After the Congressional Budget Office's (CBO) recent projections of how U.S. debt will increase, and both political parties' intention to continue large fiscal deficits into a new presidency, fiscal sustainability is a hot, if not raging, topic. Deficits are funded by issuing Treasuries. Many are suggesting a debt crisis1 will happen soon and it is nearly a forgone conclusion that Treasury yields will have to rise to absorb new debt. But, because the interest cost of the debt is still relatively low and there are plenty of buyers, this isn’t a near-term likelihood.

Supply

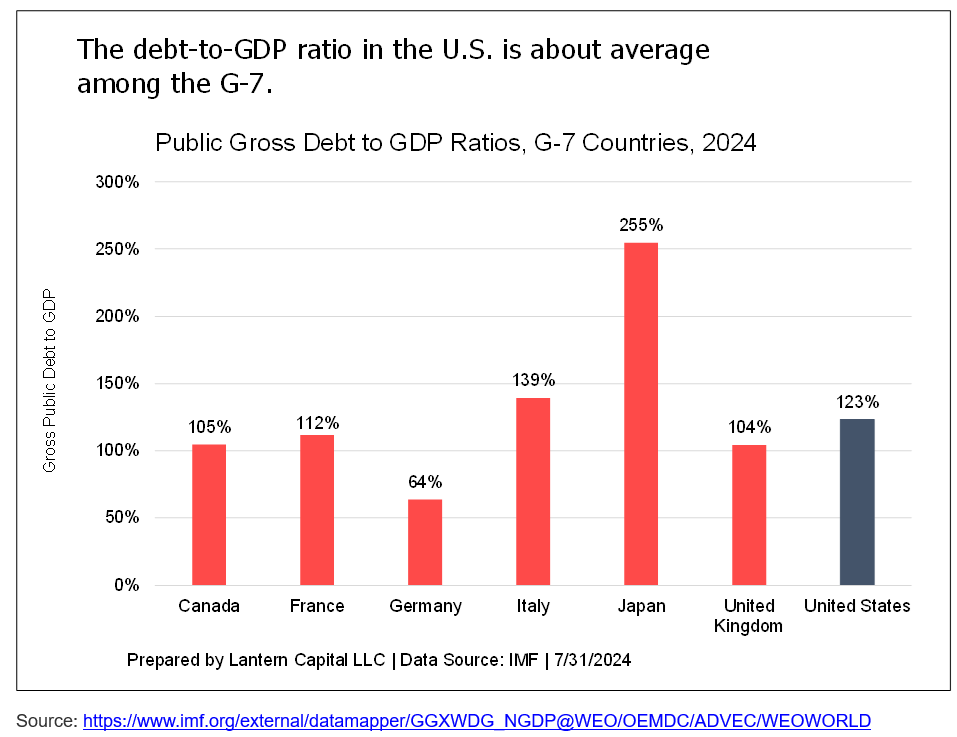

The amount of debt, or the debt-to-GDP ratio, is often the first metric used to gauge a country’s fiscal health. It measures how much public debt the country has in comparison to how much GDP it produces in a year. The lower, the better. These are shown for G-7 countries in the chart below. The U.S. (at 123%) is not near the top (Japan, 255%), but not at the bottom either (Germany, 64%). The U.S. is a little below the average of 129% and can probably handle more debt. The Penn-Wharton Budget Model, a non-partisan economic research initiative, wrote a report last October estimating that the U.S. could likely tolerate a debt-to-GDP ratio of 200%, with 175% being more realistic, and assuming financial markets believe deficits will eventually be reduced.

A ratio of 100% is often mistaken as a practical limit; of which anything over it implies leverage. But the debt-to-GDP ratio is akin to a mortgage amount compared-to yearly income. If 100% were a limit, none of us could get a mortgage for more than our yearly income. In economic parlance, the debt is a "stock" amount and the GDP is a "flow" amount, apples and oranges over time, but useful to compare between countries and over time. A more apt ratio to describe the inherent credit-worthiness of the country, is that the U.S. is financing $35.0 trillion or 23.3% against the country's net wealth of $150.1 trillion (Fed Z.1, B.1 table); not out of bounds.

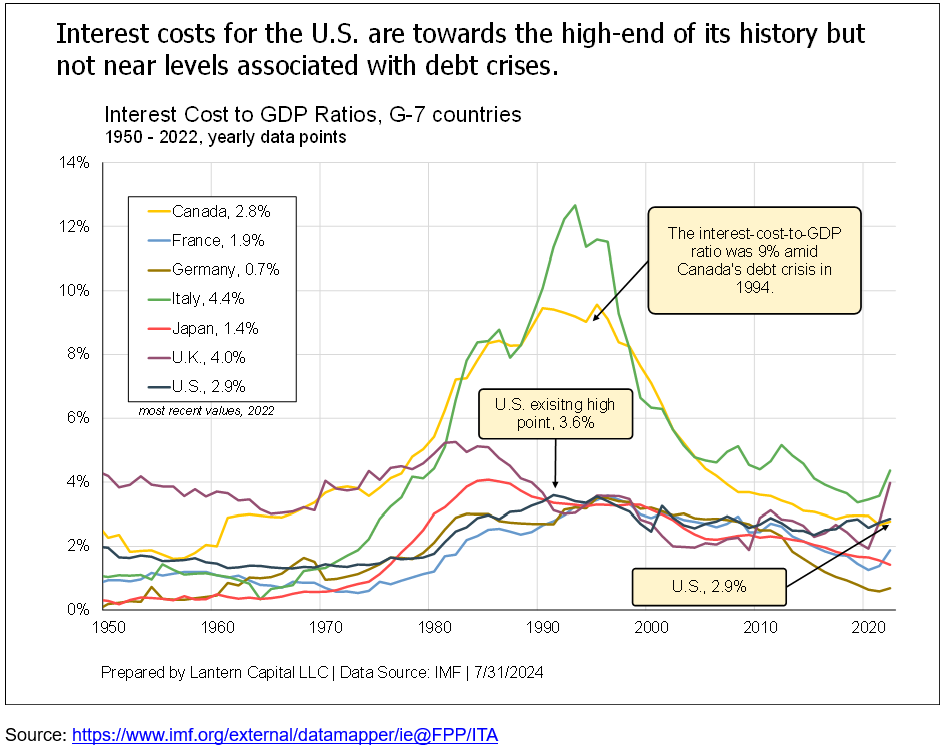

The debt-to-GDP ratio, however, misses an important part of the issue, which is how much the interest costs to the country. This is where the U.S. has a sooner problem. Big-economy reserve currency countries (essentially the U.S., Japan, and Germany) have buyers lined up to purchase their debt, allowing debt-to-GDP ratios to rise to enormous levels, but only if interest costs are low enough. Japan has a debt-to-GDP ratio of 255%, more than twice that of the U.S., but it has likely only been able to get this high because it is financed at low rates from their decades of deflation. Surprisingly, with all of its debt, Japan has an interest-cost-to-GDP ratio of just 1.4%, second to lowest of the G-7 (see chart below.)

The interest-cost-to-GDP ratio combines the average interest rate on the debt with the amount of debt to be a better overall indicator of fiscal health and proximity to a debt crisis than the debt-to-GDP ratio. Debt-to-GDP ratios don’t seem to correlate with debt crises. Historically, investors become concerned debt won't be paid back once interest costs rise too much as a percent of the economy, threatening a debt spiral where more debt causes higher rates which causes higher interest costs which requires more debt. Treasury Secretary Janet Yellen recently discussed the interest cost of the debt. In her 6/24/2024 interview with Yahoo Finance, she said,

"I think the most important metric in judging sustainability is the interest cost of the debt and the interest cost of the debt, even with higher interest rates, is at normal historical levels. It is something that if it stays here, if we engage in deficit reduction so that it stays at this level, I think we will be on a fiscally sustainable course."

"Normal historical levels" is generous. The interest on the debt in the U.S., at 2.9% of GDP (and 14.4% of government revenue), is towards the high-end of its history, but still below levels it got to in the early 1990's after the high rates of the inflationary 1970's and 1980s. That high level of 3.6% in 1991 didn't cause a debt crisis; interest rates were falling from the 1990-91 recession and the dollar was fairly stable. The debt crisis in Canada in 1994-1995 was associated with levels much higher; around 10%. The U.K.'s short debt crisis in 2022, happened with the U.K.'s interest-cost-to-GDP ratio around 4% but this crisis had more to do with how extreme and hasty Liz Truss' tax-cutting budget proposal was. The Congressional Budget Office projects it will take 10 years for the U.S. interest-cost-to-GDP ratio to rise to 4.1%2.

Demand

Treasuries naturally have demand because they are the most-trusted asset in the world to store large amounts of capital. This is because the U.S. is the biggest economy in the world, has political continuity for 248 years, is well organized (rule of law and institutions), has no capital controls, and has the heavily utilized U.S. Dollar. No other country comes close to checking all those boxes. Treasuries are the best deposit bank in the world per se; with no FDIC insurance needed, no fees, and a great yield. Many individuals have learned this over the last year with Treasury bill returns greatly exceeding what banks pay. 54% of the total or $6.8 trillion of foreign exchange reserves are held in the U.S. Dollar, and the Dollar is a party to 88% of global FX transactions (April 2022, BIS), suggesting how big its role is in global trade. Large amounts of cash in dollars usually end up being invested in Treasuries.

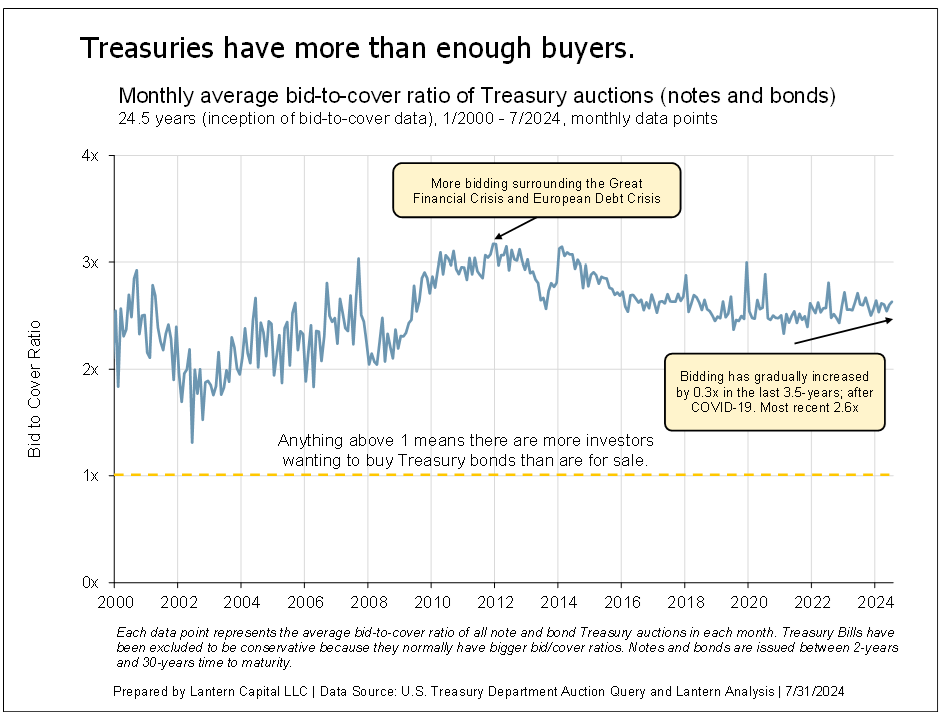

Buyers of Treasuries at auctions are plentiful, with an average of 2.6-times as many bidders to how much is available at auctions for notes and bonds in July 2024 (maturities 2-years and longer.) Treasury bills, which have maturities of 1-year or less, are higher. While this is somewhat structural by the nature of the primary dealer system, bidding has risen in recent years showing increased demand (see chart below.) There have been no Treasury auctions (bills, notes, or bonds) with a bid-to-cover ratio below two since July of 20174.

An easy way to know that Treasury demand is enough is to notice that the U.S. Treasury isn't marketing Treasuries to Households. U.S. Households (and non-profits, how the data comes) have $123 trillion of financial assets, and just 2% of them are directly allocated to Treasuries5. If the U.S. Treasury needed more demand, you would see advertisements like Japan has done in the last 15 years and the U.S. has done during wartime (below.) Treasuries could also be made Federally tax exempt to encourage more buying. None of this is happening because there isn’t a need.

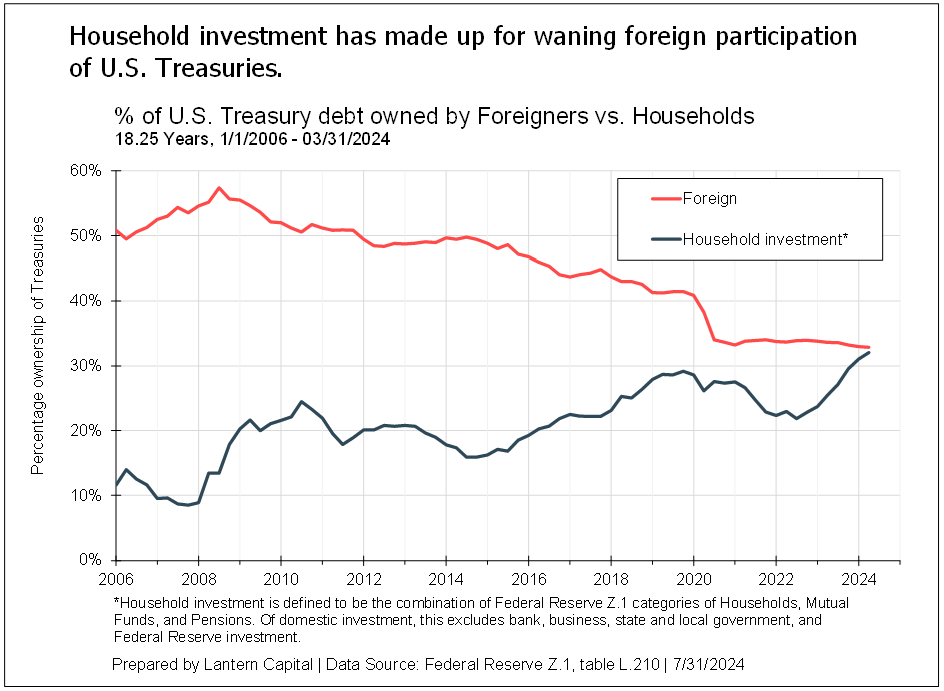

Surrounding the Great Financial Crisis, more than half of U.S. Treasury bonds were owned internationally (see chart below.) In 2009, it became a Wall Street narrative that deficit spending from the Great Financial Crisis was going to cause foreigners (especially China) to abandon Treasuries. This was the 2009 version of what we are going through now. It escalated to the extent that Secretary of State Hillary Clinton spent part of a trip to China reassuring Chinese leaders that U.S. debt was safe.

Eventually, China did reduce their investment in Treasuries. Since 2008, foreign ownership of Treasury bonds has fallen by nearly 25%. The pervasive logic of the last 15 years would’ve suggested the Treasury market would’ve run out of buyers, but it didn't and nobody celebrated. Household investment has picked up the difference without any coercing or discernable effect on Treasury yields.

Unquestionably, public debt growth in the U.S. is much nearer to the end of its capacity than its beginning and hard choices will have to be made within years, not decades to reduce deficits. It is disappointing that large deficit spending is now being used during periods of economic strength. Pro-cyclical deficits that aren't invested for the future (say, infrastructure) bring-forward economic growth that will inevitably have to be paid back. At this point, large deficit spending should be reserved for recessions and emergencies only.

But, outside of the political fracas, U.S. debt fits into a global context that isn't as dire as it is made to sound. The relentless political/Wall Street narrative that too much supply (deficits) or too little demand will lead to higher Treasury yields has been wrong for decades. Imbalanced deficit fear commentary from the press makes it seem that Treasuries are always or will soon be in a bear market; and frankly, that they aren’t safe. The $35 trillion of capital that owns them would disagree. Given reasonable debt statistics and sufficient buyers, Treasury yields will continue to be driven by the outlook for the economy, which makes them the asset with the most opportunity from a slowing or receding economy.

Eric Hickman, Founder, Lantern Capital LLC, Denver, CO

References:

1 A debt crisis is when sovereign bond yields rise outside of the normal movement from the economy. Traders sell them for credit reasons, rather than future growth reasons and often until fiscal policy is addressed. Developed-economy examples include Canada in 1994, Portugal, Italy, Ireland, Greece, and Spain (PIIGS) in the 2010’s, and the U.K. in 2022.

2 This IMF time series is used because it includes data for other countries than the U.S. The series is updated through 2022. The most recent number for the U.S. from this IMF series (2.9%) is somewhat higher than the number the CBO uses of 2.4% as-of 2023. The CBO projects the interest cost to GDP ratio to rise from 2.4% to 4.1% over the next 10 years.

3 Lantern analysis of GDP in U.S. Dollars, from the World Bank, accessed 7/29/2024

4 Lantern analysis of Treasury Auction Data, accessed 7/29/2024

5 Lantern analysis on the B.101 table of the Fed's Quarterly Z.1 report for Q1 2024. This group holds more Treasuries indirectly through pensions and mutual funds but those figures aren't isolated.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Lantern Capital

Read more commentaries by Lantern Capital