As the late George HW Bush once said, “What is it about August?”

The markets are off to a rocky start to begin the month. After finishing the month of July with a +1.57% day, the S&P 500 fell -1.37% on Thursday and -1.8% on Friday, before opening down -4% on Monday. This is certainly not the start investors would have hoped.

Reasons for the Decline

There have been a few different proposed “reasons” behind the decline in the first few days of August. Perhaps it is nerves from the upcoming election. We will know the US Presidential candidates and their running mates in the coming few days. This selloff could be a reaction to both the polls and speculative policies. Some may also attribute the selloff to the Federal Reserve being too slow to lower rates. Last week’s economic data showed that payrolls increased lower than expected, and the unemployment rate hit a 3-year high.

The selloff to open Monday’s trading has been widely credited to global concerns. As a reaction to poor job reports in the US, the Nikkei index (Japan) tumbled over the weekend, declining by -12%. Part of this decline could be due to an unwinding “carry trade.” One popular investment strategy in the last few years has been borrowing foreign currency, such as the yen, for cheap and investing elsewhere at a presumably higher yield. In the last week, however, the yen has surged in value relative to the US dollar, causing investors to devest from Japanese assets and signal a “risk off” environment.

The Truth Behind the Reasons

It’s tough to make rational sense of an irrational market. When it comes to markets, the fundamental reasons behind a fluctuation don’t really matter. What matters is supply and demand. One thing we know for sure is that this market selloff has been driven by technology-related stocks. There’s an old saying about the markets that says, “all parabolic advances end the same way.” We know that for the last two years technology-related securities have been the beneficiaries of high demand. Stocks, like the ones in the Magnificent Seven, have seen their prices rise to new highs, at an unsustainable rate. Investors become excited, thinking that their investment will begin to double and keep rising. As these stocks rise relative to their peers, they make up a greater percentage of a capitalization weighted index such as the S&P 500. Now, as investors become anxious and flee these securities, these stocks are leading the market’s volatility and have caused the market to drop fast. All parabolic advances end the same way- with a sharp drop.

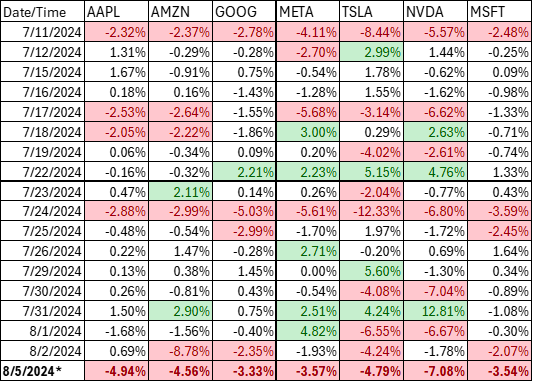

Many of these Magnificent Seven stocks are now entering “Bear Market” territory. Bear markets are signaled by a series of irrational fluctuations and sustained high volatility. The table below shows the daily fluctuations of the Magnificent Seven stocks since July 10th (the recent peak of the Nasdaq 100 Index). The green highlighted fluctuations are trading days beyond +2%, while the red highlighted fluctuations are days below -2%. Across these seven stocks, 45% of the trading sessions since July 10th have been beyond +/-2%. Even volatile “up” days are not necessarily a good thing. You can see that last Wednesday, Nvidia rose +12%. The move probably confused many investors, who were hoping to experience continued gains, when that gain was wiped away in about three days.

*Percentages on 8/5/2024 were captured during early trading. The actual closing percentage may vary. Source: Canterbury Investment Management using daily price data from Yahoo Finance.

The Market Was Due for an Outlier Day, and Technology Stocks Put it into Motion

If you were just looking at the market, and not its components, you might think that it was only a matter of time before markets experienced some short-term volatility. At Canterbury, we monitor for “outlier days.” An outlier day is any trading day that exceeds +/-1.50%. During a normal, bull market year, outlier days happen infrequently, typically between 10-20 times per year. During bear markets, they can happen almost daily, in either direction.

Prior to late July, markets had not seen an “outlier day,” or trading day beyond +/-1.50% since April. When markets go extended periods with an outlier, volatility gets extremely low and “compressed” like a spring. Eventually, an outlier day or two will serve to release some pent-up energy. More often than not, market fluctuations return to normal following a few outliers.

The alarming part right now is that the outlier days are being driven by an already emotional and bearish technology sector. Technology stocks are experiencing much larger outlier days and causing emotional market swings. If these large securities do not stabilize and find footing, it could lead the entire market to experience more outliers than would be expected.

The Equal Weight S&P 500

We know technology is volatile, but it is important to keep an eye on the equal weight S&P 500. Unlike the S&P 500, which is capitalization weighted and has a very skewed allocation to technology stocks, the equal weight index evenly distributes its allocation across all 500+ components. The equal weight S&P 500 just set a new all-time high less than a week ago. Now, it is down about -5% from that high. While this is considered a normal pullback and the volatility of that index remains relatively low, we continue to monitor for rising volatility in that index.

Money has flowed into Other Equity Areas

The recent selloff in technology-related stocks has driven up the demand for more defensive oriented securities. During Friday’s volatile move, the Real Estate, Utilities, and Consumer Staples sectors all set new highs for the year. Keep in mind that while these sectors are traditionally viewed as “defensive,” they tend to also decline during market downturns. As of right now, these sectors are generally rising, which is a positive.

As a matter of fact, last Tuesday, Proctor and Gamble (Consumer Staples stock) saw a -5% decline following an earnings report. By Friday, the stock had set a new all time high, while the market was selling off. Coca-Cola (Consumer Staples) stock also set a new high Friday, as did Southern Company (the second largest Utility stock). Even T-Mobile, which is in the Communication Technology sector, set a new high.

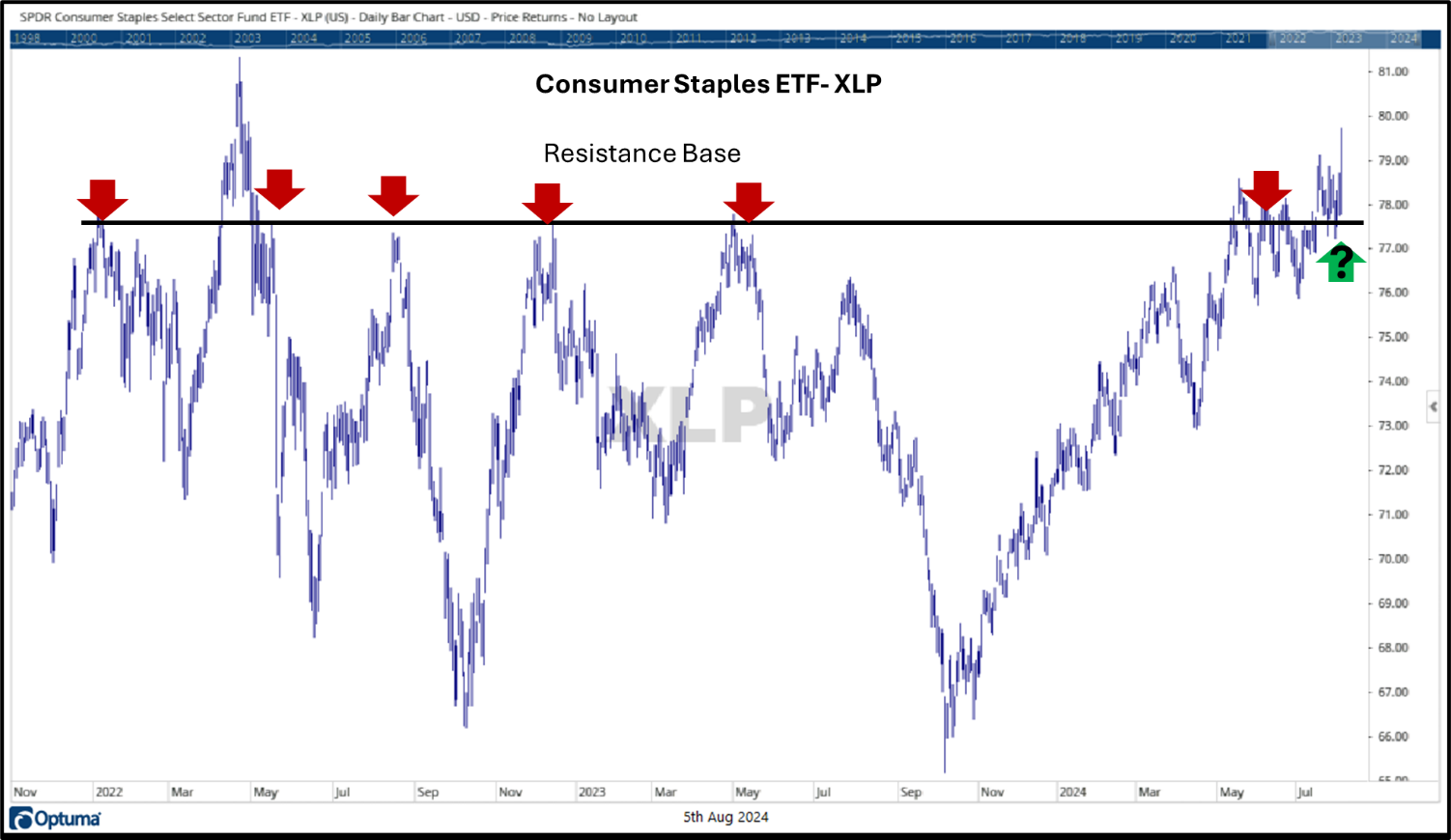

The chart below shows XLP, the Consumer Staples sector ETF, which includes Proctor and Gamble, Coca-Cola, Walmart, and Costco. You can see that the sector ETF appears to be breaking out of a multi-year base of resistance. If sustained, this would be a positive for the sector.

Source: Canterbury Investment Management. Chart created using Optuma Technical Analysis Software.

Bottom Line

When dealing with markets, one of the best pieces of advice is “do not try and make rational sense of something that is irrational.” For the last week, the markets have been irrational. While markets took a punch to the face in the trading session on Monday, given the volatility that began early last week, there’s an argument that the market could have opened up +4% as opposed to down. If the market continues to be volatile, you can pretty much flip a coin as to which direction the market will fluctuate on a given day.

It remains to be seen whether or not recent market movements are evident of an impending bear market, a release of pent-up volatility, or a short-term rebalancing of market sectors and shift in leadership. There is not enough evidence yet that says where the markets will head. There is, however, evidence that suggests many technology-related stocks are in a bear market. The large fluctuations seen in the Magnificent Seven stocks, whether those daily fluctuations have been up or down, is not a positive. Even seeing a large upward move in these securities would not signal a bull market for technology.

From a portfolio management perspective, markets have shown us that now is a time to make some adjustments to maintain stable and consistent portfolio volatility. Our Adaptive Portfolio Strategy, the Canterbury Portfolio Thermostat, happened to own positions in Consumer Staples stocks, like Proctor and Gamble and Coke, as well as a Utility stock like Southern Company. If volatility continues to rise, we will employ the use of more defensive securities, like inverse ETFs, which can help stabilize portfolio fluctuations. We will continue to monitor market fluctuations and adapt the portfolio to whichever environment comes next- bull or bear.

If you would like to learn more about Adaptive Portfolio Management and the Canterbury Portfolio Thermostat, visit www.CanterburyGroup.com, or give our office a call at 317-732-2075.

For more news, information, and analysis, visit the ETF Strategist Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by Canterbury Investment Management