Equity markets have become more volatile of late, as investors fret about economic slowing ahead of likely Federal Reserve rate cuts. But beyond the obvious macro-level implications of what had been a higher-for-longer rate environment, we believe investors should consider how high rates affect corporate profits—an issue that is too often overlooked.

Higher Rates Have Increased Financing Costs

Higher interest rates have dampened aggregate demand, which has helped contain inflation, although pockets of wage inflation persist. Less noticeable to some investors is the impact of higher rates on corporate and household balance sheets. That’s because the effects of changing rates—both up and down—tend to build as time passes, particularly for infrequently purchased items with higher price points.

For example, installment loans, such as home mortgages and auto loans, are typically measured in years rather than months. Regardless of market conditions, a relatively small number of consumers purchase these big-ticket items in any given month. As a result, it may take a long time for borrowers to feel the adverse effects of higher rates.

Consider what would happen if interest rates spiked for six months but then fell sharply. Given the tight time frame, few consumers of high-cost goods would be exposed to elevated financing costs. But what happens when rates stay high for a long time? That’s the scenario we’ve been experiencing, with consumers and businesses feeling the pinch.

High Financing Costs Reduce Economic Activity and Flow Through to Bottom Line

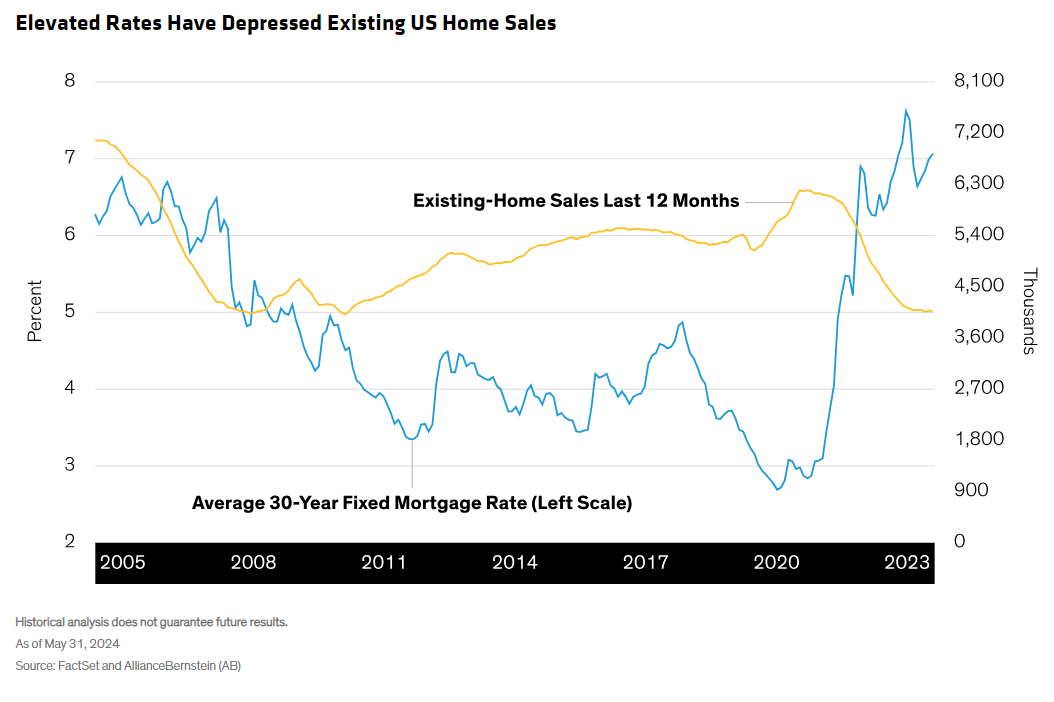

The housing market is a case study. Trailing 12-month existing-home sales hit a 14-year high of 6.2 million in August 2021, driven by rock-bottom fixed mortgage rates (Display). Since then, 30-year fixed mortgage rates have climbed more than 400 basis points to a 20-year high of roughly 7%. The result? Trailing 12-month home sales fell to four million units by the end of May 2024.

Since May 2022, over 9 million existing-home sales closed with rates above 5%. Trailing 12-month new-home sales are also down from the nearly 900,000 May 2021 peak.

The effect of higher interest rates on borrowing costs is easy to see. But less visible is the greater amount of consumer cash flows going toward debt servicing—and the inevitable crowding out of other spending that ensues.

For businesses, the effects of an elevated-rate environment are also significant. Lower demand—and lower prices—eventually erode corporate operating profits. Companies selling lower-priced items have seen declining sales volume in recent months. But companies heavily weighted toward high-end product lines still face risks, as they may not have medium- or lower-end products to offset changing consumer preferences.

A Return to Survival of the Fittest?

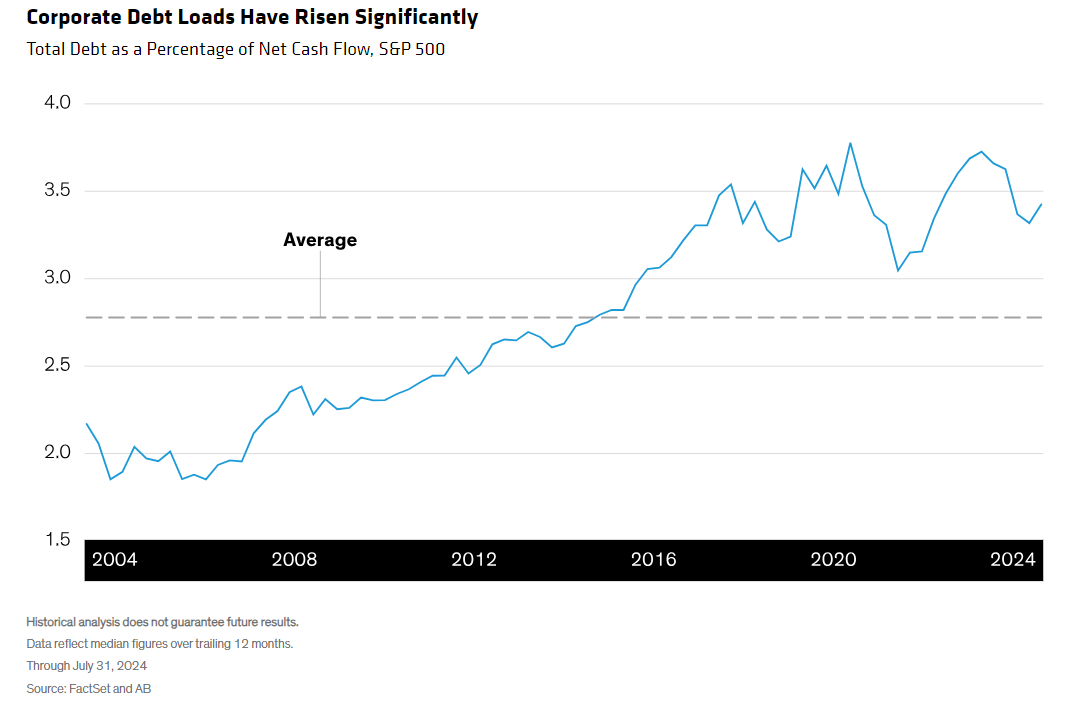

In this environment, investors must carefully consider corporate debt loads, which are significantly higher than the 20-year average (Display).

Healthy companies in rational markets typically generate excess cash after appropriate reinvestment and don’t need to rely on debt to fund operations. When demand falls, earnings may come down, but not necessarily enough to raise concerns about a company’s financial stability.

On the other hand, profitable companies with heavy debt loads may take on risks overlooked by investors—especially if those companies operate in cyclical markets. This can make them particularly vulnerable to sales and earnings weakness. Deteriorating financial results, coupled with high financial leverage, can even lead to solvency risk. For this reason, investors must make sure that a company under pressure is investing enough to support future earnings growth.

Cautionary Tales Abound

When financial conditions are tight for an extended period, the weakest players are often the most vulnerable.

A good example is Silicon Valley Bank (SVB), which failed in a matter of days in early 2023. Sometimes it takes longer. Transportation services player Yellow Roadway was burdened with debt for many years before filing for bankruptcy around the same time as SVB, when rates increased more than creditors deemed their operations could support.

SVB and Yellow both collapsed after about a year of higher rates. But we can look back to the global financial crisis for other cautionary tales, including the failures of upstart mortgage lender New Century Mortgage and investment banking giant Bear Stearns. This trail of tears didn’t end until 2009 with the forced reorganization of well-known companies such as General Motors. Consumer demand remained depressed for several years after that.

While we don’t anticipate anything that extreme happening this time around, today’s high-rate environment still has the potential to create significant strain on consumers and businesses. Even companies with strong free cash flow to support high debt loads can be adversely affected. Higher interest expenses and the need to pay off debt as it matures can threaten a company’s operations, competitive positioning and profitability. Ultimately, this can affect how investors value its stock.

Investment strategies that don’t sufficiently consider the potential damage of heavy debt and volatile cash flows are risky propositions. Identifying companies with quality businesses, manageable debt levels and healthy balance sheets can reduce risk and ultimately boost long-term return potential.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

References to specific securities discussed are not to be considered recommendations by AllianceBernstein L.P.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© AllianceBernstein

Read more commentaries by AllianceBernstein