Getting a Grip on Uncertainty

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

An evolving macro regime

Sharp U.S. policy shifts and elevated uncertainty make it seem the world is upended. What matters now for investors is getting a grip on this environment’s defining features. We have long argued that we entered a new macro regime marked by profound transformations, shaped by mega forces that could lead to many very different potential outcomes over time – for the trajectory and makeup of the global economy, inflation, government debt and deficits or global trade. 2025 has put this new regime into sharper relief, with serious discussion about the potential for fundamental changes to the structure of global markets.

Put another way, the loss of long-term macro anchors that have underpinned long-term asset allocation for decades is a defining feature of this new regime. But the global economy can’t be revamped overnight. Immutable economic laws – on global trade and debt financing – exist that policy cannot ignore in the near term. Attempts to break them are akin to trying to break laws of physics – and defy gravity – in our view.

Nobody knows where the macro environment is ultimately headed. But understanding these policy limits makes us more comfortable staying pro-risk on a tactical horizon.

Losing long-term macro anchors

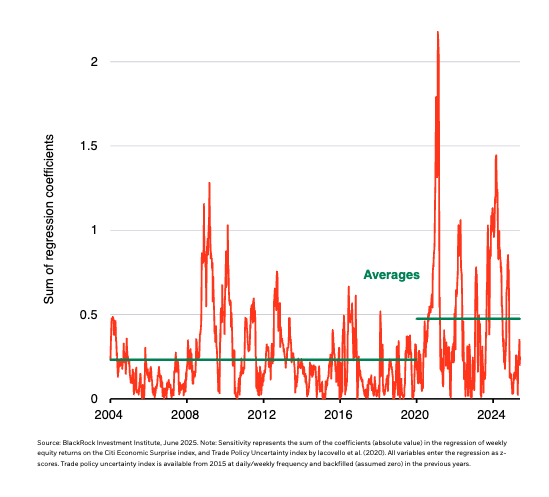

Geopolitical fragmentation, AI and other mega forces are reshaping the trajectory and makeup of the global economy. This is not a cyclical adjustment but a structural one that can lead to many very different outcomes. Elevated uncertainty is a given. We start to get to grips with it by identifying a core feature of this environment: the loss of long-term macro anchors that markets have relied on for decades.

Inflation expectations are no longer firmly anchored near 2% targets. Fiscal discipline is ebbing away. The compensation investors want for holding long-term U.S. Treasuries is rising from suppressed levels. And confidence in institutional anchors – central bank independence and the haven role of U.S. assets – has been shaken.

We think that requires a new approach to risk taking. With long-run economic trajectories now ever-evolving, one would expect investors to search data for signals about where things are headed. This is exactly what we’ve seen. Equity returns have become more sensitive to short-term data as investors try to infer what it means about both the near and long term.

Questioning the future

Equity sensitivity to macro and trade uncertainty, 2004-2025

World can’t change quickly

Immutable economic laws on trade and debt are constraining U.S. policy shifts – and can help investors navigate near-term uncertainty. We believe we now have more certainty about the near-term macro outlook than the long – a big change from the past.

One law limiting trade policy: supply chains can’t be rewired quickly without major disruption. Companies can’t just source products and inputs from elsewhere overnight without a halt in activity. We believe that rule was behind the rapid tariff carve-outs — such as exemptions for electronics from China — and why the U.S. and China soon restarted trade talks.

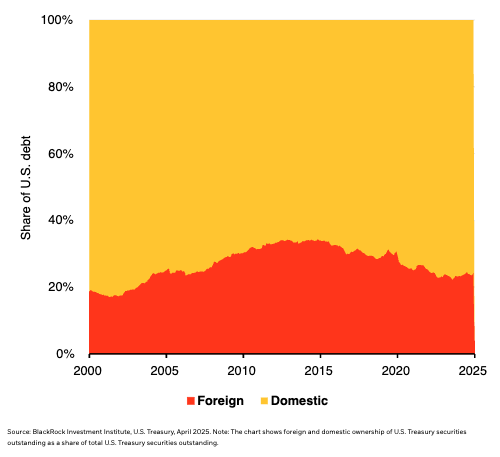

The second law is on debt: U.S. debt sustainability relies on big, steady funding by foreign investors, who hold about a quarter of it. Any falloff in foreign demand for Treasuries could spike yields and make borrowing costs so high that it forces a policy response. We think the tariff pause soon after the April 2 announcement was likely partly due to the yield spike. We see a fragile equilibrium – elevated debt, sticky inflation and higher interest rates – making U.S. Treasuries vulnerable to investors seeing them as riskier.

Foreign funding needed

Ownership of U.S. Treasuries, 2000-2025

Investing in the here and now

We have more certainty about the near-term macro outlook than the long term – an unusual situation for investors. So, we put greater weight on tactical views. That’s why our first theme is investing in the here and now. That favors U.S. equities and themes such as artificial intelligence. We stand ready to pivot depending on the ultimate impact of U.S. policy on the economy. We don’t think Europe can outperform yet without structural changes, but some of the steps Europe has taken give us optimism.

Since 2000, European equities have had many periods of outperformance over U.S. equities – but they have become increasingly rare. Yet those rallies never spurred questions about the role of U.S. assets as we’ve seen this year. We think the current economic setup still supports U.S. outperformance. We see scope for overall corporate earnings to stay solid even if U.S. growth is dented by tariff-induced disruptions and corporate caution

Limited rebounds

Ratio of European vs. U.S. equity total returns, 2001-2025

Taking risk with no macro anchor

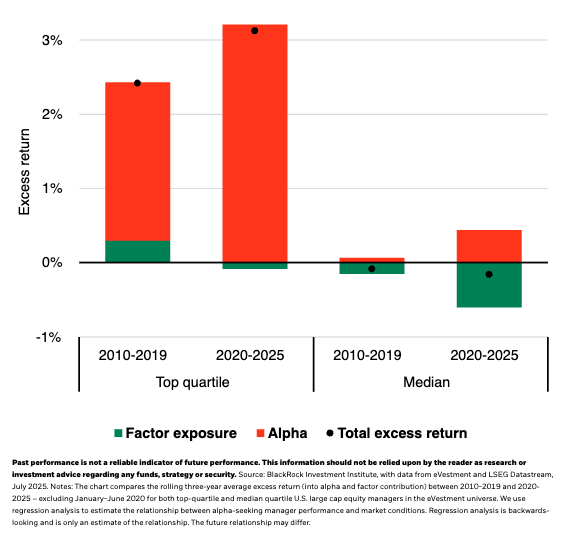

We believe this environment of transformation is better than the prior decade for achieving above-benchmark returns, or alpha. Our work finds that top-performing portfolio managers have delivered more alpha since 2020. And the median manager is seeing a bigger drag on returns from static factor exposures. That underscores how the volatile macro environment injects risk into portfolios that needs to be actively managed. That’s why taking risk with no macro anchor is our second theme.

Greater potential alpha on offer

Three-year excess returns of U.S. equity fund managers, 2010-2025

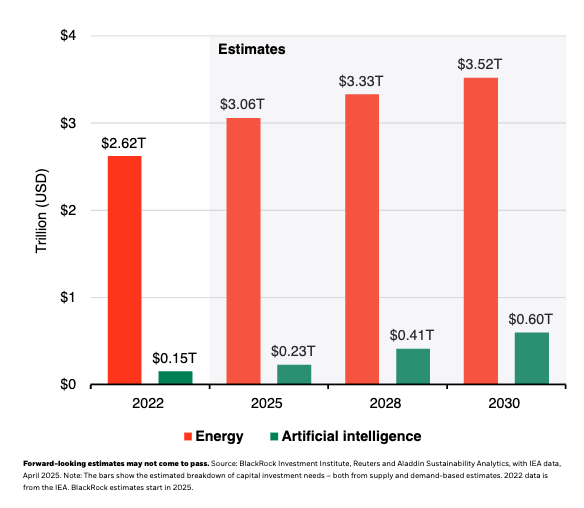

Finding anchors in mega forces

Even with the loss of long-term macro anchors, we believe mega forces are durable drivers of returns – and are finding anchors in mega forces, our third theme. Capital spending and infrastructure is at the heart of many mega forces. But big capital spending does not necessarily result in big returns, as we have seen with the energy transition and security theme. Instead, we need to track their evolution across and within asset classes, get granular with themes and constantly adapt to what’s priced in.

Tracking the investment waves

Energy and AI-related capital spending, 2022-2030

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Click here to download the PDF

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. The opinions expressed are as of July 2025 and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

In the U.S. and Canada, this material is intended for public distribution. In EMEA, in the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: + 44 (0)20 7743 3000. Registered in England and Wales No. 02020394. For your protection telephone calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock. In the European Economic Area (EEA): this is Issued by BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In Italy, for information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian. In Switzerland, for qualified investors in Switzerland: This document is marketing material. Until 31 December 2021, this document shall be exclusively made available to, and directed at, qualified investors as defined in the Swiss Collective Investment Schemes Act of 23 June 2006 (“CISA”), as amended. From 1 January 2022, this document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under art. 4 FinSA, please see the following website: www.blackrock.com/finsa. For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign Recognised Company registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738). In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorised and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 7976 Salim Ibn Abi Bakr Shaikan St, 2223 West Umm Al Hamam District Riyadh, 12329 Riyadh, Kingdom of Saudi Arabia, Tel: +966 11 838 3600. CR No, 1010479419. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA or any other authority or regulator located in KSA has approved this information. In the United Arab Emirates this material is only intended for -natural Qualified Investor as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA or any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, to sophisticated institutions who have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document, does not constitute and should not be construed as an offer of, invitation, inducement or proposal to make an offer for, recommendation to apply for or an opinion or guidance on a financial product, service and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to the Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, The Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association) for Institutional Investors only. All strategies or products BLK Japan offer through the discretionary investment contracts or through investment trust funds do not guarantee the principal amount invested. The risks and costs of each strategy or product we offer cannot be indicated here because the financial instruments in which they are invested vary each strategy or product. In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation, needs or circumstances. In New Zealand, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL) for the exclusive use of the recipient, who warrants by receipt of this material that they are a wholesale client as defined under the New Zealand Financial Advisers Act 2008. Refer to BIMAL’s Financial Services Guide on its website for more information. BIMAL is not licensed by a New Zealand regulator to provide ‘Financial Advice Service’ ‘Investment manager under an FMC offer’ or ‘Keeping, investing, administering, or managing money, securities, or investment portfolios on behalf of other persons’. BIMAL’s registration on the New Zealand register of financial service providers does not mean that BIMAL is subject to active regulation or oversight by a New Zealand regulator. In China, this material may not be distributed to individuals resident in the People’s Republic of China (“PRC”, for such purposes, not applicable to Hong Kong, Macau and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx.

©2025 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

BIIM0625U/M-4619207

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All