At GMO, we believe that valuation matters. The price you pay for a security usually has a material impact on the return delivered by that particular investment.

Within credit, valuation is almost always framed as an investment’s spread premium over the risk-free rate. 1 Currently, spreads in most credit markets are at or close to historically tight levels, meaning that investors are locking in significantly lower levels of compensation than they have, on average, over the past several decades.

How should credit investors navigate such an environment from a valuation perspective?

We think they should focus on not only nominal spread (which reflects the spread the investor earns to maturity), but on mark-to-market risk over some shorter holding period (a year is a reasonable and common framework).

Mark-to-market (MTM) risk, specifically, is the risk that the credit instrument’s spread widens enough over the holding period for the investment to underperform a comparable-duration Treasury bond or risk-free security.

When spreads are at historically tight levels, the mark-to-market risk for certain sectors with longer maturities can be very one-sided and negative.

There are three reasons this is the case:

1. When spreads are very tight, they have a greater chance of widening in the future than tightening.

And even if the odds of widening aren’t higher, the magnitude of potential widening is much higher than a corresponding tightening would be because spreads have a lower bound.

2. Tight spreads are easier to overwhelm on a mark-to-market basis.

Simply put, a bond with an annual spread of 100 basis points (bps) starts underperforming Treasuries if the market price drops by a point, while the same bond purchased with a spread of 250 bps requires a much larger 2.5-point drop prior to generating a negative excess return.

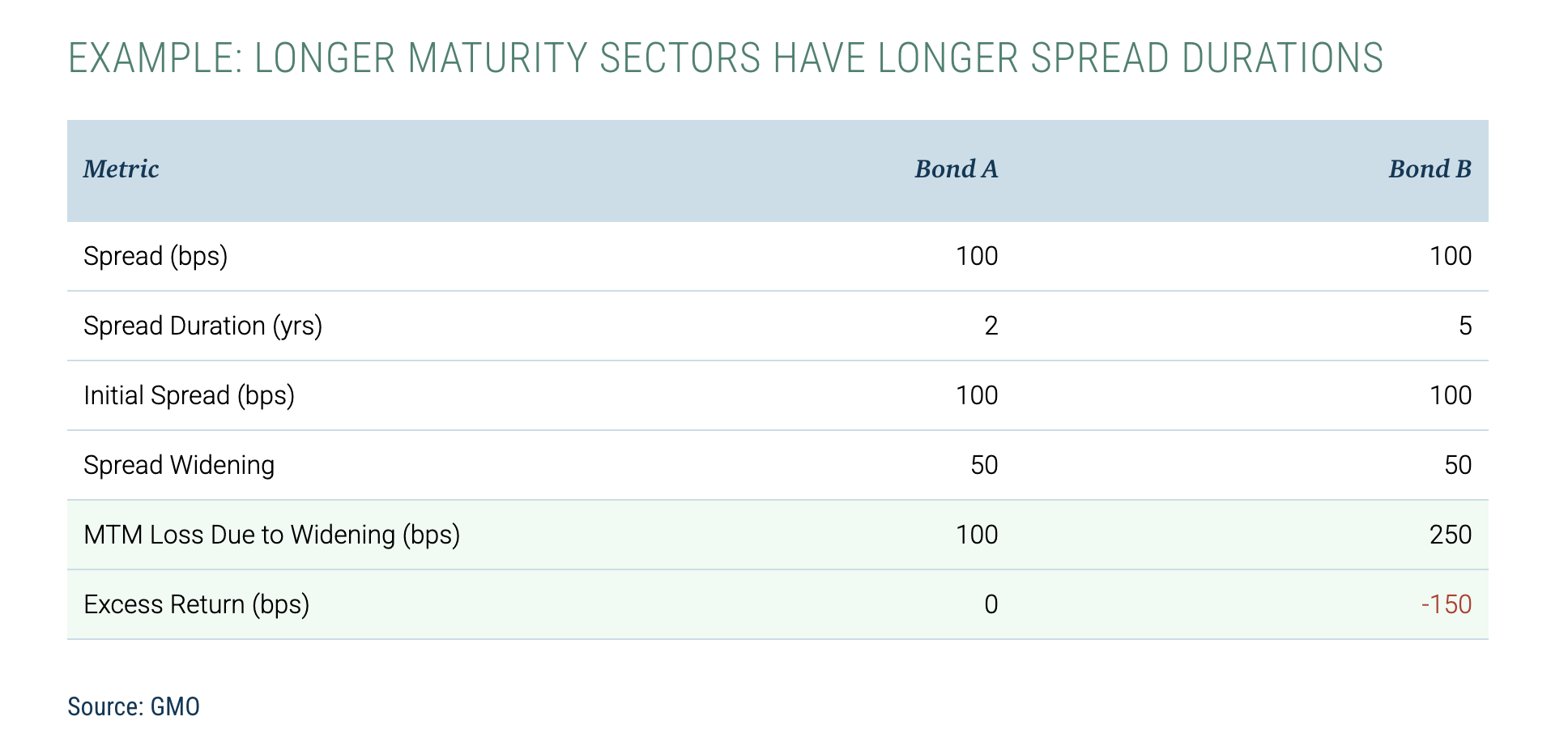

3. Longer maturity sectors have longer spread durations, which sets up a profile that more easily underperforms in a spread-widening scenario.

As an example, consider two bonds with respective spread durations of 2 and 5 years. Both start the period with market spreads of 100 bps and, after a widening, end the year with market spreads of 150 bps. The 2-year bond finishes the year flat with Treasuries because its mark-to-market loss (2 years X 50 bps) exactly offsets the 100-bp spread earned at purchase. The 5-year bond, however, underperforms Treasuries by 150 bps: its mark-to-market loss (5 years x 50 bps) significantly overwhelms the 100-bp spread earned at purchase.

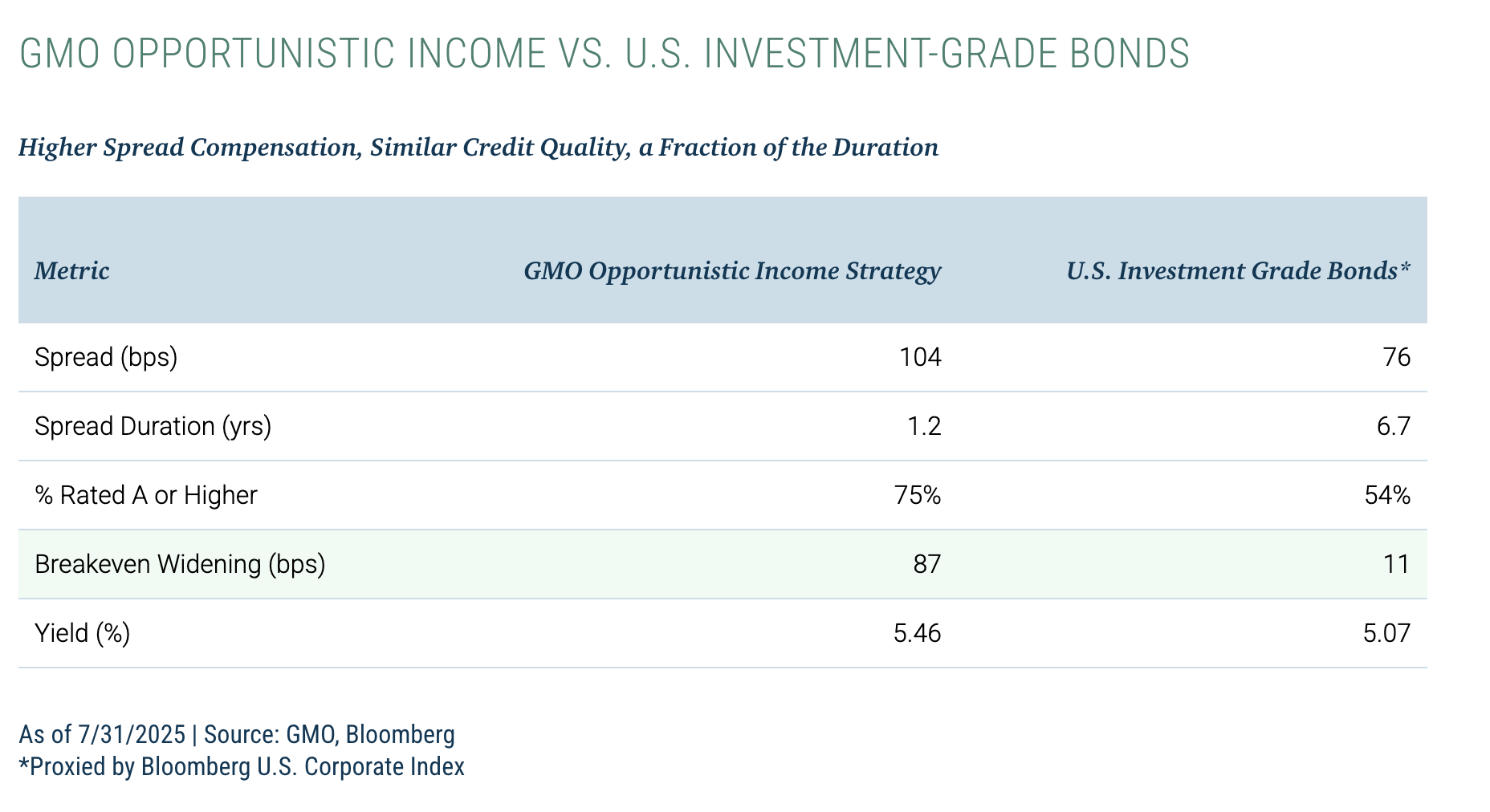

We believe the investment-grade corporate sector currently has a significantly negative exposure to these dynamics. By some measures, investment-grade corporate spreads haven’t been at levels this tight since before the Global Financial Crisis. Further, the sector has a very long spread duration of close to 7 years.

At GMO, our research has shown that investment-grade corporate bonds rarely outperform similar-duration Treasuries over the next year when spreads are this tight. So to buy into investment-grade credit today (vs. buying Treasuries), you really must believe that “this time is different.”

We think a far superior option in the current environment is to invest in the safer parts of the structured credit market. In these areas, spreads are not as tight relative to historical norms and may be achieved with what we believe to be considerably lower spread duration, and therefore reduced mark-to-market risk, compared to longer-duration sectors like investment-grade credit.

In the table below, we compare U.S. investment-grade corporates to GMO’s Opportunistic Income Strategy, which as of this writing, is generating higher spread compensation with similar (to even modestly better) credit quality and a fraction of the spread duration. This enables the strategy to continue to outperform a risk-free investment over a one-year holding period, even if spreads widen by 80+ bps, compared to investment-grade corporates, which start to underperform after just 11 bps of widening.

All else being equal, we believe that when spreads are very tight, a shorter spread duration offers investors a margin of safety compared to longer spread duration bonds. The investor’s “breakeven” is more favorable. Over the nearly 15 years we have been managing the Opportunistic Income Strategy at GMO, we have managed to return 3.2% (net) over the risk-free rate annually (measured by the Bloomberg U.S. Treasury 1-3 Years Index) and 1.4% over investment-grade bonds. 2 There have been few other moments during that period when shifting from investment-grade bonds into structured products has made more sense.

1. Measured by a duration-matched Treasury bond or risk-free security.

2. From inception to date through 7/31/2025.

Disclaimer: The views expressed are the views of Joe Auth, Ben Nabet, and Mina Tomovska through the period ending August 2025 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2025 by GMO LLC. All rights reserved.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© GMO

Read more commentaries by GMO