As students get closer to making a final college decision, the last two years of high school are particularly important.

Parents will want to review their financial strategy to meet the costs of college, including a review of current savings, financial and merit aid, scholarships and loan options. Students face many deadlines for standardized tests and application requirements.

Having an action plan can help families focus on multiple tasks, stay on top of deadlines and decrease stress. Consider this “Four-year action plan to prepare for college,” that can be helpful for families to stay on track.

Considerations for junior year

While not quite crunch-time in the task of preparing for college, the junior year is busy. Parents will research deeper into financial aid and juniors will focus more on academic requirements. Since the application process begins during the first half of senior year, a student’s academic record during junior year is especially important.

Financial priorities for parents

- Determine the Student Aid Index (SAI) for federal financial aid (formerly known as the Expected Family Contribution or EFC). This calculation will drive aid awards, including federal grants, needs-based aid from colleges and student loans. Parents and students should visit www.studentaid.gov to access the online financial aid estimate to get a sense of what a potential aid package might look like.

- Note that the calculation on the Free Application for Student Financial Aid (FAFSA) is based on family and student income from the “prior-prior” year. This means that, for a student entering college in the fall of 2025, the financial aid calculation will be based on information from the 2023 calendar year tax return (which was generally filed in April, 2024). Note that increases in income, from selling a stock or changing your Roth IRA, for example, may hurt aid.

- Review 529 account ownership to determine if changes are appropriate when considering financial aid. There have been recent changes in how financial aid is calculated. For example, distributions from 529 plans owned by non-parents such as grandparents will no longer have negative impact on the aid calculation. Learn more about changes to the Free Application for Federal Student Aid (FAFSA) form in this article.

- Research whether targeted colleges require the College Scholarship Service Profile (CSS Profile) application as part of their financial aid process in addition to the FAFSA application. Be aware that additional information not required on the FAFSA submittal may be needed.

- Start compiling information for FAFSA submission, including tax returns and information on savings, investments, and assets for both the parents and student(s).

Action items for students

- Prepare for standardized tests (PSAT in the fall, SAT/ACT later in the year), and consider taking a test prep course or working with a tutor.

- Build a resume including interests, summer employment, internships, community service and achievements.

- Start compiling a target list of schools.

- Begin college visits, making sure to get contact information for the admissions contact assigned to your region and email each contact about your interests.

- Before the end of the school year, meet with teachers, coaches or mentors to request letters of recommendation.

- Make sure course work, such as the number of Advanced Placement (AP) classes, reflects the academic requirements of targeted schools.

- Register with the NCAA if pursuing athletics at a Division 1 or 2 college.

Considerations for senior year

Senior year in high school is a memorable one as students focus on a major milestone: graduation. For students planning for college, it’s a year with many deadlines and final preparations.

Financial priorities for parents

- Make sure you have enough liquid assets for college-related expenses. This may require investment transfers within college savings accounts to more conservative options.

- Consider allocating funds within a custodial account. An UGMA (Uniform Gifts to Minors Act) or UTMA (Uniform Transfers to Minors Act) account or a regular savings account for travel costs are not considered “qualified expenses” for 529 plans.

- Identify which savings accounts to tap into first for expenses based on investment, tax or financial aid considerations. See “Strategies to make the most of college savings.”

- Research tax credits and deductions to help with college costs. See the IRS page, “Tax benefits for education.”

- Attend a college aid workshop or meet with a professional college counselor.

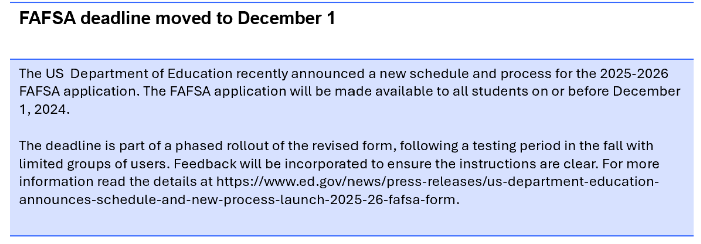

- Complete the FAFSA form (between December 1 and June 30 for this year’s filing). Note that many states and colleges request FAFSA submission as soon as possible after the application period opens. The earlier you can submit the FAFSA the better since it may improve prospects for receiving aid.

- Have the student complete a health care proxy when turning 18 and before going to college.

Action items for students

- Over the summer, start working on the Common Application and college essay.

- Consider taking the SAT in the fall, depending on your previous results and the range of scores required for the schools you are targeting.

- Review social media accounts before applying to make sure posted content would not jeopardize an admissions decision.

- Establish a professional presence by creating a LinkedIn profile.

- Complete applications as soon as possible. Be aware of early decision/early action and regular decision dates. Make sure the high school has the final list to send transcripts.

- Research and apply for local scholarships.

- Schedule official campus visits when school is in session to get a better sense of the typical student environment.

- If pursuing athletics, contact coaches to schedule official on-campus visits in the fall.

- Trim your college list to a range of options: safety, match, and reach schools.

Consult with an advisor

A financial advisor can help families navigate the entire process. From saving and financial planning and taking advantage of tax-efficient strategies, an advisor can be a critical resource. It is important to consult with a financial professional who is familiar with your individual financial situation.

Explore Franklin Templeton’s resources and learn how a Franklin Templeton 529 plan can help you invest for your child’s education.

For more information, speak with your financial professional.

WHAT ARE THE RISKS?

All investments involve risk, including possible loss of principal.

Investors should carefully consider the 529 plan’s investment goals, risks, charges and expenses before investing. To obtain the Program Description, which contains this and other information, talk to your financial professional or call Franklin Distributors, LLC, the manager and underwriter for the 529 plan at (800) DIAL BEN/342-5236 or visit franklintempleton.com. You should read the Program Description carefully before investing and consider whether your, or the beneficiary’s, home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in its qualified tuition program.

Franklin Templeton’s 529 College Savings Plan is offered and administered by the New Jersey Higher Education Student Assistance Authority (HESAA); managed and distributed by Franklin Distributors, LLC, an affiliate of Franklin Resources, Inc., which operates as Franklin Templeton.

Investments in Franklin Templeton’s 529 College Savings Plan are not insured by the FDIC or any other government agency and are not deposits or other obligations of any depository institution. Investments are not guaranteed by the State of New Jersey, Franklin Templeton, or its affiliates and are subject to risks, including loss of principal amount invested. Investing in the plan does not guarantee admission to any particular primary, secondary school or college, or sufficient funds for primary, secondary school or college.

Franklin Templeton, its affiliates, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax professional.

This material has been provided for informational purposes only and should not be construed as investment advice or a recommendation of any particular investment product, or strategy.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

© 2024 Franklin Distributors, LLC. Member FINRA/SI

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton