Core Score: How a New Approach to Credit Investing May Harness More Alpha

Historically, investors have struggled to add meaningful alpha through security selection. A dynamic new credit scoring approach could change that.

Given the breadth and diversity of the corporate credit universe, hand picking individual securities can be inefficient. That’s why we’ve developed a powerful new scoring methodology that systematically harnesses quantitative and fundamental research to generate new sources of outperformance (alpha).

Size of Bond Universe Makes Security Selection a Challenge

The credit market’s complexity and sheer scale underscores the challenges of generating alpha through bond selection. The global corporate universe comprises nearly 20,000 securities, which can make security selection both time-consuming and overly subjective. Partly for this reason, many portfolio managers aren’t able to generate much alpha from security selection, and instead lean more on levers like beta timing and sector rotation.

We believe that’s a missed opportunity. In any market—but especially today’s—security selection has the potential to generate meaningful alpha. Historically, the heightened volatility and desynchronization between interest-rate regimes that we’re seeing now has contributed to increased dispersion and idiosyncratic opportunities at the issuer and security levels.

Fortunately, in our view, investment managers can generate potential alpha by combining quantitative methods with bottom-up fundamental research. The challenge lies in efficiently converting vast quantities of data into better investment outcomes.

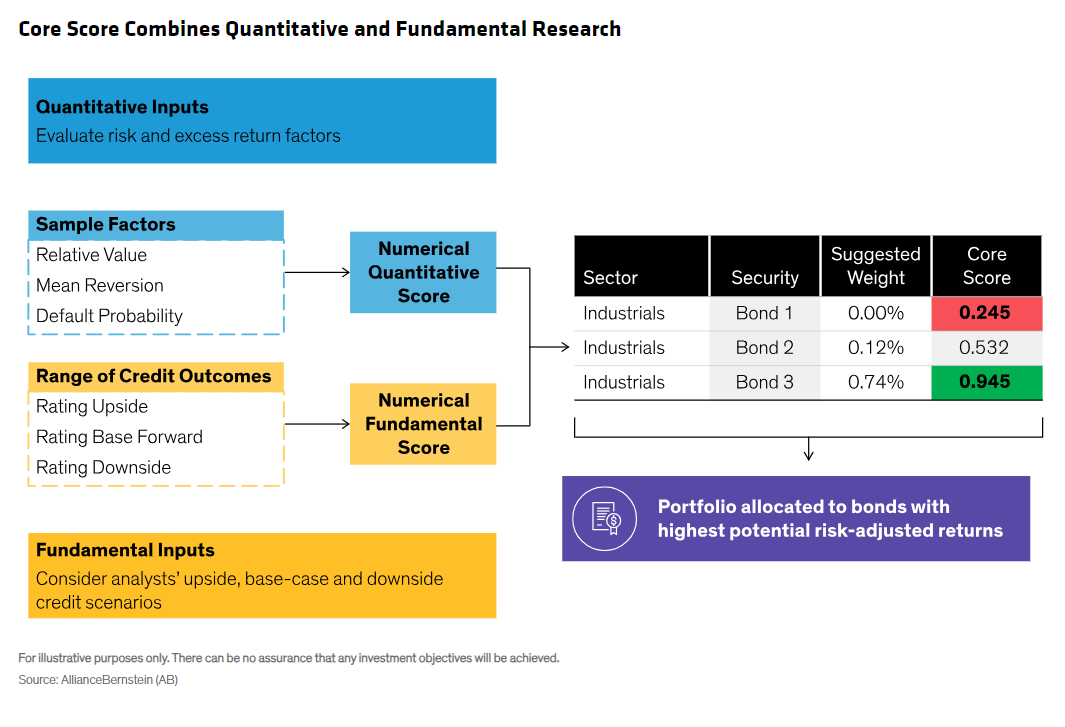

Our approach systematically funnels both fundamental and quantitative inputs into a proprietary scoring model that ranks bonds by their attractiveness. We call this a “core score.”

Here’s how it works.

Balancing Fundamental and Quantitative Inputs

At the heart of the core-score methodology is traditional fundamental research. Credit analysts conduct thorough due diligence of issuers and securities, and assess various outcomes for each bond—including a base case, an upside case and a downside case. This range of outcomes is then used as a part of our fair-value model to determine a bond’s attractiveness relative to current market pricing. This informs the fundamental score for each security.

The second part of the process involves quantitative research. Analysts filter bonds through various predictive factors with demonstrable links to historical outperformance, such as momentum, relative value or default probability. Once securities are assessed through a factor lens, each bond is assigned a quantitative score that reflects our quantitative research team’s view of its attractiveness.

The fundamental and quantitative scores are then combined. The result is a single core score for each bond (Display). The core score informs our understanding of a bond’s return potential relative to its risk and allows portfolio managers to consistently implement our best ideas in client portfolios. We believe this increases the probability of generating alpha from security selection.

A Powerful Tool for Today’s Global Credit Market

What makes the core score so powerful?

There’s no substitute for sound fundamental research, but the enormity of the global bond market also requires a quantitative process that provides breadth of coverage. Our core-score model makes research more scalable and targeted—allowing us to make informed decisions about many individual securities. Ultimately, we believe that consistently identifying many mispriced securities with strong risk-adjusted return potential is a smarter way to manage bond portfolios.

And because our methodology is data driven, it’s efficient and effective—not unlike daily exercise that provides incremental benefits that add up over time. The core score is refreshed daily for each bond in a benchmark index—including existing and new issues. That’s significant, as there can be more than 40 tranches comprising dozens of new issuers on any given day in the US investment-grade market alone, to say nothing of the volume of global issuance.

Less visible to investors is the flexibility the core score provides—including more time for analysts to engage with issuers* to gain unique, forward-looking insights, and the ability to respond to market pricing shifts more dynamically. This is especially important in today's fast-moving market, when it’s critical to capture opportunities that might otherwise be missed.

While a core score makes sense in any market, we believe it’s especially relevant given today’s global credit backdrop and increased volatility. In our view, investors can’t afford to miss out on idiosyncratic opportunities as they arise. As we see it, the core score could provide opportunistic investors with a powerful new tool for harnessing alpha.

*AB engages issuers where it believes the engagement is in the best interest of its clients.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.