Systematic Equity Outlook: Decoding Upside and Downside Risks

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe first half of 2024 in equity markets was characterized by strong headline returns, low volatility, and persistent mega cap tech leadership that underpinned steady momentum factor outperformance.

Now, recent macroeconomic and geopolitical developments along with shifting AI sentiment have raised concerns over whether these dynamics can continue as we look ahead. This quarter, we explore the potential for emerging risks to upend year-to-date trends, and where investors can seek opportunities amid greater uncertainty.

The left tail: geopolitics and trade protectionism

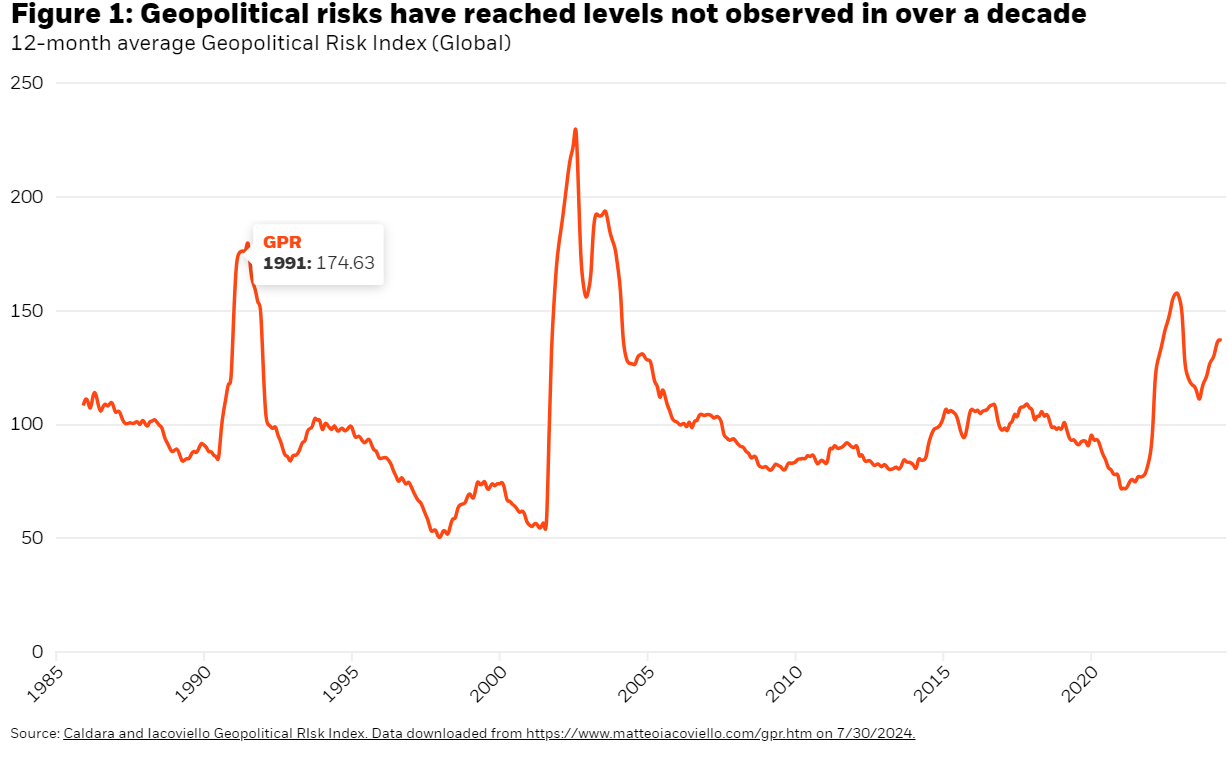

Geopolitical tensions have been steadily rising over recent years on the heels of more frequent global conflicts, trade disputes, and heightened strategic competition. Figure 1 illustrates how global geopolitical risks have reached highs not seen in more than a decade based on an index which measures the volume of monthly news articles related to adverse geopolitical events.

With the US election cycle underway, market focus has shifted to the potential for protectionist trade policies and new regulations to disproportionately impact globally exposed firms. Against this backdrop, we’ve increasingly turned to data-driven analysis that helps decipher which companies are building domestic self-sufficiency and managing geopolitical risks.

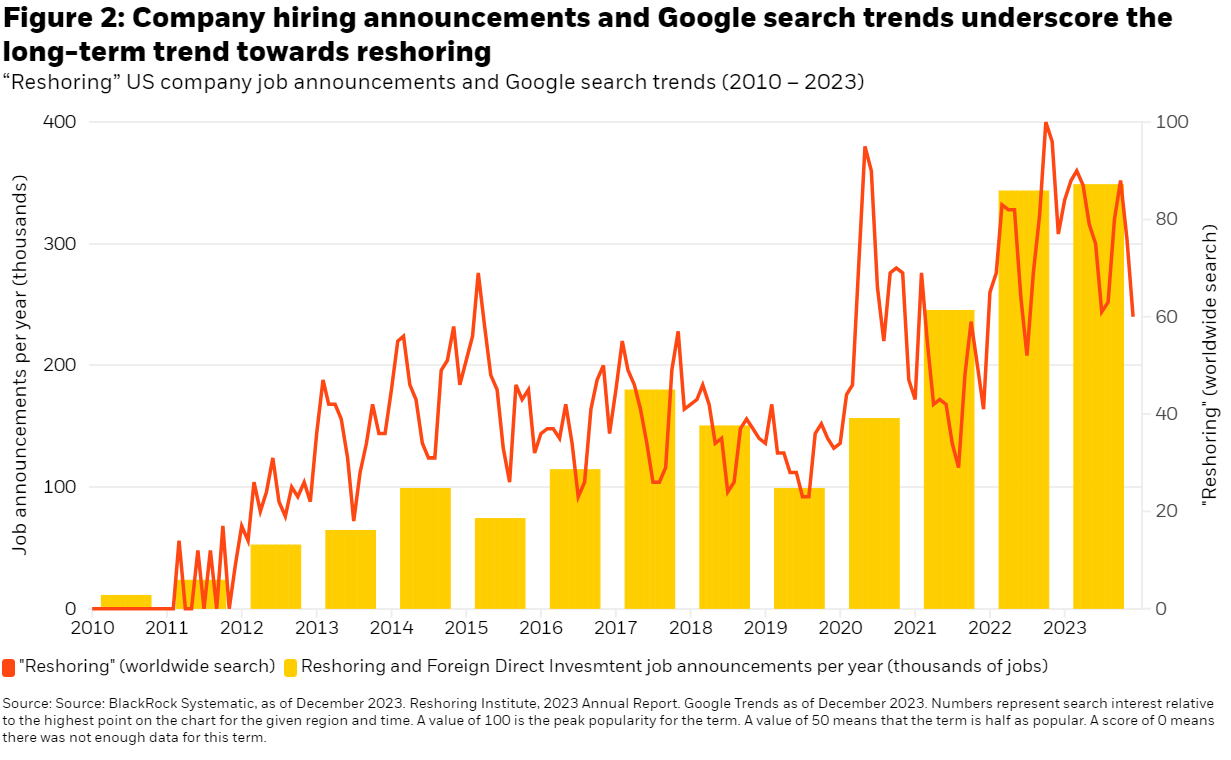

The act of reshoring, or bringing production, supply chains, and other business operations back to domestic locations, is one way that companies are adapting to a more fragmented world. Figure 2 shows the steady long-term rise in company announcements related to reshoring jobs which reached around 350,000 for 2023, along with Google search traffic revealing growing attention to the topic.

In identifying companies engaging in or benefitting from reshoring activities across industries, we employ a large language model (LLM) supplemented with granular text analysis and alternative data to help build a comprehensive basket of exposures. At a high level, this analysis reflects a positive view towards domestic industrials, raw materials suppliers, and real estate companies, and a relatively more negative view towards internationally exposed manufacturers and logistics firms.

Where innovation meets geopolitics

The technology sector has been a key area of focus around this topic given its highly global presence, with US tech companies generating nearly 60% of revenues overseas.1 This puts the tech sector at the intersection of two prominent mega forces—AI and geopolitical fragmentation—with the potential to drive a wide range of stock-specific outcomes. Recent US executive actions, such as doubling semiconductor tariffs to 50% underscores potential headwinds to firms with global exposure.2 Meanwhile, supportive legislation such as the CHIPS and Science Act of 2022 represents a nearly $53 billion investment in US semiconductor manufacturing, research, and development.3 This reflects the US government’s commitment to tech leadership which is likely to remain an area of political consensus, potentially creating a supportive backdrop for companies who are fostering US-centric technological innovation and production.

The right tail: more room for markets to price a soft landing

Soft inflationary data spurred the start of the recent rotation as investors adjusted expectations for monetary easing. As we look ahead, the potential for a right tail “FOMO” scenario could drive a more persistent rebound across segments of the market that lagged amid steady thematic and factor trends earlier in the year.

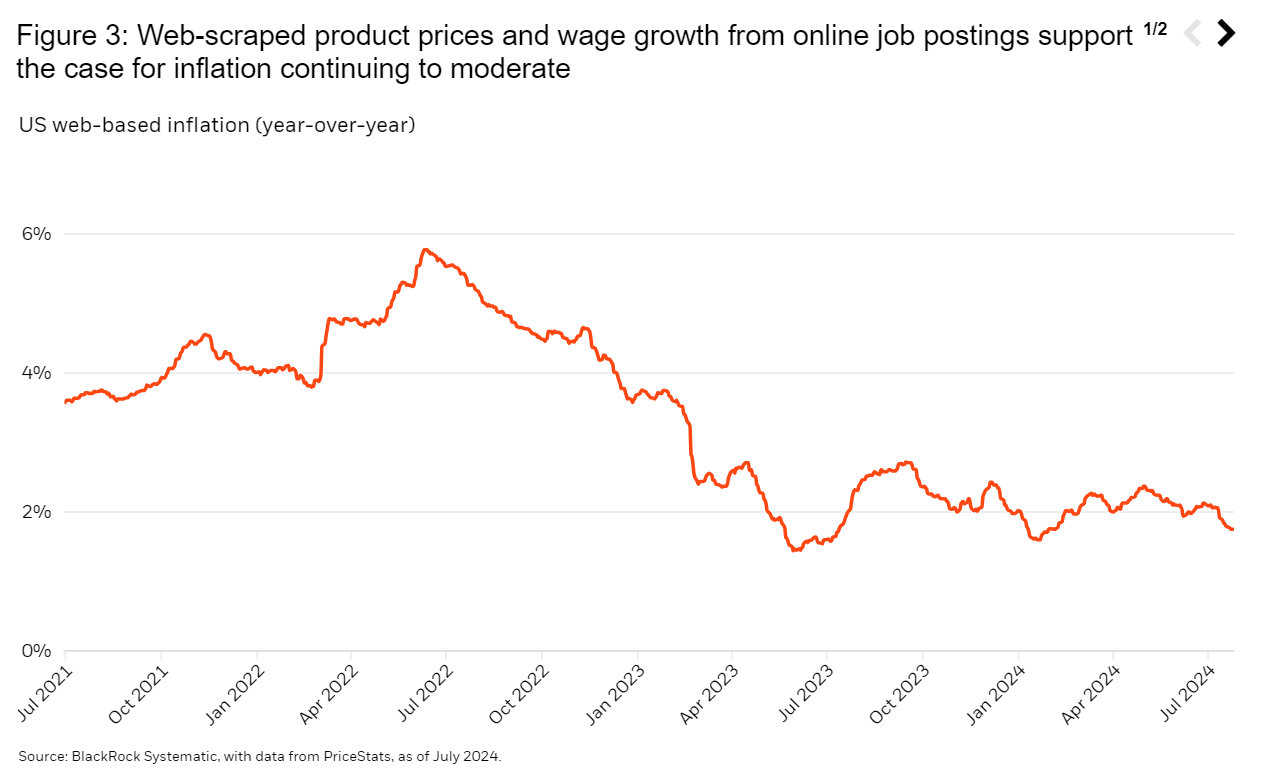

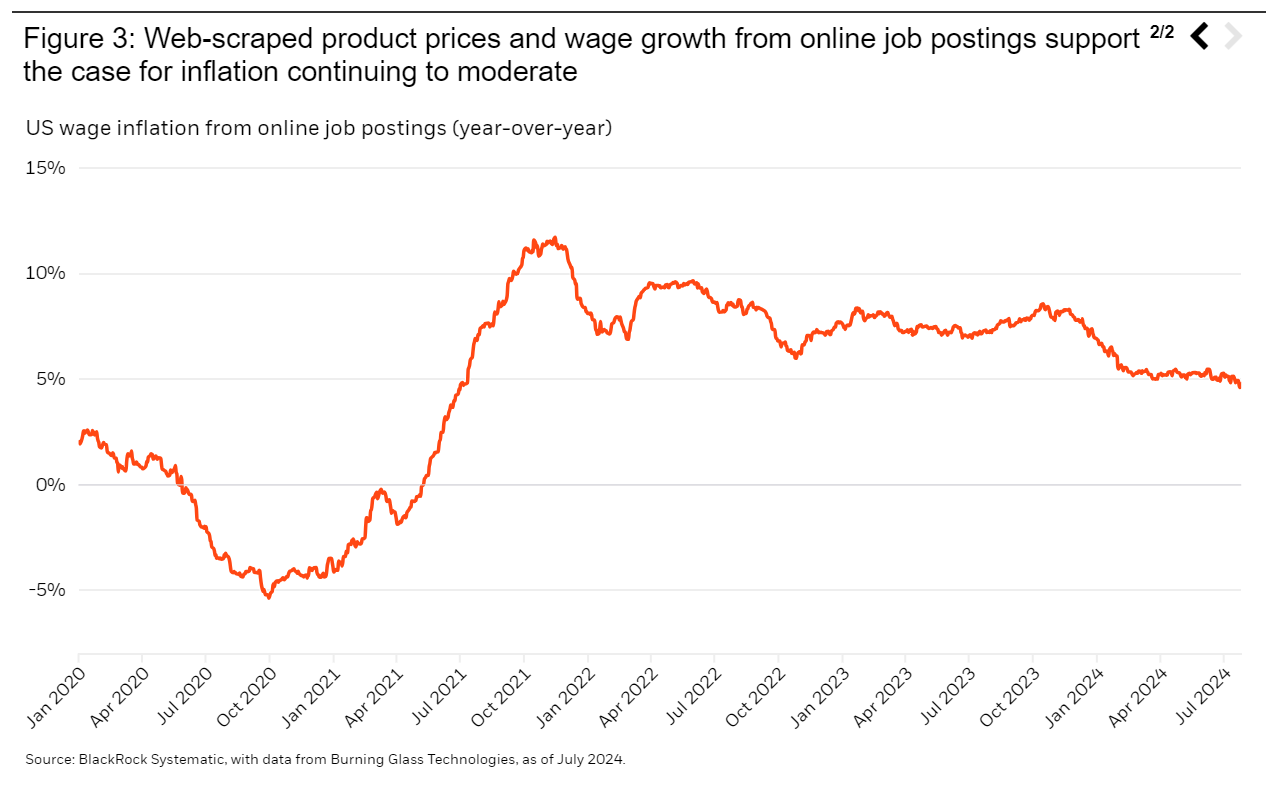

The two charts in Figure 3 show our alternative inflation indicators including web-scraped product prices and wage growth from online job postings which increasingly suggest that inflation is easing in real-time. Taken together with our estimated recession probability which remains below consensus estimates, hopes for a soft-landing have the potential to gain further traction in markets as these timely measures translate to official data releases.

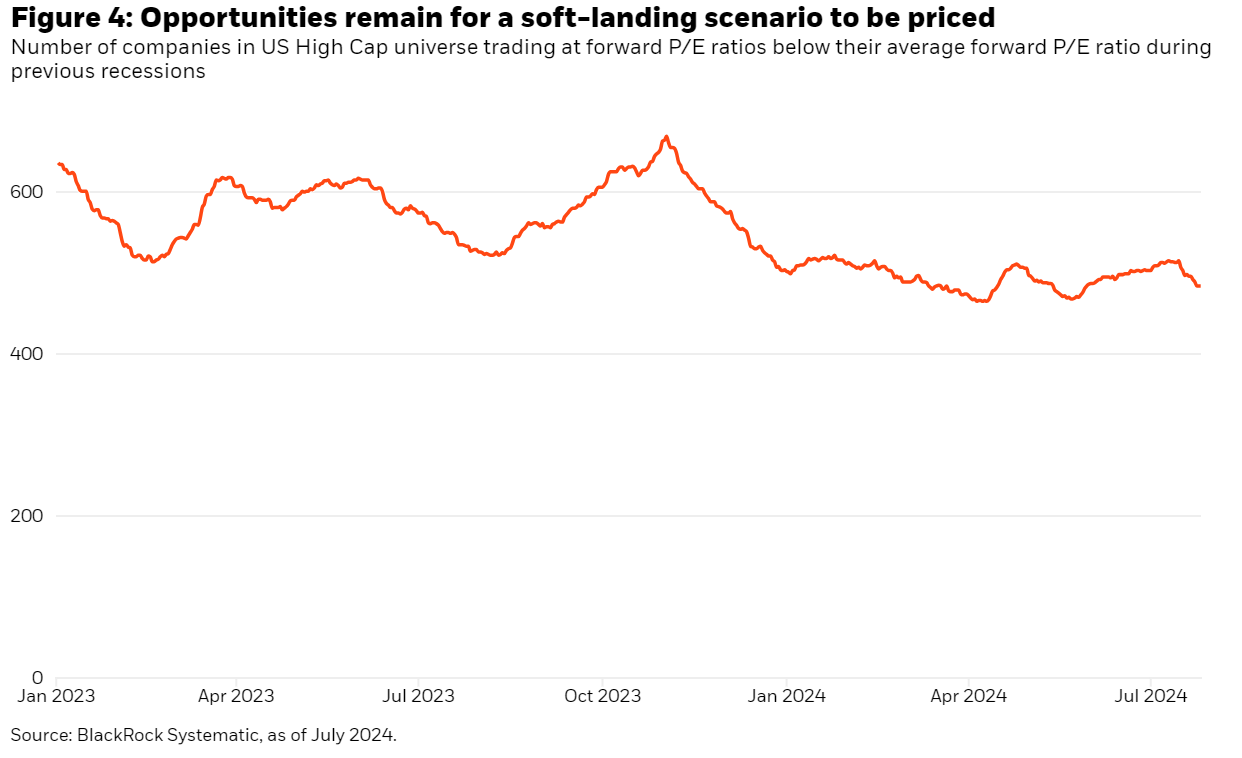

Assuming this “right tail” macro narrative continues, the question becomes how much economic optimism is already priced? We explore this in Figure 4 by measuring how many companies across the US high cap universe are trading at a forward price-to-earnings (P/E) ratio that is below their average forward P/E ratio during previous recessionary periods. The chart shows that even after the strong market run of the past few months, there are still ~480 stocks trading below levels consistent with a recession, comprising more than one-third of the total universe. Recession-consistent pricing is concentrated within the most cyclical segments of the market, including airlines, construction, and housing, creating opportunities to exploit mispricings if data continues to point towards the economy avoiding a recession.

AI sentiment slipping, but still not DotCom 2.0

As the risks of both left and right tail outcomes increase, investors may choose to reallocate capital concentrated in established positions that have significantly outperformed year to date, most notably the AI trade.

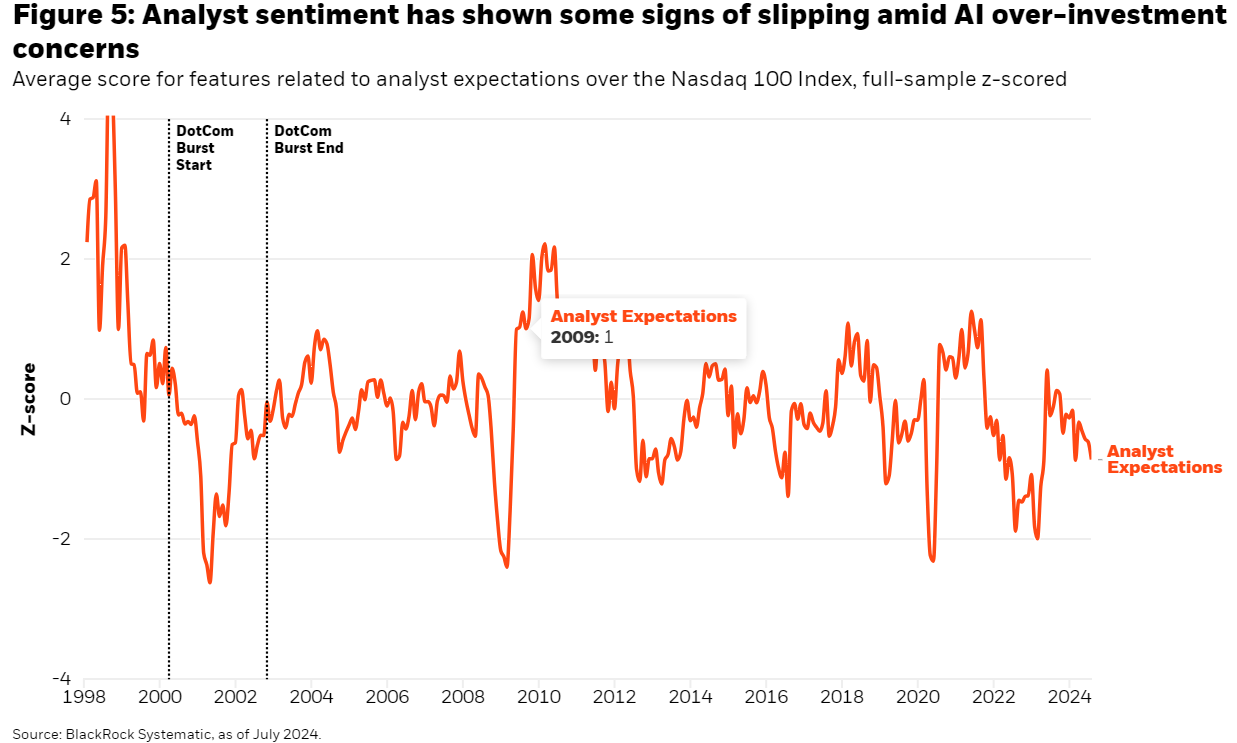

Investor sentiment towards the AI theme has waned recently in response to high growth in capital expenditure spending, particularly among the hyperscalers in this space, amid concerns that the returns on this investment may not be as high as initially expected. Analysts are increasingly questioning whether sales and earnings will be able to keep pace with these large investments over the coming years. This weakening sentiment is reflected in measures of analyst expectations shown in Figure 5 below.

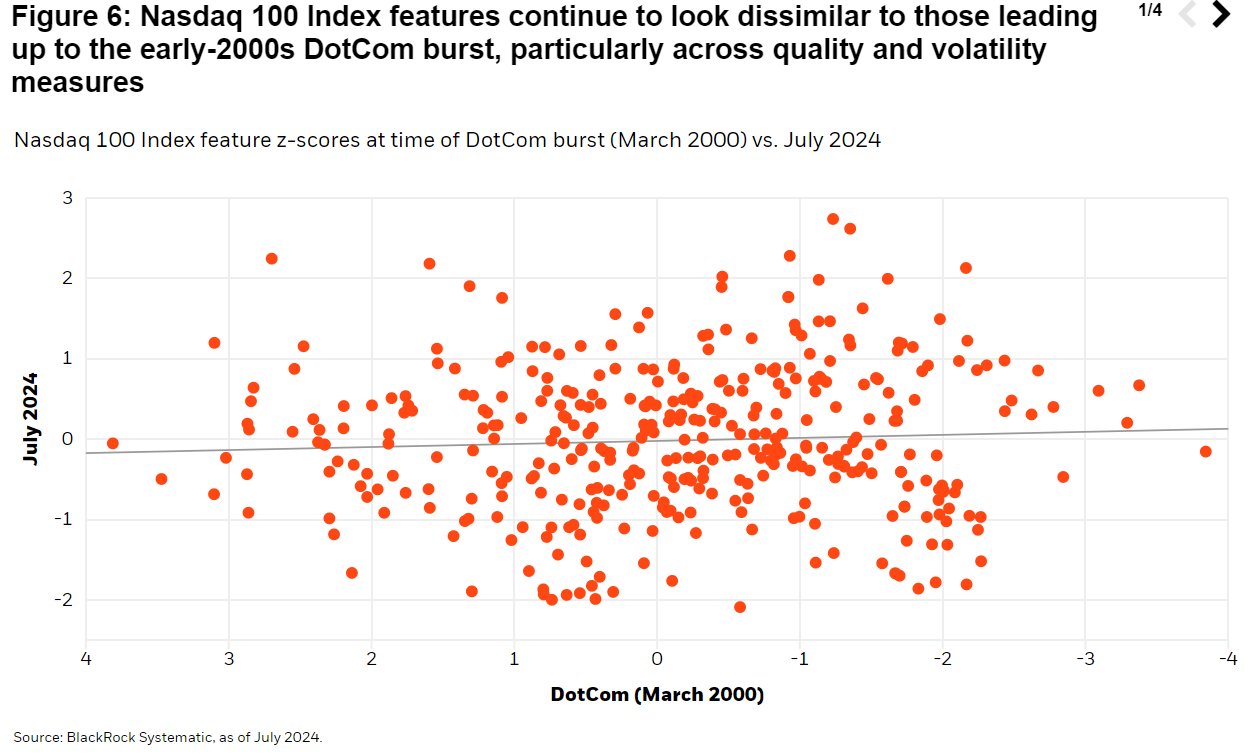

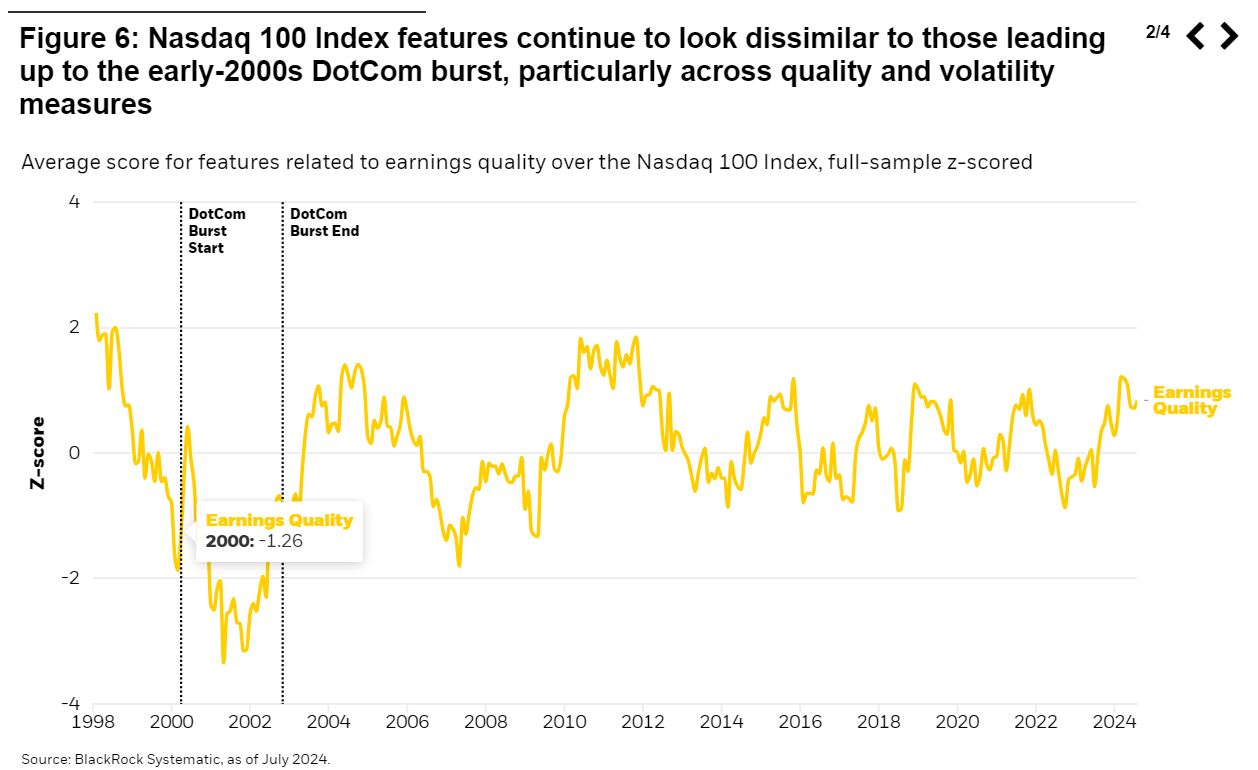

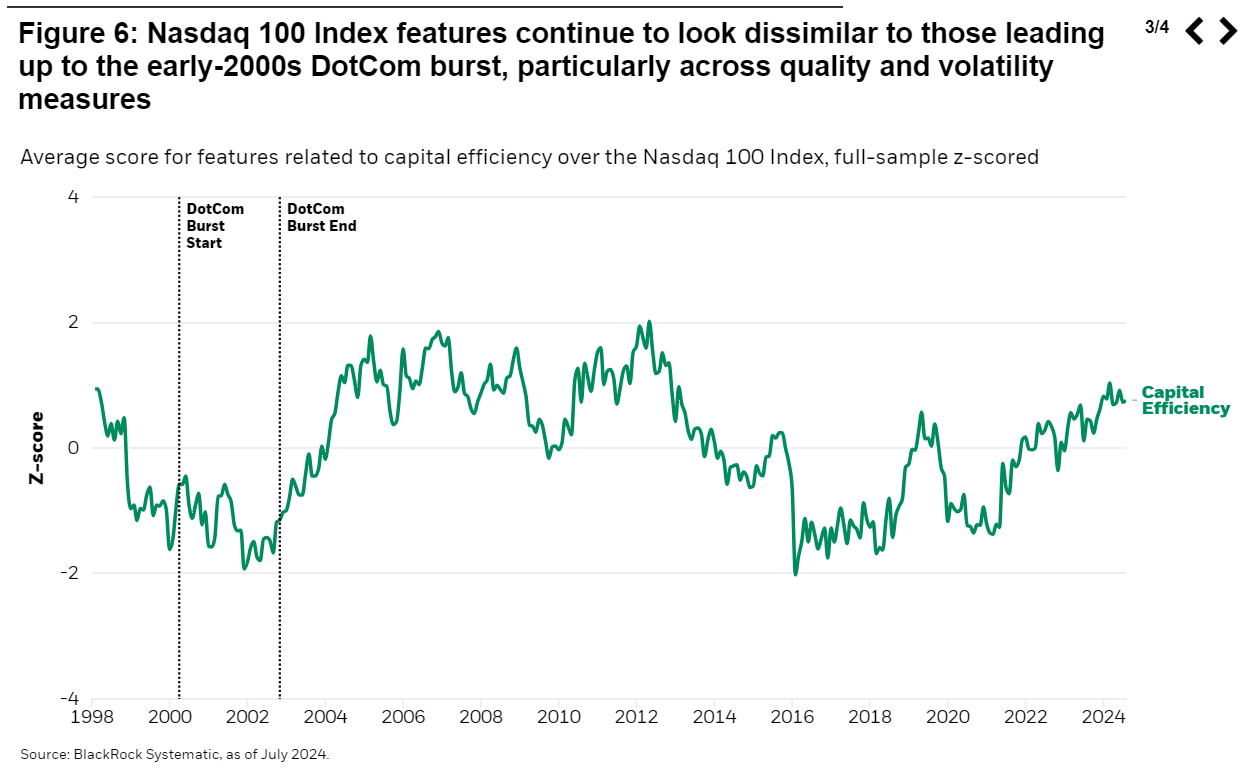

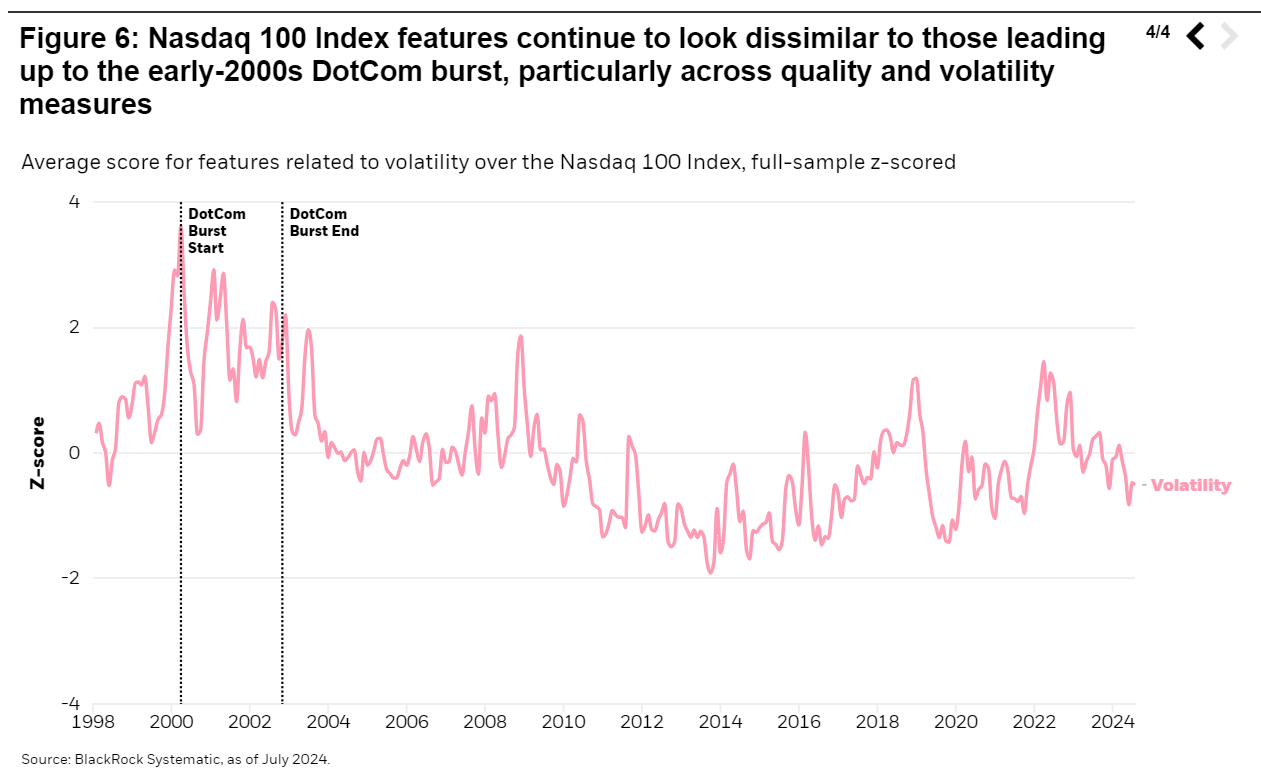

But more broadly, the current environment continues to look significantly different from the early-2000s tech bubble as illustrated in the series of charts in Figure 6. The first chart shows the z-scores of ~500 features for the Nasdaq 100 Index today versus at the start of the DotCom bubble burst—revealing very little similarity between the two periods, particularly along the dimensions of quality and volatility. The subsequent charts illustrate these differences with the time series of average aggregated feature scores across earnings quality, capital efficiency, and volatility buckets.

These dynamics have helped keep our confidence in the AI opportunity intact. However, the slight detachment in sentiment underscores the need for investment insights capable of looking beyond first-order effects.

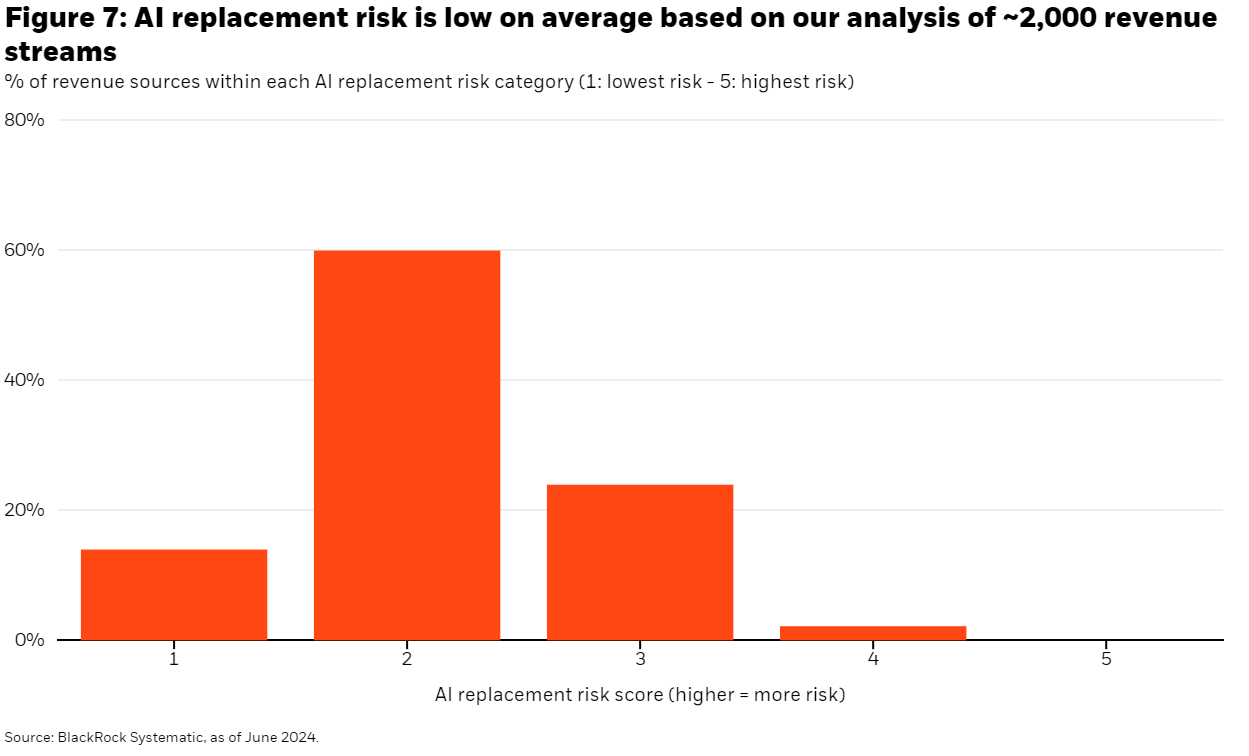

For example, we’ve taken a deeper look at the long-run risks of business models being replaced by AI technologies. There is some nuance to this as companies facing redundancy risks could also be reaping the benefits of these technologies near-term. In this way, initial market excitement in response to AI-driven efficiencies and cost savings could eventually turn to skepticism over time. This is becoming more relevant as the eagerness to reward companies based on broad associations with the theme appears to be fading.

To explore potential redundancies, we analyzed ~2,000 unique revenue sources across the economy, using a large language model (LLM) to score their exposure to replacement risks (1: lowest risk of being replaced by AI – 5: highest risk). The histogram in Figure 7 shows the economy-wide distribution of scores, revealing that replacement risks are relatively low overall.

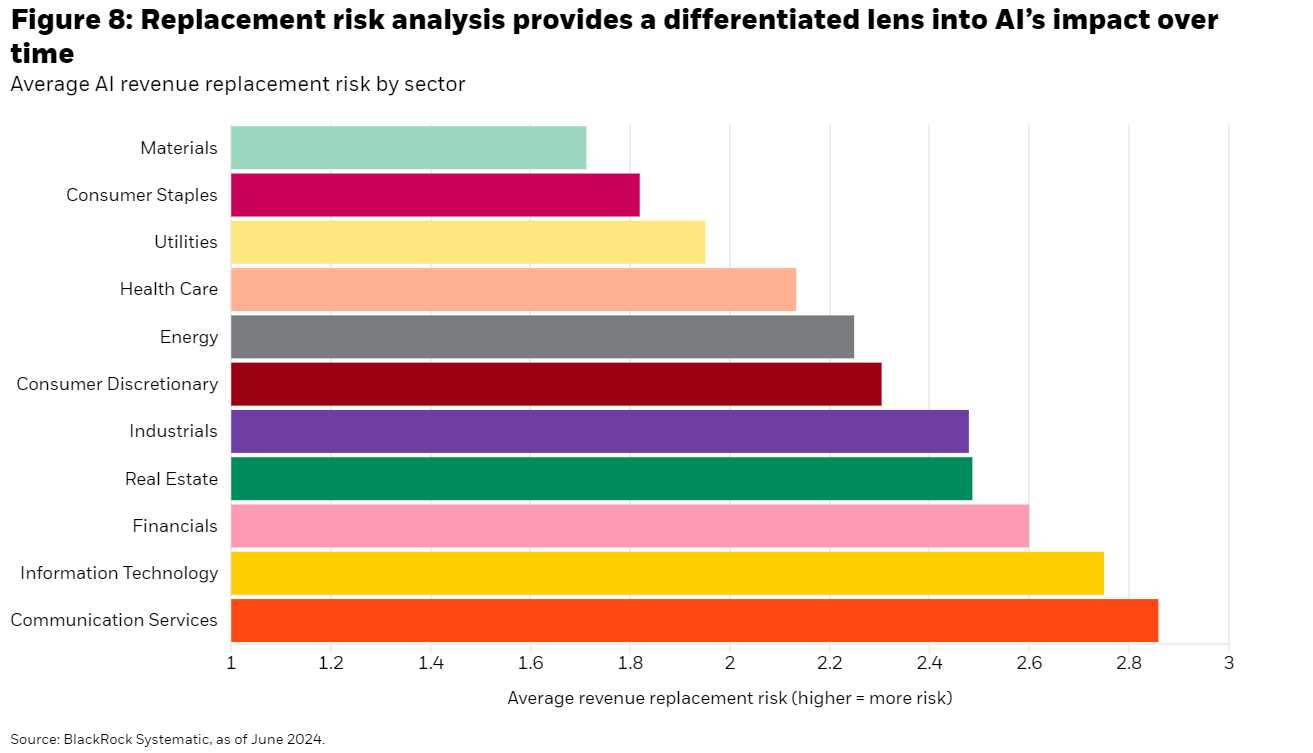

Figure 8 applies this analysis at the sector level. Materials and consumer staples appear the least vulnerable despite often being perceived as relative losers of the AI era given limited potential to benefit from these technologies. They are viewed positively in this context because demand for products is unlikely to be impacted by the progression of AI. In contrast, segments of information technology including software reflect a higher level of risk given AI’s potential to replicate certain tasks. While this is just one of several lenses we apply to the AI theme, it offers a unique perspective as investors focus on companies positioned to deliver tangible long-term results.

Conclusion

The first half of 2024 was characterized by strong equity market returns, muted volatility, and persistent market themes. Now, equity investors are faced with a range of new risks across geopolitics, macroeconomic developments, and weakening AI sentiment.

While we remain net long the AI theme, we have reallocated somewhat in favor of higher duration, more cyclical macro expressions, supported by our dovish duration and inflation outlooks and compelling signs that the equity market has yet to fully price these encouraging developments.

In navigating these evolving dynamics, our diversity of research competencies and breadth of alternative data sources helps us remain nimble and harness new opportunities amid greater uncertainty.

1 Source: BlackRock as of 4/30/2024.

2 Tariff Announcements 2024.

3 White House CHIPS and Science Act Press Release One Year After 2023.

This material is prepared by BlackRock and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2024 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is intended for information purposes only and does not constitute investment advice or an offer or solicitation to purchase or sell in any securities, BlackRock funds or any investment strategy nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction.

Stock and bond values fluctuate in price so the value of your investment can go down depending upon market conditions. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments.

Index performance is shown for illustrative purposes only. Indexes are unmanaged and one cannot invest directly in an index.

Investing involves risk, including possible loss of principal.

Prepared by BlackRock Investments, LLC, member FINRA.

©2024 BlackRock. Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates.. All other trademarks are the property of their respective owners.

USRRMH0824U/S-3753053

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All