Given that most tax provisions of the Tax Cuts and Jobs Act are currently set to expire at the end of 2025, including the lifetime estate and gift tax exclusion, a review of estate plans seems prudent. While the future of estate and gift-tax policy is uncertain, there are important actions to consider now that could have an impact on the overall tax efficiency of an estate plan.

Here are five estate planning strategies to consider that could maximize a plan’s tax efficiency.

Plan for the 10-year rule on inherited IRAs

Since most non-spouse beneficiaries will have to liquidate inherited IRAs within 10 years following the death of the account owner and likely pay taxes upon distribution, there may be strategies to transfer retirement savings in a tax-smart manner to the next generation. For example, consider naming heirs who are more likely to be in lower tax brackets as IRA beneficiaries. For 2025, there are new rules for inherited retirement accounts that need to be followed. Beginning this year, many heirs subject to the 10-year distribution rule will also, at a minimum, need to take a minimum distribution based on their remaining life expectancy. This applies on inherited account where the original owner died after reaching their required beginning date (RBD). For more details see our article, “Unwinding the 10-year rule for inherited retirement accounts.”

Review estate planning documents and strategies

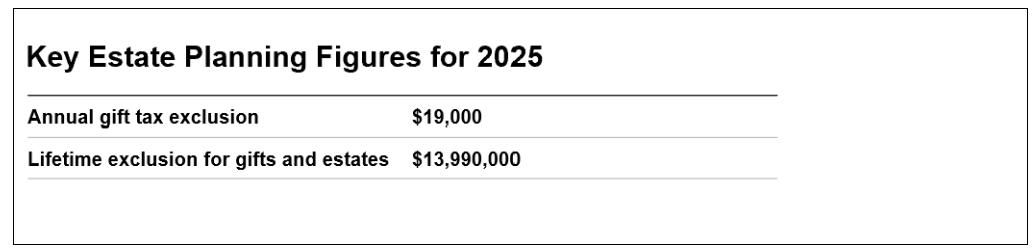

Beginning with tax law changes effective in 2018, the increase in the lifetime exclusion amount for gifts and estates ($13,990,000 per individual in 2025) may have unintended consequences for some individuals and families with wealth comfortably under that threshold. They may think that they do not have to plan for their estate. However, taxes are just one facet of estate planning. It is still critical to plan for an orderly transfer of assets or for unforeseen circumstances such as incapacitation. Strategies to consider include proper beneficiary designations on retirement accounts and insurance contracts, wills, powers of attorney, health care directives and revocable trusts. Additionally, existing trusts should be reviewed to determine if changes are needed based on the current gift and estate tax thresholds.

Plan for potential state estate taxes

While much attention is focused on the federal estate tax, certain residents need to know that many states have estate or inheritance taxes. There are several states that are “decoupled” from the federal estate tax system. This means the state applies different tax rates or exemption amounts. A taxpayer may have net worth comfortably below the $13,990,000 exemption amount for federal estate taxes but may be well above the exemption amount for their state. For example, estates in Oregon with net worth higher than $1 million may be subject to state taxes. It is important to consult with an attorney on specific state law and potential options to mitigate state estate or inheritance taxes

Develop a strategy for low-cost-basis assets

Ensure stepped-up cost basis is maintained when property is transferred at death. For example, careful consideration should be made around lifetime gifts that may jeopardize a step-up in cost basis on property at death. When property is gifted, the party receiving the gift generally assumes the original cost basis. Additionally, certain trust provisions may be utilized to ensure that property receives a step-up in cost basis at death.

Expand use of 529 accounts for education savings

529 college savings plans are great tools for funding a variety of education-related expenses including K-12 tuition in some states, qualified apprenticeship programs and higher education expenses. Additionally, a special provision allows individuals to front-load five years of annual gifts as a contribution into a plan. With the annual gift tax exclusion at $19,000 for 2025 that means that up to $95,000 (or $190,000 for married couples) can be contributed into a 529 account while not exceeding current gift limits (assuming no other gifts are made during the next five years). This may allow for a larger removal of assets from an estate once the contribution into the 529 account has occurred.

Seek advice

Consult a qualified tax or legal professional and your financial advisor to discuss these types of strategies. It is critical to work with a professional who has knowledge of your specific goals and situation.

For more planning strategies, see “Ten income and estate tax planning strategies for 2025.”

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

Copyright © 2024 Franklin Templeton. All rights reserved.

Ref. 3936810

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Franklin Templeton

Read more commentaries by Franklin Templeton