Executive Summary

The opportunity set for emerging market (EM) equities has changed dramatically over the past three and a half decades – geographically, at a sector level, and in terms of market capitalization.

But even as the composition and characteristics of EM evolve, we believe one thing remains consistent: EM equities continue to offer investors the opportunity to add value to their portfolios. As economic growth has translated into increased breadth, depth, and maturity in the EM capital markets, investors now have access to more building blocks than ever before, from indexing, fundamental active, and quantitative, to thematic, regional, and country-specific.

In this paper, Altaf Kassam, Kamal Gupta, and Alejandro Gaba outline the key points to consider and practical steps for creating an effective emerging market equity portfolio.

Key takeaways:

- Broader openness to active approaches can improve portfolio efficiency.

- Enhanced strategies can play a pivotal role in boosting portfolio efficiency, offering a compelling balance of alpha potential, scalability, and cost-effectiveness.

- Small-cap active exposures deserve a strategic role — even in conservative risk budgets and under cautious beta assumptions — thanks to their diversification and robust alpha potential.

- Focusing on net alpha maximization — even within strict fee regimes — can enhance outcomes more effectively than mechanically adjusting unconstrained portfolios by eliminative higher-fee segments.

This is a framework for allocators seeking a structured, evidence-led approach to evaluate design trade-offs and make more informed EM portfolio decisions.

The changing face of EM equity investing

The opportunity set for EM equities has changed dramatically over the past three and a half decades. When the MSCI EM Index was first introduced in 1988, it represented ten economies. Each of these could be roughly characterized as “underdeveloped, but growing rapidly.” By the end of Q1 2025, there were twenty-four economies reflected in the Index, and there is a healthy debate over whether some of its constituent economies, capital markets, and infrastructures are too mature to even qualify for the “emerging” label.

The current EM Index is quite different from its initial incarnation, as economic growth has translated into increased breadth, depth, and maturity in the EM capital markets.

- In geographic terms, Asian firms made up nearly 46% of the EM Index at inception. As of end-Q1 2025, this number has jumped to over three-quarters of the Index, with China accounting for more than 30% and India inching close to the 20% mark.

- At a sector level, the EM Index’s tilt has shifted from production to consumption, with the financial, technology, consumer discretionary, and communications sectors displacing, to some extent, materials, staples, and industrials.

- Finally, in terms of market cap, mega- and largecap stocks1 make up over 60% of the EM Index as of end-Q1 2025. Twenty years ago, these two capitalization categories together made up less than 20% of the total Index weight. While the nominal market capitalization of listed equities has increased over this period, the proportionate increase in mega- and large-cap companies in the EM Index has been much higher than in the Developed Market (DM) Index.

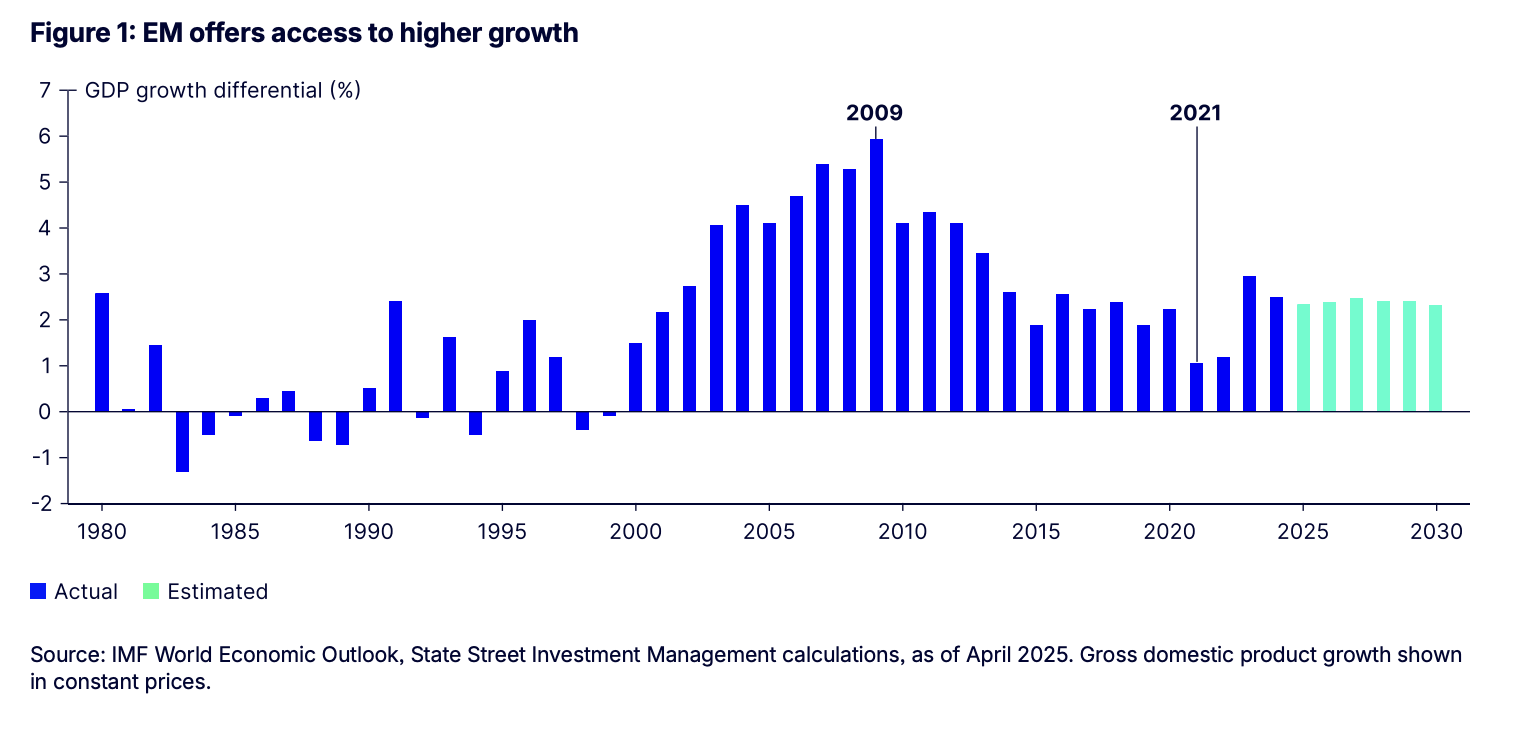

Even as the composition and characteristics of EM change, EM equities continue to offer investors access to faster-growing economies — a dynamic that has held true especially since the early 2000s. The GDP growth differential between emerging and developed markets is expected to return to its pre-COVID baseline, as shown in Figure 1.

As of end-Q1 2025, EM represents a little over 10% of the MSCI All Country World Index (ACWI), a widely followed benchmark for global equity exposure. This is notably disproportionate to EM’s role in the global economy, where it accounts for 41% of global nominal GDP2 and contributes the majority of global GDP growth. As EMs continue to develop and become more integrated into global markets, their influence is likely to grow. That said, given the non-trivial transfer of EM economic strength into equity market outperformance, we believe a more nuanced approach is needed — one that looks beyond index-based investing. In the following sections, we examine key considerations for building effective EM equity exposure, including the role of indexing, the relevance of core factors, the case for active management, and opportunity in EM small caps. Within this, we explore the role of various portfolio building blocks. Finally, we will conclude by presenting a set of optimal EM equity portfolio allocations to serve as a foundation for further thinking.

EM indexing: A foundation, not a finish line

- Best-in-class EM index managers can mitigate many of the higher trading costs prevalent in EM through smart portfolio construction and efficient trading.

- While indexing remains a valuable component of EM portfolios, the uneven transmission of economic growth into indexed equities’ performance, as well as their higheralpha opportunities, highlights the need to look beyond indexing to fully capture the EM opportunity set.

Indexed investments in EMs have been gaining popularity in recent years, offering low-cost, scalable exposure and serving as a valuable source of liquidity — especially for large investors. Market-cap weighted index strategies provide a simple and efficient way to access broad EM exposure, and they continue to play a significant role in investor portfolios. That said, implementing index exposures in EM can be more complex than in developed markets, given local execution dynamics.

Historically, higher trading costs, liquidity constraints, and market frictions often resulted in non-trivial performance drag and wider tracking error — especially when compared to developed market index funds. Emerging markets have come a long way with improving liquidity and market structures, though some of these challenges such as capital controls and settlement delays persist. Best-in-class EM index managers can mitigate many of these challenges through smart portfolio construction and efficient trading, especially around index rebalance periods — narrowing the gap between fund and benchmark returns.

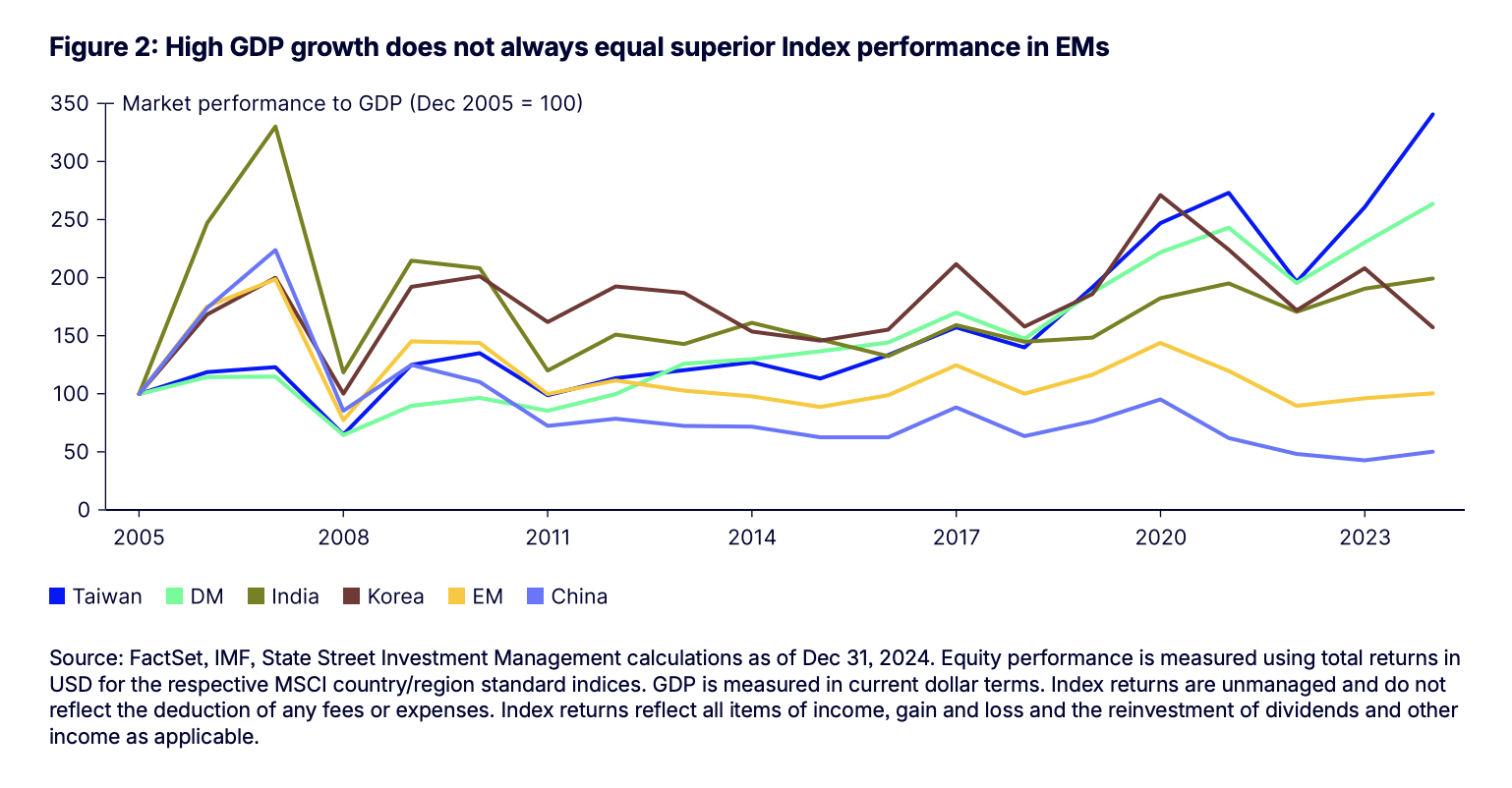

These issues are not exclusive to index strategies, but they tend to be more binding in passive portfolios due to their rigid structures. Beyond these implementation challenges, there is a deeper issue: The weak and uneven transmission of EM economic strength into equity market returns, as we show in the below figure. While markets like Taiwan and India — and to some extent Korea — have effectively turned their economic growth advantage into equity performance, others such as China have significantly lagged the major developed and emerging equity markets despite strong economic growth. This uneven transmission between economic fundamentals and equity outcomes means that passive benchmarks may not fully capture the breadth of EM opportunity set.

Given both the structural inefficiencies of index implementation and the highly heterogeneous nature of growth-to-performance transmission, we advocate a more nuanced approach for accessing the EM equity opportunity set. In the next section, we move up the activeness spectrum to explore the role of active approaches.

Seeking opportunity along the activeness spectrum

- Core factor strategies can provide a transparent, low-cost foundation for capturing risk premia in EM. They serve as a scalable midpoint between indexing and active management, and a natural entry point for investors progressing along the active spectrum.

- Enhanced strategies can deliver riskadjusted returns at scale, with fee efficiency, making them especially attractive for institutions seeking consistent outcomes.

- Active strategies can capture the full EM opportunity set by exploiting macro shifts, cross-sectional dispersion, and under-researched segments like small caps.

As discussed in Casting a Wide Net: Why True Passive Strategies Are Rare Catches, activeness is not a binary choice between passive and active — it is a spectrum that spans from systematic beta strategies to enhanced and fully active approaches. Each strategy type offers a different balance of simplicity, transparency, and acceptance, and thus appeals to different investor preferences, risk budgets, and implementation constraints.

Systematic factor solutions in EM: Low-fee access to the EM active opportunity set

Systematic factor solutions sit closer to the index end of the spectrum. They are typically high in simplicity and transparency, and are widely adopted by market participants. These strategies offer low-cost, rules based exposure to academically validated factors like Value, Quality, Small Size, Low Volatility, and Momentum.

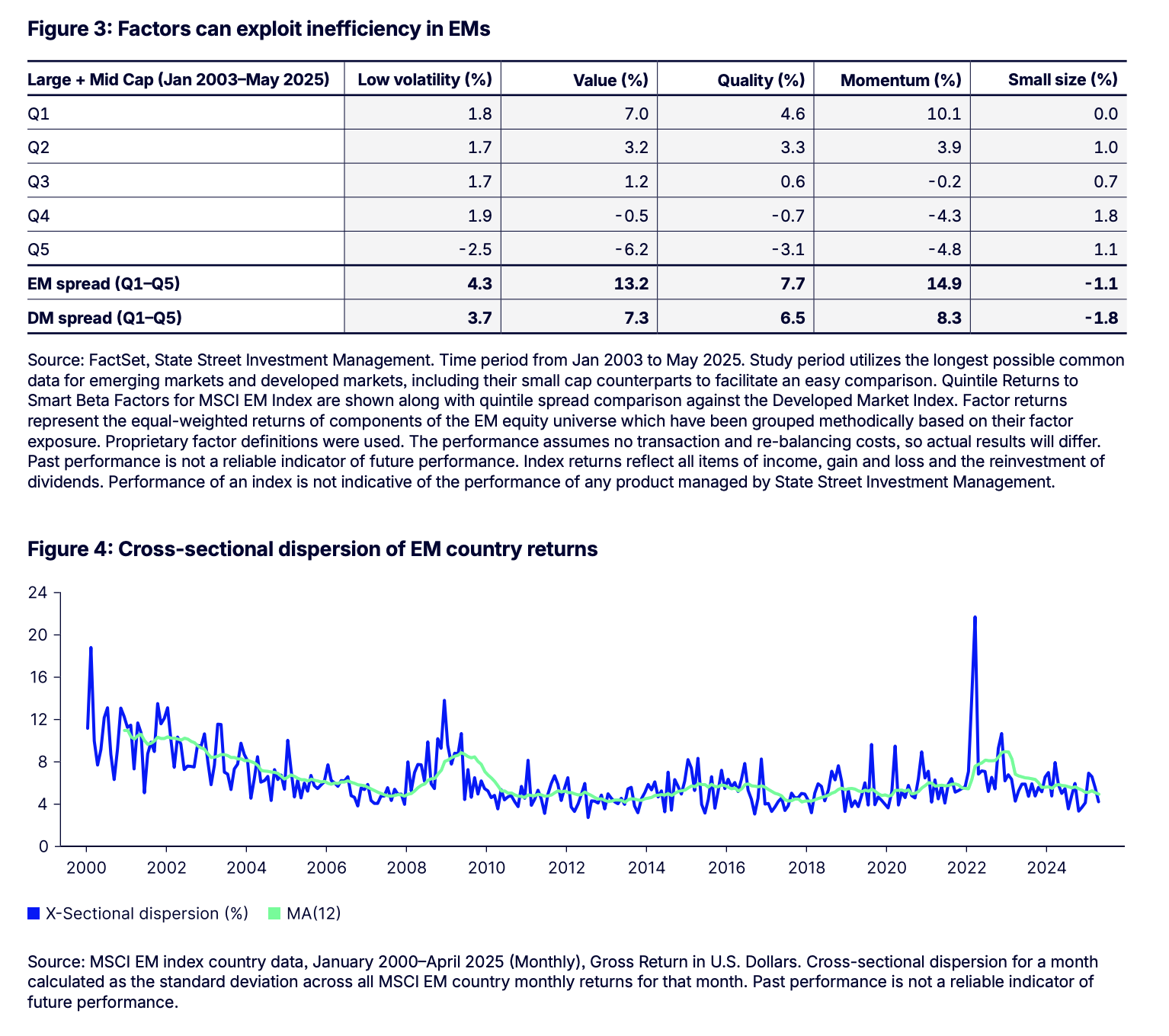

Their appeal is reinforced by the empirical evidence from EMs. Our analysis of factor spreads over the past two decades, based on our proprietary factor definitions, reveals that EM present a particularly fertile ground for factor-based strategies. As illustrated in the chart below, factor return spreads in EM are robust across most factors.

Given single-factor strategies are susceptible to cyclical performance, many investors are increasingly adopting core factor strategies. These multi-factor approaches combine complementary factors to mitigate cyclicality and improve return consistency3. Our core factor approach embodies this philosophy by combining Quality, Value, and Momentum, three factors that have shown particularly strong spreads, while carefully managing factor interactions to ensure robust diversification and more reliable outcomes.

Core factor strategies offer a compelling middle ground between index and active approaches. Like capweighted indexing approaches, they provide liquidity, scalability, and cost-efficiency, making them suitable for large institutional portfolios. At the same time, by systematically tilting toward premium factors, they have the potential to deliver excess returns over the benchmark in the long term. For fee-sensitive investors, core factor strategies represent a pragmatic choice — offering low-cost, diversified access to factor premia while maintaining transparency and discipline.

Importantly, these strategies can also serve as a stepping stone along the active spectrum: Investors seeking to further enhance returns or express more nuanced views can build upon this foundation by moving toward more active, high-conviction approaches.

Active management in EM

Core factor strategies offer a simpler, scalable, and transparent way to capture long-term factor premia in EM. However, their simpler, static, and less adaptive nature limits responsiveness to changing market conditions and makes them vulnerable to factor crowding and mean-reverting environments. This can lead to extended periods of underperformance, especially when dominant factors fall out of favor.

Read more here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© State Street Global Advisors

Read more commentaries by State Street Global Advisors