Where Strategists See Market Opportunities in Second Half

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMarkets face several challenges in the second half as recession fears reignite and the U.S. presidential election looms in November. A recent mid-year strategist pulse check from Natixis Investment Managers revealed where strategists believe the top opportunities exist across markets.

Natixis discussed the results of their mid-year strategist pulse check in the 2024 Strategist Outlook: July Surprise. The survey included 30 market strategists across the Natixis family. The survey covered macro risks as well as market opportunities for the remainder of the year.

See also: “Strategists Believe Politics Top Macro Risk in Second Half”

Strategists Weigh In: Growth Prospects and Equities

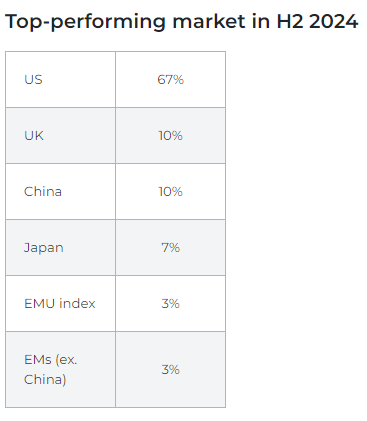

Despite concerns surrounding political risk, strategists overwhelmingly believe the greatest growth opportunities lie in the U.S. in the second half. With Europe still recovering from its recession last year, nine out of 10 strategists failed to see the region catching up to U.S. GDP growth by year’s end.

Strategists also took a dim view of China’s growth prospects, given recent moderation. While the country still posts GDP growth of over 4.5% as of Q2, it continues to trend downwards. China’s current growth pales in comparison to previous years of 8% GDP and higher, according to World Bank Group.

Uncertainty remains a core tenant of second-half outlooks. The authors noted that of Natixis strategists, “two-thirds believe corporate earnings will provide a tailwind for markets in the second half of the year. “ On the other hand, the same number worry that markets are too optimistic.

U.S. stocks offer the most second-half outperformance potential, according to those surveyed. 60% of respondents believe information technology will remain the best-performing sector. Only 13% put their bets on consumer staples, while 10% favored healthcare.

That said, much of the technology sector’s outperformance this year rode on generative AI optimism. Concerns of a potential AI bubble began to surface in recent months. “While only 7% see it as a high risk in H2, 47% rate the risk as a medium,” Natixis explained of strategist expectations. “Another 43% think it will be a low risk through year-end.”

Image source: Natixis Investment Managers

Fixed Income

Bond yields hit decade highs this year on elevated rates and uncertainty. Hopes of interest rate cuts this fall, alongside rising recession concerns, caused yields to drop recently (prices and yields move opposite within bonds). July brought with it a deluge of inflows of fixed income in July. A record $39 billion of approximate inflows went into bond ETFs last month, according to Bloomberg.

Strategists all indicated quality as their top choice within fixed income in the second half. However, they were evenly split regarding sector in the U.S. 23% of strategists viewed core short government bonds, core long government bonds, or investment grade corporates as the best opportunity. Half of all strategists also believe investors should begin extending duration exposures now.

“Fewer see the risk-reward trade-off working in favor of bonds with more exposure to credit risk,” the authors noted. Of those surveyed, “only 13% think high yield bonds or hard currency emerging market debt offer the best returns.”

In European markets, investment-grade corporates are viewed as most favorable (27%) in the second half. This was followed by 17% for core long government bonds and 13% for core short government bonds. Only one-fifth view opportunity in hard currency, emerging market debt.

Strategists on Cash and Alternatives

Many investors currently hold high levels of cash and cash alternatives in their portfolios. However, these cash holdings represent missed opportunities and higher risk in the second half.

Over half (53%) of strategists indicated the missed return potential of investing in equities versus cash in the first half. The S&P 500 generated a return of 15.3%, the Nasdaq an 18.6% return, the FTSE All-World Index 13.3%, and the Nikkei 18.28% return in the first half.

“Another 43% point to the risk of reinvesting at a lower rate when current holdings mature,” cautioned Natixis. “And the same number point out that inflation can reduce the real return investors get from cash.”

While cash diminishes as a favored investment in the second half, alternatives continue to rise. 60% of strategists believe a 60/20/20 portfolio — comprised of equities, bonds, and alternatives, respectively — will outperform a traditional 60/40 portfolio.

Risk mitigation alternatives proved most favorable amongst those surveyed. “The largest number predicts that precious metals and absolute return strategies (17% in the US, 20% in Europe for both) will outperform,” Natixis noted. It’s a bet on both downside protection as well as a potential hedge for the role of politics in the second half.

Strategists also viewed private debt and private equity favorably in the U.S. (both 13%). In Europe, private debt proved favorable with 13%, while private equity appealed to just 10%.

Options-based strategies also continue to carry weight with strategists. “In the US, strategists also see the potential for options-based strategies to deliver the best returns, suggesting some may anticipate an uptick in volatility as second-half-risk concerns play out,” explained Natixis.

Meanwhile, real estate remains a low (40%) to medium-risk (47%) option despite housing sector woes and China’s property developer influences on the global sector.

Sustainability Demand Increasingly Driven by Investors

Over half of strategists surveyed believe investors will drive demand for sustainable funds in the next two to five years. However, all believe that politics will continue to play a divisive role in the space.

“With sustainable investing at the center of heated political debate, 57% believe regulations related to these investments will get stronger,” Natixis revealed. “What those new regulations are and how they’re implemented depends on where you are.”

The largest area of opportunity comes in the form of data reporting, with 67% predicting merging within ESG scoring providers within five years. Strategists are also evenly divided between engagement (43%) and the rise of ESG leaders (43%) as the drivers of change.

“In the coming years, 60% say they expect impact investing will continue to expand,” explained Natixis. That said, “few (20%) see that sustainable investing will be adopted as a standard integrated into all portfolio strategies.”

For more news, information, and analysis, visit the Portfolio Construction Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All