A number of myths exist about value investing as it pertains to timing the economic cycle, interest rates, and elections. Dispelling these misconceptions may open a window of opportunity for investors in this year’s second half.

Bill Nygren, CFA, CIO-U.S. and PM at Harris | Oakmark, discussed three current value investing myths this year in a recent video. Collectively, the three myths underscore why it’s important not to try to invest time in the space and instead maintain long-term exposure.

Value Investing Requires Economic Flourishing

Some investors may fall into the trap of thinking that value stocks only offer strong performance during periods of robust economic growth. However, the opportunity exists for value investing in almost any economic environment, short of a strong recession.

Value stocks, like virtually all other stocks, perform relatively poorly when a significant economic recession strikes. In times of varying economic growth and real GDP levels, value stocks historically offer positive returns for investors.

“In economic environments when GDP growth has been between minus four all the way up to above six percent, value investing has delivered pretty decent returns,” explained Nygren.

The Russell 1000 Value Index generated a 1.1% average quarterly return when real GDP fell between -4 and -2% in a period between March 1979 and March 2024, according to Morningstar data calculated by the firm. The Index generated its strongest quarterly returns (4.3%) when real GDP fell between 2-4%. This was followed closely by a 4% return with real GDP levels of 4-6%. According to the historical data, the Index only generated a negative return when real GDP fell below -4%.

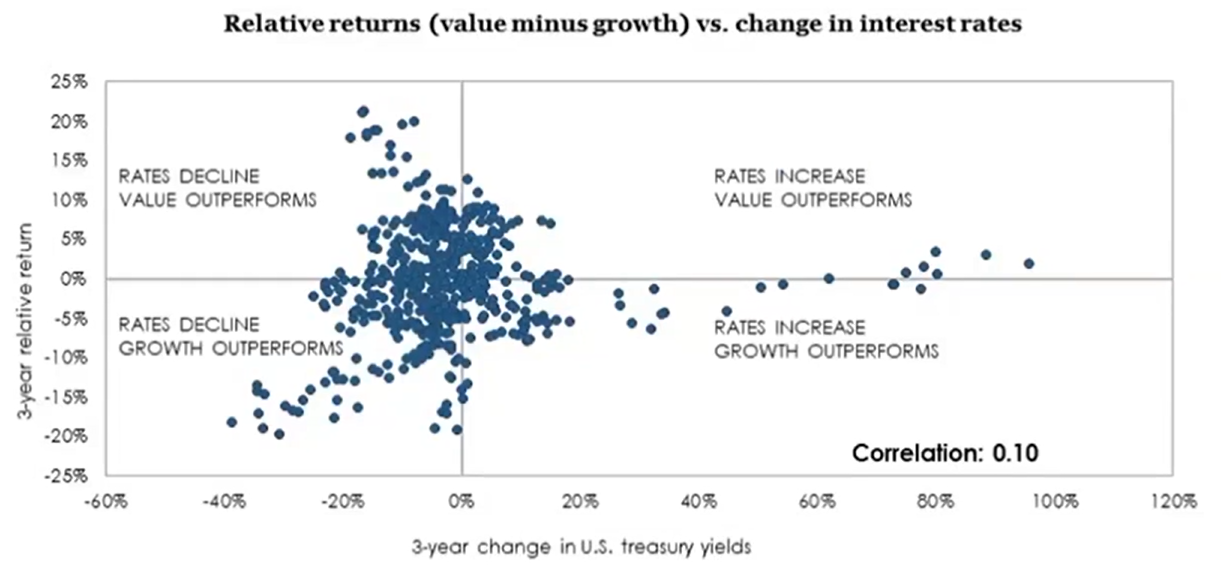

Value Stocks Only Perform in Rising Rate Environments

The firm also charted the three-year annualized returns of the Russell 1000 Value Index versus the Russell 1000 Growth Index between March 1979 and 2024. They compared the returns relative to the 3-year change in U.S. Treasury yields.

Image source: Natixis Investment Managers

They found that strong declines in interest rates benefited growth stocks, an unsurprising outcome. The remainder of the time, they found just a 0.1 correlation of relative returns to yields. “Unless you think rates are in for a very, very significant drop, you should ignore them as you think about how much of your portfolio you want allocated to value,” Nygren said.

Election Years Lead to Stock Underperformance

Investors tend to fixate on the potential for volatility in markets during election years. Some may even conflate volatility for reduced return potential for stocks, a myth that holds little weight when looking back historically.

“The reason the myth exists: non-election years have been a little bit better for both the S&P and for value investors,” explained Nygren.