Key takeaways:

- Valuations that had priced in the softest of economic landings have been tested hard over the past few days, following weak US employment data, with some of the hottest parts of the global equity market hit hardest.

- While the current volatility might be painful, a reset after a period of excessive optimism could pave the way for a healthier market for the remainder of 2024.

- We believe this could be a favourable environment for stock pickers, with high levels of market volatility, creating opportunities to identify and invest in fundamentally strong companies that appear to have good prospects.

What happened?

After a highly volatile moment in global markets, it is important to take stock of what has been happening. It now seems very clear that markets got ahead of themselves. Sentiment indicators, valuations and surveys all showed significant complacency about the outlook for the global economy. Many different types of investors had become very bullish on the back of good earnings results and the expectation for interest rate cuts, creating a fragility to the market rally.

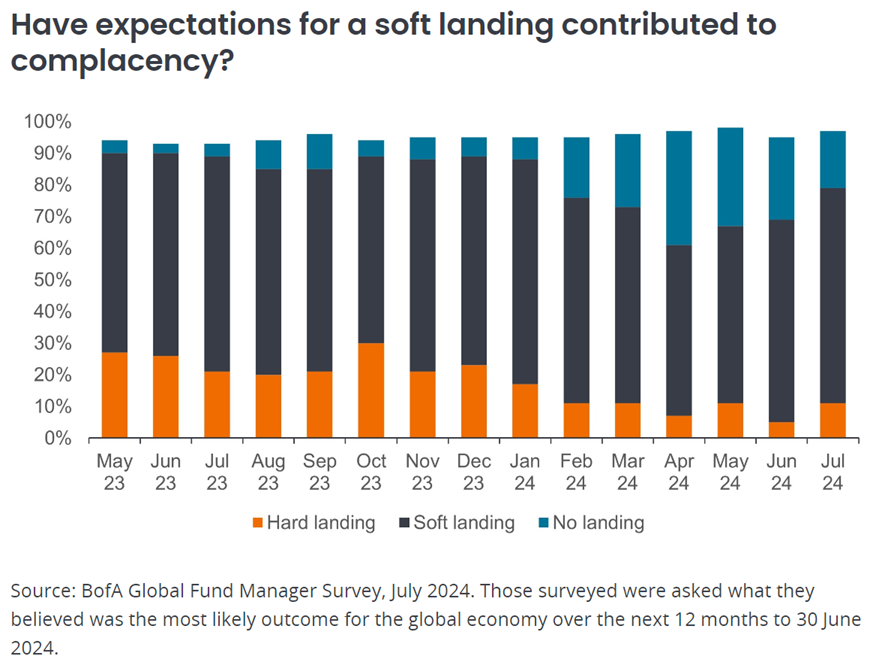

Valuations had priced in the softest of economic landings, in line with expectations (see chart), and a weak labour market report was the catalyst for many to come to the realisation that there is still a reasonable chance of recession. That said, it still seems too early to make a decisive call, with a lack of glaring financial weaknesses creating resilience in the US economy and a stronger Institute for Supply Management services release showing that it is not all doom and gloom. The magnitude of market moves is perhaps as much about the lower liquidity we see at this time of year as the scale of any reset in sentiment or economic outlook.

The equity rotation persists

It is notable that the worst volatility has been in the hottest parts of the global equity market, such as the so-called Magnificent 7, the NASDAQ 100 and certain Asia stock markets (eg, TOPIX). However, it is also important to note the areas that have held up better over the last couple of days and the last month, namely US value shares, US midcap stocks and the FTSE 100 Index in the UK. This suggests that there is an ongoing market rotation against the backdrop of a reset from over-enthusiasm. Lower interest rates, in the absence of a hard landing, have historically been good for risk assets overall, but some had already perhaps more than priced this in. A reset could create a more solid foundation for a push higher over the rest of the year, assuming the US labour market holds together.

A focus on Japan

The most significant volatility has been seen in Japan, where the export-sensitive stock market had previously benefited from continued weakening of the yen. The rapid strengthening of the currency in recent weeks likely pushed leveraged investors to unwind their positions. With interest rates having risen so much elsewhere and having barely moved in Japan, the yen has been an obvious candidate for funding foreign exchange carry trades.

However, the rapid currency unwind seems to have bled into equity market sentiment as a strengthening yen brought into question assumptions about Japanese export earnings. For those less committed holders, such a clear short-term headwind may have overpowered the longer-term argument of improving shareholder friendliness. The market may remain volatile in the short term as investors react to unprecedented market moves – Japan’s TOPIX rallied sharply on 6 August, a day after its second-worst single-day fall since 1950.

What’s next?

The silver lining is that, while the current volatility might be painful, a reset after a period of excessive optimism could lead to a healthier market. However, even if widely expected, a market reset of this speed and magnitude is unnerving for most any investor. It’s important to understand that a soft landing is being questioned but is not out of the question, meaning economic resilience and declining interest rates could ultimately help to lift risk assets again.

At the same time, these events are a critical warning that the market is relatively expensive and likely will remain extremely sensitive to any more negative economic news for the time being. Further, U.S. household stock ownership is at an all-time high, so stock market performance is likely to affect consumer confidence more than ever before.1

While we continue to closely monitor the economic data, we see this as a favourable environment for active managers to benefit our asset allocations – the relative resilience of some areas of global markets shows that there are opportunities for those willing to look for them.

###

Sources and Definitions

1 “More Americans Than Ever Own Stocks.” Wall Street Journal, 18 December 2023.

Active management: An investment management approach where a fund manager actively aims to outperform or beat a specific index or benchmark through research, analysis and the investment choices they make.

Bull market/bullish: A bull market is one in which the prices of securities are rising, especially over a long time. Bullish sentiment is where investors are optimistic about the prospects for share price gains.

Foreign exchange carry trades: A strategy that involves borrowing from a lower interest rate currency to fund the purchase of a currency that offers a higher interest rate, with the intention of capturing the difference as a profit.

FTSE 100 Index: A stock market index that represents the 100 largest companies listed on the London Stock Exchange.

ISM Services report: A report produced by the Institute of Supply Management, a body responsible for measuring the views of participants in manufacturing and non-manufacturing industries in the US.

Leveraged investors: Where investors have borrowed to increase exposure to an asset/market. This can be done by borrowing cash and using it to buy an asset, or by using financial instruments such as derivatives to simulate the effect of borrowing for further investment in assets.

Liquidity: Liquidity is a measure of how easily an asset can be bought or sold in the market. Assets that can be easily traded in the market in high volumes (without causing a major price move) are referred to as ‘liquid’.

Magnificent 7: The seven major US listed technology stocks that have seen significant stock price gains over the past few years: Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla.

Market rotation: The movement of money around the marketplace, from sector and industry, or between countries or asset classes, as investors and traders look to anticipate the next state of the economic cycle or react to specific market events.

Mid-cap stocks: Companies with a valuation (market capitalisation) within a certain scale, eg. $2-10 billion in the US, although these measures are generally an estimate.

Nasdaq 100: A stock market index consisting of the 100 largest non-financial stocks traded on the Nasdaq stock exchange.

Recession: A decline in economic activity, commonly identified as a fall in GDP (gross domestic product) for a country over two consecutive quarters.

Risk assets: There is no specific classification of ‘risk’ assets, but they are generally considered to be assets that can display a high degree of price volatility, such as commodities, equities or real estate.

TOPIX: The Tokyo Stock Price Index – a leading index of companies traded on Japan’s Tokyo Stock Exchange.

Value shares: Value investors search for companies that they believe are undervalued by the market, and therefore expect their share price to increase. One of the favoured techniques is to buy companies with low price to earnings (P/E) or price to book (P/B) ratios.

Volatility: The rate and extent at which the price of a portfolio, security or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Janus Henderson Investors

Read more commentaries by Janus Henderson Investors