Rebuilding Resilience in 60/40 Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey points

- Heightened fiscal, trade, and policy dynamics challenge the performance, stability, and diversification potential of 60/40 portfolios.

- Strategies that look beyond directional market opportunities to take advantage of return sources of dispersion in idiosyncratic risk may help rebuild portfolio resilience.

- We highlight two strategies as potentially better ways to play stocks (BDMIX) and bonds (BIMBX) in this new regime.

The 60/40 portfolio, where 60% is invested in stocks and 40% in bonds, is the initial starting point for many portfolios. The exact asset mix is often adjusted based on an investor’s time horizon, risk tolerance, and financial goals, but the simple, proportional stock-bond combination is what is often considered a “balanced” portfolio.

But in recent years, the driving forces behind the success of the 60/40 have come under pressure, first with post-COVID inflation uncertainty, and today with heightened fiscal, trade, and policy changes. What does this mean for portfolio construction? Rebuilding portfolio resilience may require more dynamic alternatives to traditional stock and bond allocations.

The 60/40 portfolio today

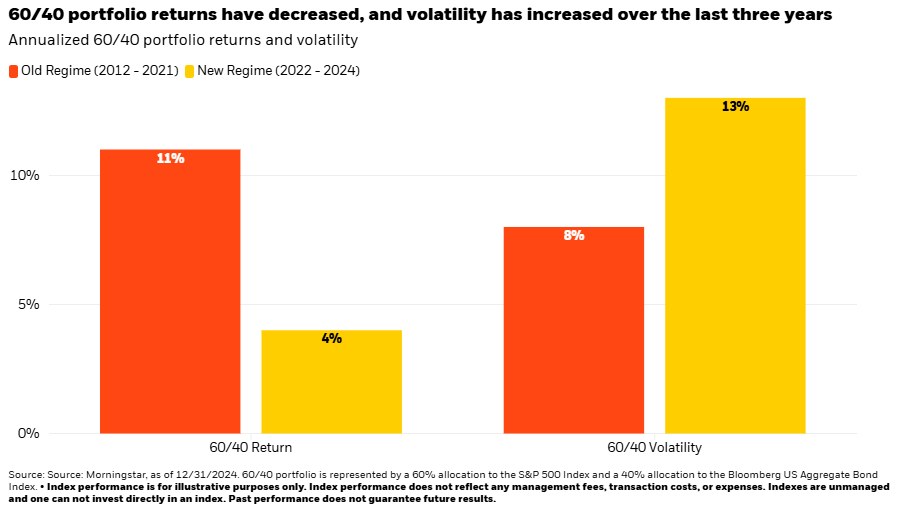

The shift to a world of higher overall interest rate volatility amid greater macroeconomic, policy, and market uncertainty is shaping a new regime for investing. The below chart highlights the impact on 60/40 portfolio outcomes, showing reduced return potential and increased volatility over the last three years relative to the previous decade.

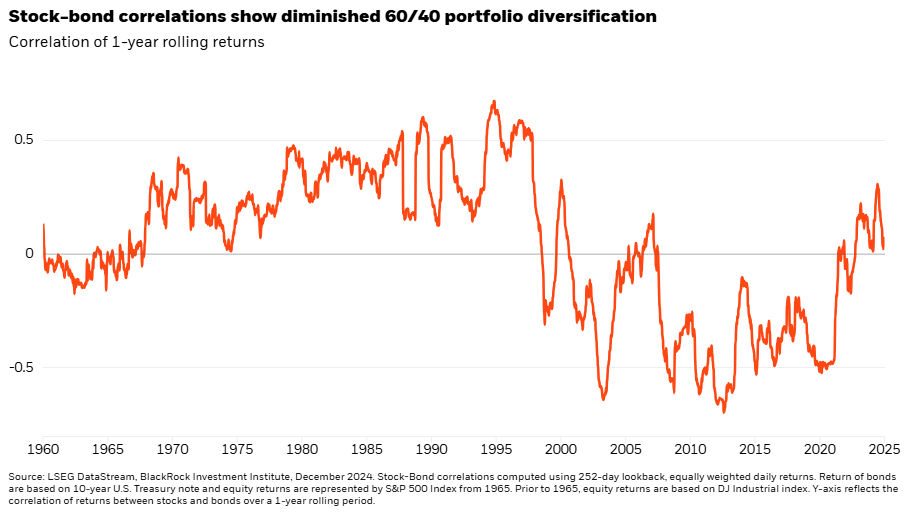

These characteristics of the “new regime” also challenge the diversification of 60/40 portfolios. The chart below shows the rise in stock-bond correlations from consistently negative levels that persisted for over a decade following the Great Financial Crisis (and mostly negative for the decade prior). Among other factors, the transition from an environment of inflation remaining below the US Federal Reserve’s 2% target to the current backdrop of above-target inflation has challenged this diversifying relationship. Since the start of 2022, bonds have lost money in 14 of the months where stocks were negative, with the US Aggregate Bond Index participating in nearly half the downside of the S&P 500 Index on average.1

The hedging efficacy of bonds has also become more nuanced over time, highlighting the importance of where investors hold duration exposure along the curve. For example, despite the start of the Fed’s rate-cutting cycle last year, long-term yields increased due to factors such as inflation and rising term premia. These dynamics dominated the direction of long-end rates, leaving them less responsive to the path of Fed policy than in past cutting cycles. This has made it so that simply owning traditional bonds hasn’t delivered the same performance and hedging results as historically.

A more granular view of stock-bond correlation broken down by maturity shows a higher degree of ballast in shorter-term bonds where inverse yield movements have been the strongest during recent risk-off episodes. We did see a return of longer-term bonds providing ballast as recession fears emerged in Q1 of 2025,2 reflecting the expectation for policymakers to swiftly react to any weakening in the economy while tolerating above-target inflation.

But overall, the potential for continued sticky inflation, rising term premia from historically suppressed levels, and the impacts of fiscal and broader policy dynamics may continue to undermine the performance and hedging efficacy of longer maturities. However, we should also note the potential that a more significant increase in long term interest rates could prompt a larger fiscal and/or monetary policy response that attempts to contain the term premium widening. The prospects for stagflation where longer-term yields rise with higher long-run inflation expectations (while shorter-term bonds follow the Fed policy trajectory) underscores the importance of where interest rate exposure is held.

In addition to these implications for bond market performance and diversification, today’s uncertain and challenging macroeconomic and policy backdrop will likely remain a source of volatility in the stock market with the potential for frequent market reversals and rapidly shifting narratives ahead. This type of investment backdrop creates an opportunity to rethink portfolio allocations by looking beyond broad market index exposures and beta-tilted strategies.

Rebuilding portfolio resilience with new return sources

One approach is considering alternatives to stocks and bonds that are less dependent on the overall direction of markets to generate returns. For example, a strategy that can invest long and short across the stock market can target a different and diversifying return source that isn’t captured in the traditional 60/40 construct.

This alternative return source is called dispersion, which is the difference in individual security returns across the market. Factors like higher interest rates and macroeconomic uncertainty have contributed to a world shaped by higher dispersion in company results, creating a rich opportunity set for long/short alpha strategies at a time of potentially more muted directional market returns.

Long/short strategies take advantage of cross-sectional dispersion by forecasting which stocks will outperform and underperform on a relative basis—regardless of whether overall markets are rising or falling. The result is a return stream that can be uncorrelated to broad markets with the potential to enhance the “60” or the “40” of portfolios depending on the goal of the strategy.

Better ways to play stocks and bonds?

Rebuilding the 60: Our Global Equity Market Neutral Fund (BDMIX) seeks to generate consistent stock-like returns with less volatility and a near-zero correlation to the market. The strategy invests across ~7,000 global equities with a relatively even split of long and short positions, leveraging data-driven insights to dynamically adapt and exploit relative winners and losers as markets evolve.

Rebuilding the 40: Our Systematic Multi-Strategy Fund (BIMBX) is designed to be a better way to play fixed income, targeting outperformance with less volatility compared to traditional bonds. We do this by combining directional fixed income exposure with long/short alpha strategies. The alpha component provides an uncorrelated, defensive return stream that adds an alternative source of diversification to traditional duration.

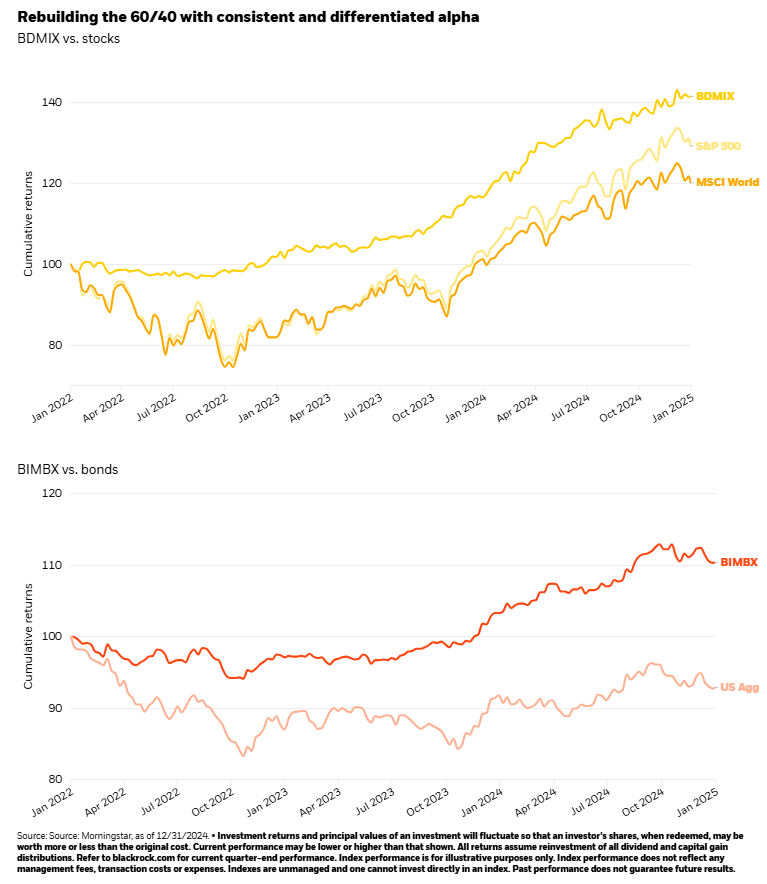

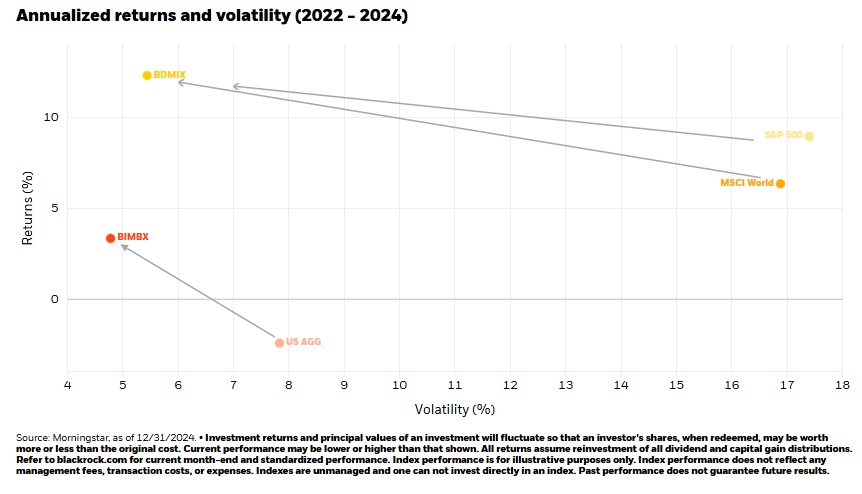

These strategies share the common link of harnessing cross-sectional opportunities, capitalizing on today’s elevated dispersion to enhance return potential and consistency while boosting portfolio diversification. The below charts show how over the last three years, these flagship strategies have consistently outperformed stocks (for BDMIX) and bonds (for BIMBX) across a wide range of market environments.

Importantly, these results have been achieved with less volatility than their traditional asset class counterparts. The low correlation between BDMIX and BIMBX (0.11 as of 12/31)3 suggests they have the potential to be complementary when used in the same portfolio.

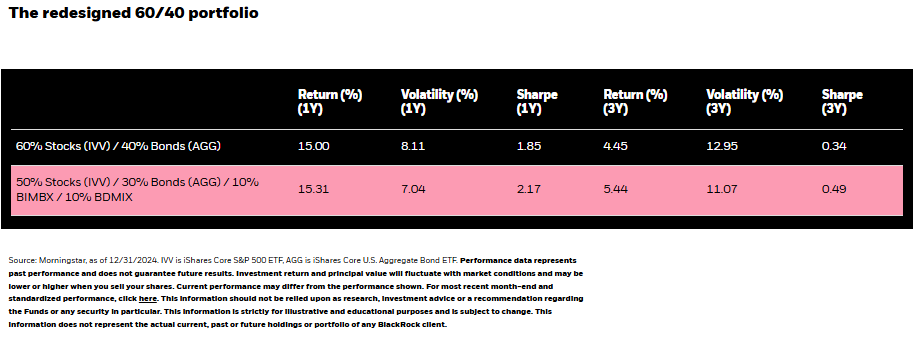

Rebuilding resilience in 60/40 portfolios

The below table illustrates the impact of adding 10% allocations to BDMIX and BIMBX, sourced from stocks and bonds, respectively. Compared to the 60/40 allocation, the “redesigned” portfolio has generated higher returns with lower volatility and more efficient risk usage (higher Sharpe ratio) over the 1- and 3-year periods.

Putting it all together

The 60/40 portfolio faces challenges in the new investment regime. Portfolios have become more volatile while diversification and return potential have decreased over recent years. Investors can build more resilient portfolios by considering different ways to play stock and bond markets—for example incorporating strategies that take advantage of new and differentiated return sources. These alpha-seeking strategies have the potential to turn market beta headwinds into tailwinds, taking advantage of higher volatility and dispersion to enhance portfolio outcomes.

1 Source: BlackRock USWA Market and Portfolio Insights Team, Morningstar, as of 12/31/2024. Average monthly stock returns in 14 months when S&P 500 Index was negative since 2022 were -4.5%, and bond returns for Bloomberg US Aggregate Bond Index were -2.2%.

2 Source: https://www.cnbc.com/2025/02/25/us-treasury-yields-investors-look-toward-key-home-price-data.html

3 Source: Morningstar, as of 12/31/2024. Correlation of 5-year daily returns.

Investing involves risks, including possible loss of principal.

Key risks of BDMIX: The fund is actively managed and its characteristics will vary. Stock values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. The issuers of unsponsored depositary receipts are not obligated to disclose information that is, in the United States, considered material. Investing in long/short strategies presents the opportunity for significant losses, including the loss of your total investment. Such strategies have the potential for heightened volatility and in general, are not suitable for all investors. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. The fund may engage in active and frequent trading, resulting in short-term capital gains or losses that could increase an investors tax liability. Short-selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short-sale proceeds in other investments. Investing in small- and mid-cap companies may entail greater risk than large-cap companies, due to shorter operating histories, less seasoned management or lower trading volumes.

Key risks of BIMBX: The fund is actively managed, and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage-or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of US government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. The fund may use derivatives to hedge its investments or to seek enhanced returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. Effective 1/4/19, the Alternative Capital Strategies fund name was changed to the “Systematic Multi-Strategy Fund”. The Fund’s information prior to September 17, 2018 is the information of a predecessor fund that reorganized into the fund on September 17, 2018. The predecessor fund had the same investment objectives, strategies and policies, portfolio management team and contractual arrangements, including the same contractual fees and expenses, as the fund as of the date of reorganization. As a result of the reorganization, the Fund adopted the performance and financial history of the predecessor fund.

Diversification and asset allocation may or may not protect against market risk or loss of principal.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change. This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. Reliance upon information in this material is at the sole discretion of the viewer.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the value of debt securities. Credit risk refers to the possibility that the debt issuer will not be able to make principal and interest payments.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective. The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

Prepared by BlackRock Investments, LLC, member FINRA.

©2025 BlackRock, Inc. or its affiliates. All Rights Reserved. iSHARES and BLACKROCK are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0325U/S-4301582

A message from Advisor Perspectives and VettaFi: Advisors, do you want to join us at Exchange as a complimentary guest. Use the code APContributor25 when you register.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All