Executive summary:

- The MPC has decided to reduce the bank rate from 5.25% to 5.00% despite high June services inflation reaching 5.7% year-on-year.

- A majority of five members opted for a cut of 25 basis points, while the remaining four advocated for unchanged interest rates.

- Although the decision was expected by most analysts, bond markets still reacted to the announcement at noon today. The yield of 10-year UK gilts fell to a low of 3.91% after the decision.

The members of the Bank of England’s Monetary Policy Committee (MPC) are probably not intimately familiar with Taylor Swift’s back catalogue. If they were, Swift’s hit “Cruel Summer” may have been ringing in their ears when cutting rates today for the first time since March 2020.

Puns aside, the MPC decided to reduce the bank rate from 5.25% to 5.00% despite high June services inflation of 5.7% year-on-year (partly driven by prices for hotels and live music) that some observers had attributed to Swift’s “Eras” tour coming to the UK that month.

A majority of five members1 opted for a cut of 25 basis points, while the remaining four advocated for unchanged interest rates. At the previous meeting in June, the MPC had voted 7-2 to hold rates steady. Today’s decision was expected. Of 60 economists surveyed by Reuters, 49 had predicted the cut. Money market traders had been somewhat less confident, projecting a 60% likelihood of lower rates ahead of the decision.

Recent retail sales and business confidence data revealed sluggishness in UK economic activity, tipping the balance towards a rate reduction. With today’s move, the European Central Bank and the Bank of England (BoE) have started their rate cutting cycles ahead of the U.S. Federal Reserve, which is widely expected to follow suit at their September policy meeting.

UK services inflation impacted by one-offs

Price increases for restaurants and hotels, health, and other services were widely seen as a major stumbling block to starting the easing cycle. Elevated service inflation of 5.7% in June had been meaningfully above the projection of 5.1% from the BoE’s last Monetary Policy Report published in May, but the MPC decided to look through some of the one-off effects. Aside from Taylor Swift fans driving up hotel and concert ticket prices, there were index-linked adjustments to rents and communication services that reveal more about past inflation than current price pressures.

Importantly, the labor market cooling that has been underway for months continues apace and is expected to dampen wage growth, feeding into lower future inflation for services. The unemployment rate rose to 4.4% in the three months ending in May 2024 from a cyclical low of 3.6% in mid-2022. Job vacancies, which are a leading indicator for wage growth and unemployment, have fallen continuously for 24 months.

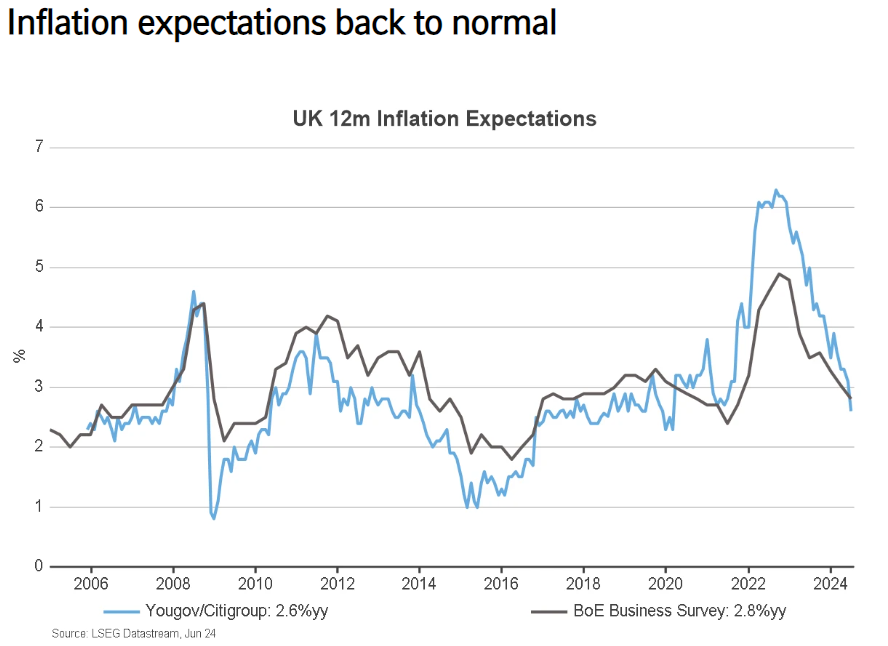

What should also be reassuring to the BoE is the return of inflation expectations to normal levels. As shown in the Chart, the Yougov/Citi survey of consumers and the BoE’s business survey for 12-month ahead inflation expectations are back to 2.6% and 2.8%, respectively—in-line with pre-pandemic levels. The period of very high inflation in 2022-23 has not embedded itself in the psyche of consumers and businesses, making the central bank’s job easier.