMLG), and the Level Four Large Cap Growth Active ETF (LGRO). All three are trailing SPYG’s results this year.

Each of these growth ETFs holds Microsoft, Nvidia, and Apple among the top positions. However, their overall mix is very different, reflecting their portfolio managers' views of the opportunity set. For instance:

- LRGG is about high conviction and concentration.

The newcomer from Macquarie is built on the idea that concentration is your friend, but you need a long-term focus on companies that can stand the test of time and disruption. This fund typically owns under 25 names - that's very concentrated. It’s a high-conviction play for high-conviction growth investors.

Beyond the top three holdings, LRGG sees long-term opportunities in names like Intuit, UnitedHealth, and Waste Connections among others.

- MMLG is a multimanager approach.

MMLG from First Trust counts on more than one subadvisor team to make portfolio management decisions. The fund has about 50% of the portfolio tied to technology names, but it rounds its top 10 security holdings with names like ServiceNow, NU Holdings, and Netflix, among others.

- LGRO looks for quality and “behavioral” pricing opportunities.

The fund from SS&C Alps holds the least amount of Nvidia of these three ETFs – only about 4.2% of the total mix. But it brings a focus on quality, keeping an eye on pricing opportunities any time “behavioral inefficiencies,” as the firm puts it, lead to a disconnect between price and real value.

Beyond Headline Performance

Active management has yet to make a significant dent in the predominantly passive U.S. equity ETF category. While it's easy to see why in a market such as we've had, we all know that market leadership can change, and past performance is merely an indication of where we've been, not of where we're going.

Product development across active ETFs has been robust, with lots of value-add ideas coming to market every day. We invite you to stay on top of what active managers are bringing to the table. For a list of growth ETFs, check out our ETF Screener where you can filter your research as broadly or narrowly as you wish.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: Join us on July 25 for the Q3 Fixed Income Symposium, where advisors will gain insights into essential fixed income strategies and market trends to navigate 2024's challenges.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All