Demand growth is cooling, but evidence suggests that overall fundamentals are still sound.

As the economic cycle matures, investors have increasingly become concerned that the US consumer may be starting to struggle. With consumption accounting for roughly two-thirds of economic activity, signs of stress among consumers could signal the start of an economic downturn, or even a recession.

Signs of Strain…and Changing Spending Patterns

We do see signs that consumers face more financial stress than they have over the past few years. After all, households have largely eroded their savings stockpiles from the pandemic. This naturally increases caution—something corporate America started sensing in the first quarter. It’s still early in the second-quarter earnings season, but the song remains the same: demand is cooling. From an average growth rate of 2.75% in 2023, real personal consumption is down to an annualized 1.9% so far in 2024.

As consumers shift gears in their buying behavior, we’re seeing more strength in spending on services and essentials than on goods, particularly the types of big-ticket goods with longer replacement cycles bought during the pandemic. Think furniture, appliances and grills. Based on personal consumption expenditure data, services spending is growing faster than goods spending, and is almost back to its pre-pandemic share of wallet levels.

Bargain Hunting: An Intensifying Search for Better Value

Shoppers are increasingly value oriented as they browse the shelves, forcing many companies to up their promotional discounts.

Quick-service restaurants are at the forefront of this trend: McDonald’s recently reported declining same-store sales, and is resorting to more discounts to spur restaurant traffic. After hiking prices to keep pace with labor costs, Chipotle highlighted higher price sensitivity in California that hurt business. Lamb Weston, one of the country’s largest french-fry manufacturers, echoed this notion—it called out an evolving operating backdrop driven partly by slower restaurant traffic.

So it seems clear that consumers are tapping the brakes and being more discerning about prices. But we see a theme of conservatism, not collapse—a story we think will continue.

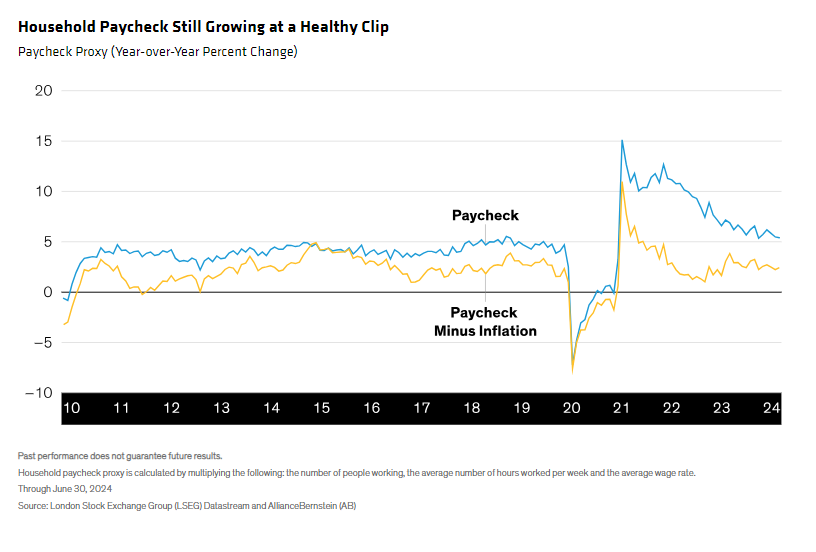

Paychecks and Payments: Kicking the Tires on Fundamentals

Overall, consumer fundamentals remain strong. One way to gauge this is with a proxy for the household paycheck. We can create this by multiplying three data points together: the number of people working, the average number of hours worked per week and the average wage rate (Display). This indicator continues growing at a healthy clip and is outpacing inflation, which should support future consumption.

Source: London Stock Exchange Group (LSEG) Datastream and AllianceBernstein (AB)

Greater price sensitivity among consumers may be good news, too: it suggests that inflation will continue to fall, opening the door for the Fed to cut interest rates in short order. Rate cuts are a critical stabilizer for the economy, helping to reduce financing costs. That’s important, because even with aggregate consumption still solid, lower-income consumers are starting to feel more stress.

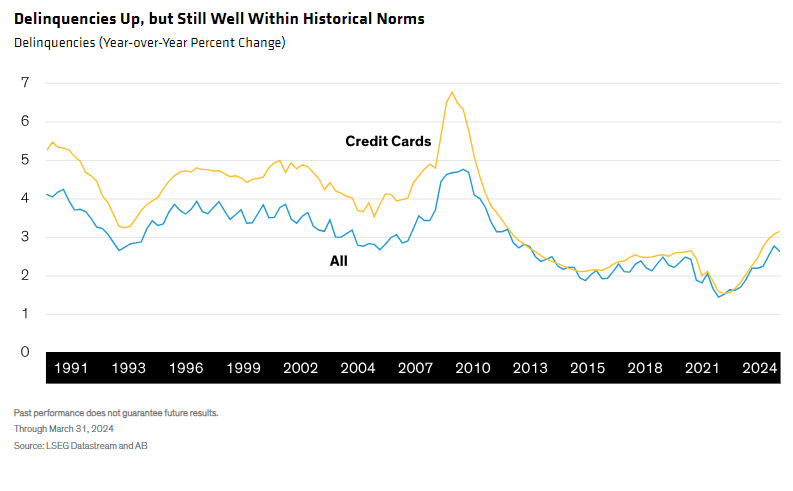

More Borrowing…and an Uptick in Delinquencies

One symptom is the decline in the household savings rate this year, as people rely more on borrowing to make ends meet.

That debt is pricier with the Fed’s policy rate still high and credit card interest rates up. Lower-income consumers are more likely to run credit card balances, so the burden of tighter monetary policy falls heavier on those consumers. On its latest earnings call, Visa described a stable consumption backdrop for higher-income customers and moderating activity from lower-income cardholders. That’s a change from the firm’s prior-quarter commentary that described stability across all income groups.

Based on that observation, it’s no surprise that credit card delinquencies have ticked up (Display). Viewed in a broader context, though, the delinquency rate remains well within historical norms. In fact, the rise in recent months has merely boosted it from all-time lows to something that seems more normal. With the Fed likely to cut rates over the next few quarters, we think borrowing costs will fall too, which should ease the pressure.

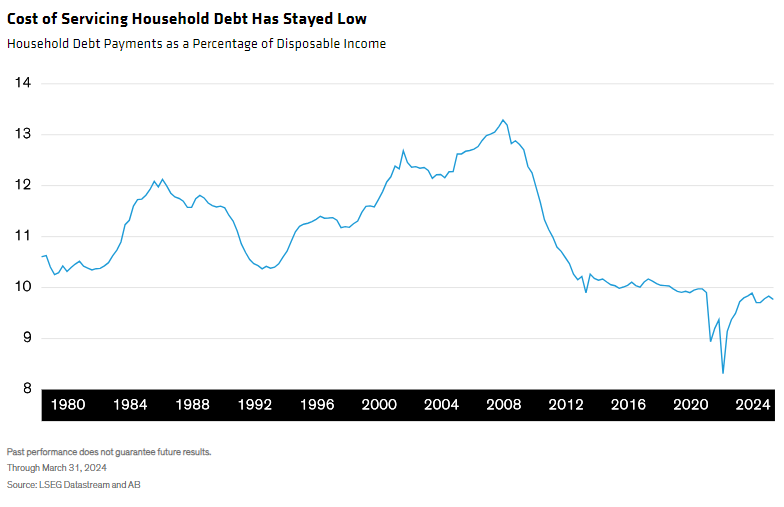

Debt Burdens Have Remained Low…Even with Higher Rates

In an encouraging development, the consumer’s debt-service ratio has remained low even though rates have not yet started to fall. This measure, which quantifies the cost of servicing debt relative to disposable income, has stayed this way for two reasons: income has been strong, and overall consumer credit as a proportion of gross domestic product (GDP) has been trending downward in the post-pandemic era. At about 18% of GDP today, outstanding consumer debt, in aggregate, is below its long-term average.

From a big-picture perspective, it’s understandable that many onlookers worry about signs of strain on the US consumer. However, we don’t believe that they point to a deeper downturn in this vital cog of the economy. Slower demand and greater price sensitivity imply that inflation is likely to fall, pushing interest rates lower. In our view, this should help keep the slowdown manageable, setting the stage for a soft landing that prolongs the economic expansion.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© AllianceBernstein

Read more commentaries by AllianceBernstein