The Windshield Is Bigger Than the Rearview Mirror for a Reason

"I want to tell you that the windshield is bigger than the rearview mirror for a reason. What's in front of you is so much more important than what's behind you."

- Singer & Songwriter Jelly Roll

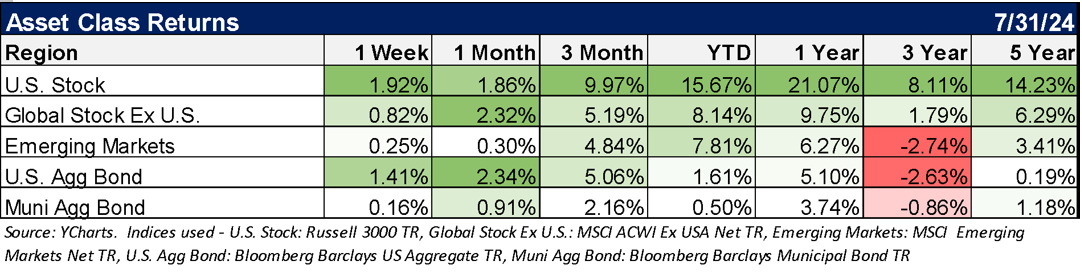

U.S. and global stocks advanced in July and strengthened year-to-date gains. Despite heightened volatility, the S&P 500 Index returned 1.2% in July to post its third straight monthly gain. July’s performance lifted the index’s year-to-date return to 16.7%. Unlike the performance driven by the “Magnificent 7” for much of the market rally, July returns were strongest from Real Estate, Financials, and Utilities. Somewhat surprisingly, small-cap stocks rallied more than 10% in July and value stocks outpaced growth stocks across size categories. Bonds also advanced amid the market’s growing rate-cut expectations.

The U.S. Federal Reserve Bank (Fed) left rates unchanged on July 31, awaiting greater confidence that core inflation is on a sustainable path toward the 2% target. Core Personal Consumption Expenditures (PCE), the Fed’s preferred gauge, remained unchanged at 2.6%. Citing continued progress on the inflation front, the Fed fueled market speculation about future rate cuts. At the end of July, the futures market placed a 90% probability on the Fed cutting rates by 25 bps in September.

It is clear that all of the central banks are not in a geosynchronous cutting cycle, but the trend is certainly that interest rates globally are poised to come down. The Bank of England (BoE) and Bank of Canada (BoC) cut rates for the first time in more than four years, while the European Central Bank (ECB) held steady, and the Bank of Japan (BoJ) was forced to raise rates to stabilize the Yen against the U.S. Dollar.