What’s going on with US consumers? This question is always top of mind for investors, and an easy one to ask. But it’s full of nuances, especially late in the credit cycle with mixed signals emerging. Lingering pandemic-related distortions have made it even harder to get a firm handle on consumer health, but getting that handle is critical to investing effectively.

Bearish Signals…but Not Broad Weakness

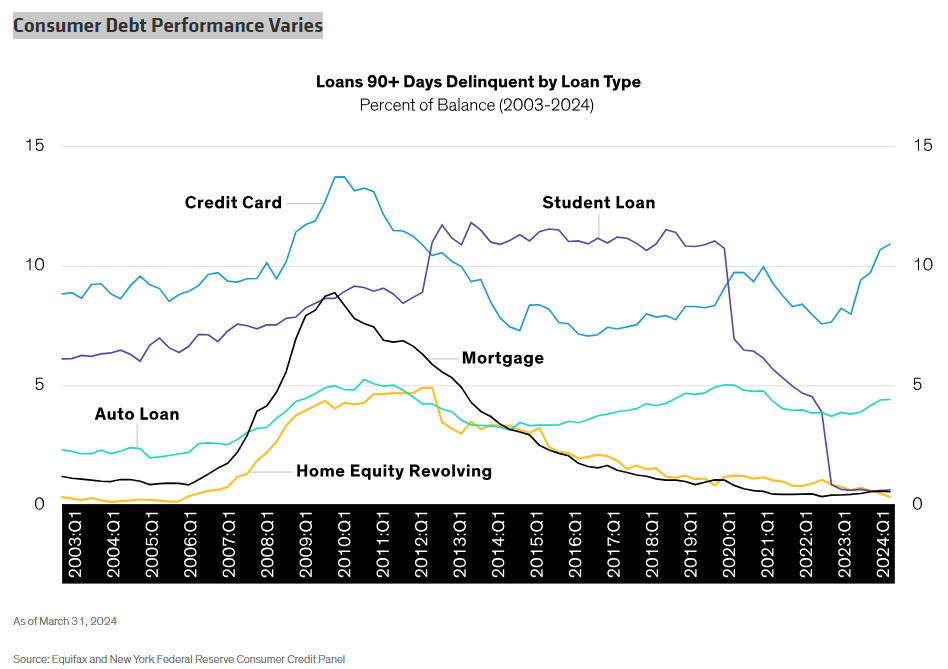

A snapshot of consumer fundamentals and macro trends today reveals a mixed picture. There are plenty of bearish signals. The labor market shows signs of weakening. Prices on many consumer staples remain high. Savings rates have declined while delinquency rates have been rising. And higher interest rates are starting to weigh on consumers with multiple forms of debt.

But while there may be conservatism in consumer behavior, we don’t see broad weakness in the fundamentals. Household debt growth is slowing and net worth is increasing, while unemployment remains low by historical standards. And the Federal Reserve is getting closer to an interest rate cut, which could alleviate borrowing costs.

What’s more, lending standards have been tightening over the last two years. Yes, delinquencies are up—but they’re rising from historic lows to what we consider more normal levels. As we see it, the coupons available on most consumer loans today better reflect the prevailing interest rate and risk environment.

A Formula Creating More Opportunity for Investors

Mixed signals can create a formula for a promising investment environment. We’ve seen varied performance across consumer asset classes this year (and even across originators within asset classes) in the massive $6.3 trillion asset-based finance market. For investors who can be discerning with their capital, this backdrop can be compelling.

Of course, while broad macro views can provide important insight into the data, investors in consumer debt must focus on specific loan opportunities, not aggregated loan data. To use an analogy borrowed from equity markets, we think the most effective approach focuses on “single names” rather than the total index.

This much is clear to us: consumers aren’t monolithic, nor is consumer-debt performance throughout a cycle. Investors should look to buy from specific loan originators that specialize in particular loan types. It might be an auto loan, a consumer loan or a credit card receivable to someone who is underserved by traditional banks. We believe the right investment approach is a targeted one.

Perhaps most importantly, we think it’s critical to invest in a specific approach to underwriting, which we consider one of the most important indicators of likely performance.

Loan Purpose Matters….

For example, data consistently shows that consumers tend to prioritize certain types of debt over others when times are tough. Auto loans are near the top of the repayment hierarchy and, despite some recent negative headlines, we consider the sector attractive (for this and other reasons).

Another important element of consumer behavior is tied to the purpose of a given loan. Think of someone who buys a car or installs energy efficient windows. The consumer associates something tangible with the debt, and that typically affects his or her likelihood to repay it.

….So Does the Loan Originator

There’s considerable variation among loan originators, too. A great deal of consumer borrowing today—particularly for higher-risk borrowers with near- or sub-prime credit ratings—is originated by non-bank lenders. The quality of underwriting on these loans varies.

This puts a premium on private credit investors’ sourcing and underwriting capabilities: in our view, how soundly a loan is underwritten is one of the most reliable indicators of performance. The targeted borrower, marketing strategy, loan structure, underwriting fundamentals and track record of the loan originator all make a big difference.

In other words, the originator of the loan matters as much as the type of debt.

Vetting the many platforms that can be loan sources is also important, in our view. What are the key pillars of the originator’s underwriting philosophy? Can the investor validate those views with supporting data? What’s the relationship between marketing, underwriting and collections? Quantitative analysis of dynamics like these can help investors decide whether they are partnering with the right originators. If an originator can’t reconcile its views on risk with its historical performance, it might be time to look for investment opportunities elsewhere.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein