As the Fed begins cutting rates, October’s surprisingly strong US employment report only adds to the data pointing to a soft landing, despite lingering concerns of a downturn. We expect the economic expansion to continue, which has important implications for multi-asset strategies.

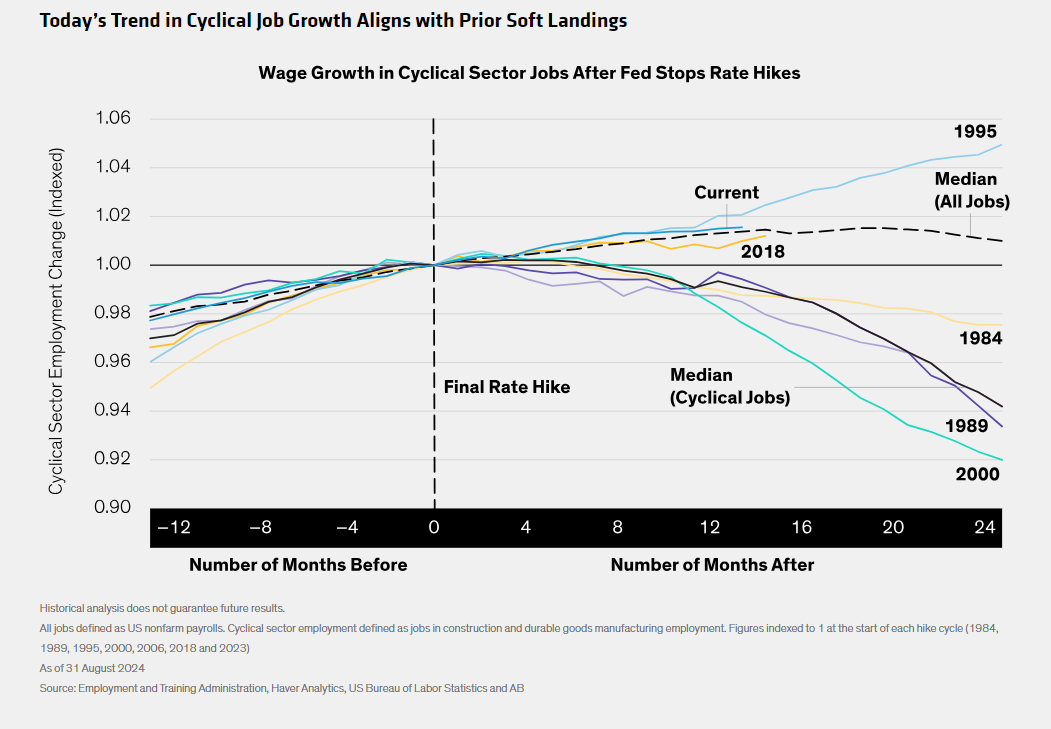

Resilience so far in cyclical, rate-sensitive employment increases our confidence. Growth in construction and manufacturing jobs has remained robust since the Fed’s last rate hike in July 2023 (Display), benefiting from very resilient demand for new homes. When this was the case at the end of two prior tightening cycles, soft landings occurred. When the Fed stopped hiking prior to recessions, these sectors were showing early signs of labor market weakness.

Equities Should Benefit; Bonds May Get Bumpy

Policy easing and economic weakness clearly don’t always go hand in hand. The current easing cycle is the normalization of exceptionally tight policy to address 2022’s inflation shock. We expect the growth backdrop to continue to support risk assets, especially high-earning US stocks as well as select emerging markets, which present diverse opportunities.

We expect bond yields to gradually descend, though it could get bumpy on the way down as the Fed recalibrates to neutral. In this environment, we believe government bonds will once again offer attractive hedges to risk assets.

For multi-asset investors, a positive growth outlook and inflation normalization are two of many inputs that inform strategic and tactical allocations in a diversified approach. As always, investors should remain flexible to respond to changing conditions.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.