Positioning Ahead of the Fed: ETFs for a Lower Rate Era

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe first cut is the deepest — so they say. As with all complicated relationships, this mantra may certainly ring true for the Federal Reserve and the markets — at least from a psychological standpoint. Recent Fed commentary, coupled with the latest dose of economic data, has crystallized investor confidence in rate cuts coming in less than a week.

Inflation has quieted and the jobs market continues to soften, with hiring falling below even pre-pandemic levels. Right now, fed funds futures are pricing in 85% odds of a quarter-point trim.

Fed Governor Christopher Waller said the committee will proceed carefully with cuts and can always act “quickly and forcefully” should the labor market continue to deteriorate. He also said he would support “front-loading cuts” if appropriate.

After three years of rate hikes, investors are ready to chart a course through the Fed’s lower-rate regime.

Rising Tide to Lift All Boats

First rate cuts have historically been hugely bullish for stocks. Since 1970, the S&P 500 has risen an average of 18% one year following the first cut in non-recessionary periods. Broad-based vanilla equity ETFs offer the most straightforward exposure, but other products offer more nuanced ways to help investors capitalize on rate cuts.

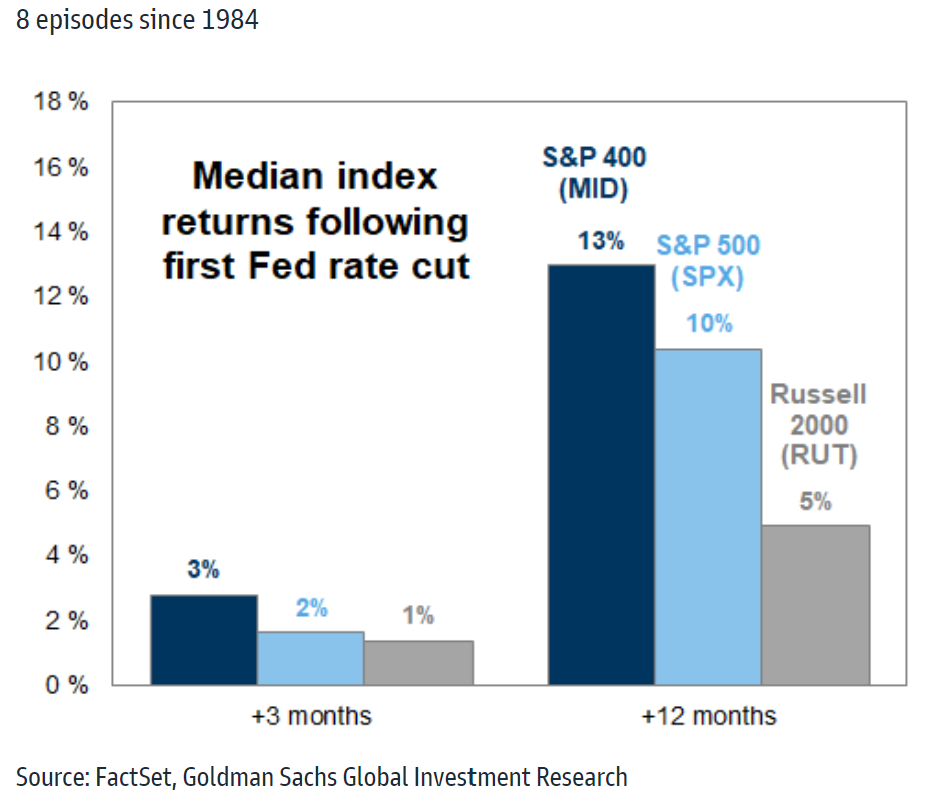

Small-caps and midcaps have felt the sting of rising rates more acutely than their large-cap counterparts, and stand to benefit most from lower borrowing costs. Earnings have also improved, and the valuation gap between large and small- to midcap companies is wider than ever these days, presenting opportunities for funds like the Vanguard Small Cap ETF (VB), the iShares Core S&P Small-Cap ETF (IJR) and the Avantis U.S. Small Cap Value ETF (AVUV), all of which have seen north of $3 billion in net inflows this year. The VictoryShares Small Cap Free Cash Flow (SFLO), which screens out small caps, is a relatively new entrant but has already crossed the $100 million mark in total assets within a year of trading. SFLO takes a more forward-looking, more liquid approach than many of its peers.

Rate-Sensitive Sectors

Despite tech’s dominance, utilities are now the best-performing sector in the S&P 500, up more than 19% year to date — with tech now the biggest loser in the third quarter. Utilities also boast some of the highest free cash flow yield on the market. That's a reflection of piping hot demand for energy to power up AI data centers. Bank of America just upgraded the sector to overweight from market weight, recommending investors put more money to work in utilities and less in tech.

The $18 billion Utilities Select SPDR Fund (XLU) has returned 22% year to date and charges 0.09% in fees. The Global X U.S. Infrastructure Development ETF (PAVE) — which invests in companies tied to the production of raw materials, heavy equipment, and construction — has seen $1.5 billion in inflows.

REITs have finally broken out of their rut and attracted investor interest again over the summer. Lower mortgage rates should draw more buyers back into the market, while homeowners who were previously unwilling to sell should now add much-needed inventory back onto the housing market. The Real Estate Select Sector SPDR Fund (XLRE) and Vanguard Real Estate ETF (VNQ) are key players in this space, with more than $1 billion in inflows each.

Consumer staples are also starting to turn a corner. The SPDR Consumer Staples ETF (XLP) has seen $1.2 billion in new money over the past month.

Preferred Stocks & Dividend Growers

Preferred stocks, which typically pay fixed returns, are considered hybrid debt/equity instruments and tend to rise in value as interest rates decline. The Global X U.S. Preferred ETF (PFFD) invests primarily in the preferred stocks of banks and utilities, offering up healthy yields and monthly dividends — while VanEck's Preferred Securities ex-Financials ETF (PFXF) provides access to preferreds for investors unwilling to bet on the banking sector.

Pure dividend plays, like the Capital Group Dividend Value ETF (CGDV), can provide a steady income stream. The fund charges 0.33% and actively owns high-yielding common stocks from proven dividend payers.

Going for Growth: High-Duration Tech

Historically, lower rates have been a boon for high-duration, growthier stocks, particularly in the technology sector. A lower discount rate for future cash flows equates to higher discounted valuations. Despite concentration risks, tech is the only sector to have suffered a correction of 10% or more this year. The Invesco QQQ Trust (QQQ) fell more than 10% from its July high. Smaller growth companies can also borrow more cheaply to fund growth initiatives, spurring on more investment and expansion. The Vanguard Russell 2000 ETF (VTWO) and Invesco S&P SmallCap Momentum ETF (XSMO) are the two most popular small-cap growth plays this year.

Fixed Income on Fire

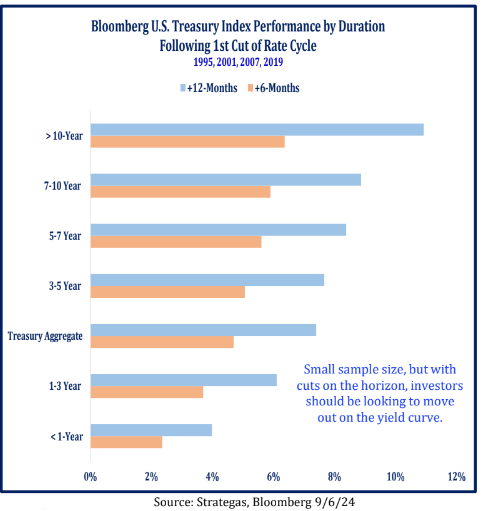

The anticipation of rate cuts has already lit a fire under Treasuries and bond ETFs across the duration and credit quality spectrum. The yield on the 10-year Treasury note has sunk to levels not seen since the wake of last year’s regional banking crisis — hovering around 3.65%. Many who sought refuge in short-term Treasuries are now looking to take on more duration to lock in yields and enjoy capital appreciation.

Investors may look to the SPDR Portfolio Long Term Treasury ETF (SPTL) and the iShares 20+ Year Treasury Bond ETF (TLT), which owns long-dated bonds with maturities of 20-30 years. Both have enjoyed massive inflows this year — to the tune of $3 billion and $11 billion, respectively. Per Strategas, the long duration bucket (+10-years) hosts an average six-month gain of 6.4% post-first cut versus 2.3% for cash-like instruments.

Investment-grade corporate bonds, such as those in the Vanguard Long-Term Corporate Bond ETF (VCLT) and iShares 10+ Year Investment Grade Corporate Bond ETF (IGLB), offer a balance between risk and return, as spreads tighten. Investors have also embraced credit strategies like the actively managed SPDR Blackstone Senior Loan ETF (SRLN) and BlackRock Flexible Income ETF (BINC) to pursue continued higher income as broad-based rates fall.

Gold ETFs: Back in the Game?

Gold ETF flows have picked up steam again after sputtering out early this year. The SPDR Gold Trust (GLD) has suffered net outflows this year, but has finally seen money pour in — $1.3 billion in the past four weeks alone.

The SPDR Gold MiniShares Trust (GLDM) remains the most popular for its cost-effectiveness — with a haul of $918 million this year, the cheapest on the market at just 0.10%. The VanEck Merk Gold ETF (OUNZ) and the abrdn Physical Gold Shares ETF (SGOL) are the second and third most popular gold ETFs this year, respectively.

The precious metal also stands to benefit from a weaker dollar and has historically done well in times of economic distress. Gold has yielded higher returns than the broader stock market during six of the last eight recessions.

While the frequency and magnitude of rate cuts remain in question, ETFs offer investors myriad options with which to strategically position themselves to prosper in lower rate climes while minimizing volatility.

For more news, information, and analysis, visit VettaFi | ETF Trends.

VettaFi LLC (“VettaFi”) is the index provider for SFLO, for which it receives an index licensing fee. However, SFLO is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of SFLO.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All