The US presidential election is likely to be a tight contest and the noise will also likely intensify as November approaches. Tax policy differences are always top considerations, especially for municipal bond investors. Comparing proposals on both sides could help investors prepare for either outcome.

Trump-Era Tax Cuts Are Expiring…Or Maybe Not

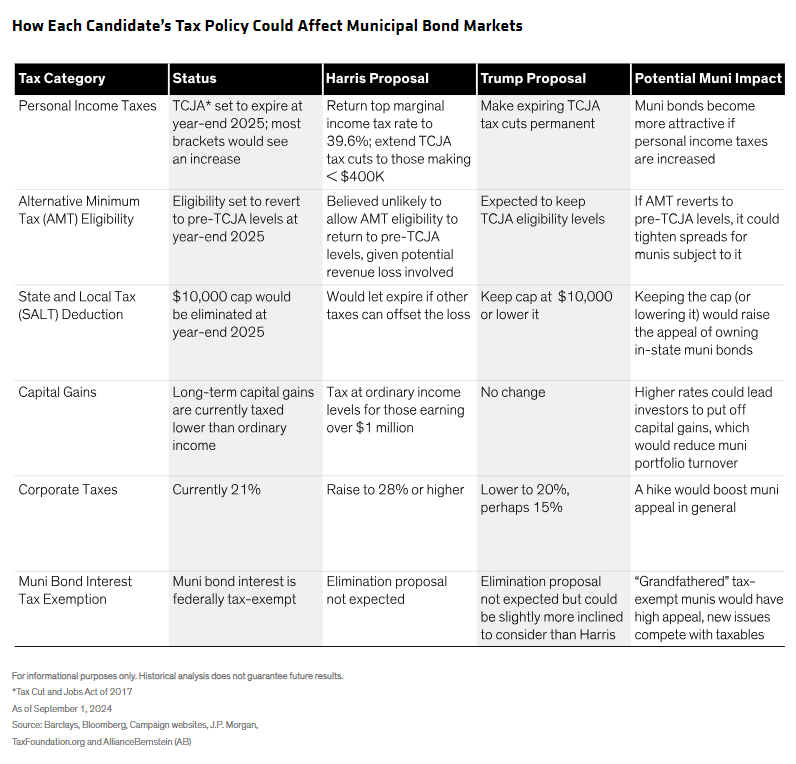

The sharpest policy contrasts relate to key provisions of 2017’s Tax Cuts and Jobs Act (TCJA), some of which are due to expire at the end of 2025. They include personal tax rates, Alternative Minimum Tax (AMT) thresholds, and State and Local Tax (SALT) deduction limits (Display).

Income Tax Rates: Fine Tuning on Both Sides

Personal income taxes are a particularly hot topic this election cycle, because the TCJA’s significant rate reductions for middle-class voters will eventually sunset. Former President Donald Trump is expected to favor extending all the Act’s tax cuts.

Vice President Kamala Harris is expected to extend tax cuts under the TCJA, but only to households earning less than $400,000 annually. Meanwhile, those making over $400,000 would see an increase in personal taxes and Medicare surcharges, for a combined maximum tax rate of 44.6%.

What it means for munis—Higher personal income taxes will make municipal bonds more attractive, considering the federal tax exemption on their interest income.

The AMT: Eligibility Could Change

For investors subject to the AMT, the rules can affect the tax-exempt status of some municipal bonds. By significantly raising the AMT exemption and income phaseouts, the TCJA sharply reduced the number of AMT-eligible taxpayers to about 200,000 from 5 million. If the higher levels expire, it could widen AMT eligibility again, to what would now be estimated to be over 7 million taxpayers.

The Harris camp believes that higher AMT provisions pose a substantial cost in lost revenue and might prefer to let them expire. As with most of the TCJA provisions, Trump would likely push to extend the current levels.

What It means for munis—We think it’s unlikely that the higher AMT exemption will be phased out—policymakers on both sides are weighing the fiscal impact of having so many middle-class taxpayers once again become eligible. Over the longer term, a permanent extension could cause spreads to decline on municipal bonds subject to the AMT, which is about 4% of the market.

State and Local Tax (SALT) Deductions: It’s a Question of Limits

TCJA’s $10,000 limit on SALT deductions has generally made the tax-advantaged benefit of muni bonds more attractive, especially in states with higher property taxes. But without changes, the cap will sunset at the end of 2025 and the SALT deduction will become unlimited again.

Trump is not expected to support removing or raising the cap and could possibly entertain lowering it. Observers say that Harris could be swayed to allow the cap to expire if the potential revenue loss can be offset through alternative tax sources.

What it means for munis—Keeping the cap (or lowering it) would raise the appeal of munis and other in-state investments.

Corporate Taxes: Not Much Daylight Between the Two Candidates

Harris advocates raising the corporate tax rate from 21% to 28%, significantly down from a 35% target she eyed during her 2020 primary run. Trump prefers to keep the 21% rate, which became permanent under the TCJA, but has also tested the reaction to 20% “for simplicity,” or even 15%, which would put it among the world’s lowest.

What it means for munis—A higher corporate tax rate would make municipal bonds more attractive to banks and insurance companies—which use them in investment portfolios—and be a modest tailwind for the asset class.

Capital Gains: Distinct Differences, but Not Much Impact from Either

Harris wants to tax long-term capital gains at the same rate as short-term gains and ordinary income for households making over $1 million. This change would push the long-term rate from 20% to 39.6% for the highest earners, and to 43.4% when factoring in the 3.8% Medicare surcharge.

Trump is not expected to change the current capital gains tax rate.

What it means for munis—There’s a chance higher capital gains taxes could lead investors to delay generating them, which could broadly lower muni portfolio turnover.

Is Muni Tax Exemption at Stake?

Think tanks on both sides of the political aisle suggest that eliminating the federal tax exemption on municipals could bring new revenues to offset those lost when key TCJA provisions expire.

We think the elimination scenario is remote, and neither candidate has indicated a preference—perhaps seeing slim benefit relative to potential blowback, such as a massive reaction from state and local governments. Also, the revenue foregone from the muni exemption is a tiny portion of the overall projected budget through 2033.

What it means for munis—On the off chance the exemption is removed, existing tax-exempt munis would likely be “grandfathered,” making them more attractive than newer, non-exempt issues. Otherwise, expect the status quo.

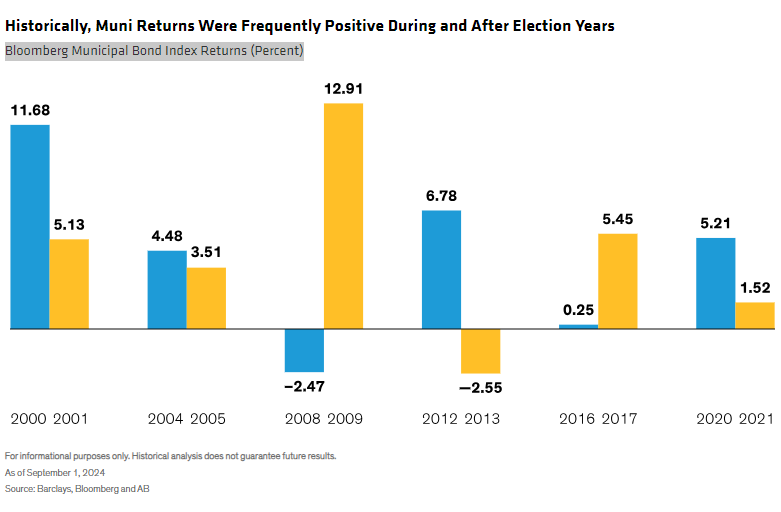

A Historical View: Muni Returns Have Been Agnostic to Election Cycles

Uncertainty over shifting tax policies isn’t the only driver of muni investor jitters. Elections tend to spark worry, but we think there’s solid evidence that they shouldn’t.

Historically, presidential elections have generally had limited bearing on muni market returns. Republicans and Democrats each won three elections since 2000, and muni bond returns were positive for each election calendar year and the year after in four of the six periods (Display).

We believe that powerful macro events—not election anxiety—factored into the 2008 and 2013 muni downturns, particularly the global financial crisis and taper tantrum, respectively. 2016 may have been an exception, when Trump’s win surprised a market that hadn’t accounted for his tax policies. Despite a sharp sell-off that November, however, the market rebounded in December and advanced well into positive territory through 2017.

Neither candidate’s victory would seem to pose a muni market surprise like 2016. The political climate will likely intensify in the coming months, which is all the more reason to focus on the bigger picture—which is that munis remain exceptionally attractive today. Yields are still high, valuations are compelling, and issuer fundamentals are strong. In our view, this makes munis a worthy candidate for long-term investors.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein