July Corporate Bankruptcies Hit Highest Level Since 2010

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCorporate bankruptcies hit a 14-year high in 2024, and the pace continued through the first seven months of 2025.

This should throw cold water on those who imagine the U.S. economy is booming, and it underscores the Catch-22 facing the Federal Reserve as it wrestles with interest rate policy to battle sticky price inflation.

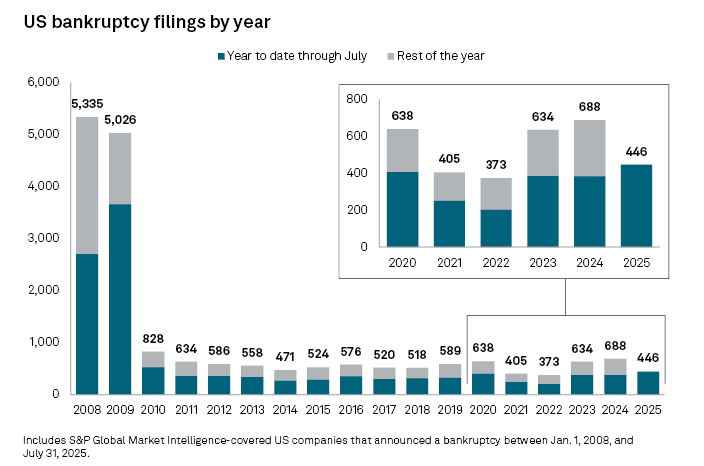

In July, corporate bankruptcies hit the highest monthly total (71) since July 2020 when governments shut down the economy for the pandemic, according to data compiled by S&P Global.

That number was up from 66 bankruptcy filings in June.

Through the first seven months of 2025, 446 companies filed for bankruptcy. That was the most for any 7-month period since 2010, in the midst of the Great Recession.

S&P Global data includes companies with public debt and assets or liabilities of at least $2 million or private companies with assets or liabilities of at least $10 million at the time of filing.

Three companies entered the bankruptcy process in July with more than $1 billion in assets and liabilities at the time of their filings: LifeScan Global Corp., Genesis Healthcare Inc., and Del Monte Foods Inc. subsidiary Del Monte Foods Corp. II Inc.

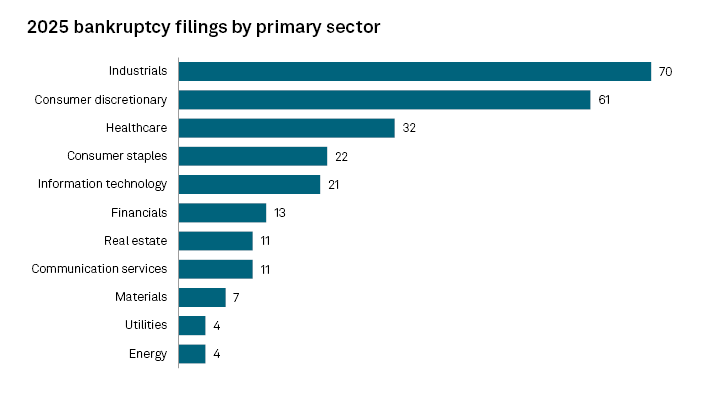

The industrial and consumer discretionary sectors reported the most filings so far in 2025, with 70 and 61, respectively.

Consumer discretionary is a category of businesses that sell goods and services considered non-essential. According to S&P Global, this sector “has been particularly susceptible to economic headwinds, even with strong overall U.S. retail sales activity, as consumer buying trends have shifted and budgets have tightened due to inflation.”

According to S&P Global, companies are struggling in this higher interest rate environment. Uncertainty surrounding tariffs is also straining companies.

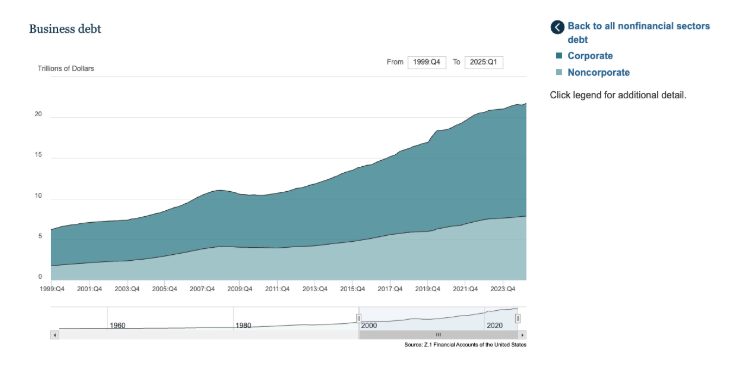

U.S. businesses are buried under a massive debt load totaling $21.75 trillion as of the end of the first quarter, according to Federal Reserve data.

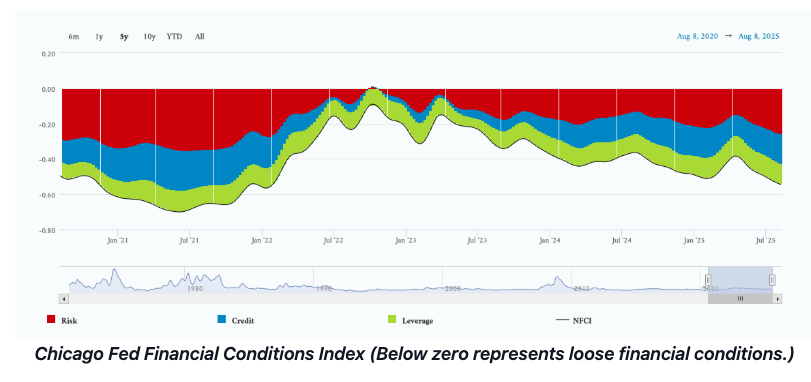

This is one of the reasons the markets are desperate for interest rate cuts. However, it’s not altogether clear that a Fed move will relieve corporate strain. While the central bank can push the short end of the yield curve down, the longer end is a different story, as pointed out by BCA Research bond strategist Ryan Swift.

"Yields at the front-end of the Treasury curve would almost certainly come down in any reasonable scenario where the Fed is cutting rates, but the very long end for the 10-year or 30-year is more in doubt. If yields don't come down, then there is no economic benefit to borrowers from the rate cuts. But rate cuts could ignite animal spirits and send risk assets higher in the near term."

In fact, 10-year Treasury yields rose after the Fed slashed rates by 1 percent at the end of 2023. The Treasury market has continued to show strain ever since, with bond prices falling and yields rising.

The Fed is between a rock and a hard place. The debt strain (not only on corporations, but also on consumers and the U.S. government) provides a strong argument for rate cuts. However, inflation clearly isn't dead.

Ironically, the Fed is a primary reason businesses are saddled with so much debt to begin with. The central bank held interest rates at zero for nearly a decade after the 2008 Financial Crisis and dropped them back to that level during the pandemic. Even at the height of the Fed’s tightening cycle, monetary policy remains historically loose.

This incentivized borrowing, blowing up this massive debt bubble.

The current situation puts the Federal Reserve in an impossible situation. It simultaneously needs to hold rates steady to keep price inflation at bay and lower rates to keep the air in the debt bubble.

It can’t do both.

Mike Maharrey is a journalist and market analyst for Money Metals with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

Our Service, Use, and Transaction Terms (“Terms”) and Privacy Policy (collectively, the “Policies”) govern your access to and use of this Website. By using the Website or engaging in transactions with Money Metals, you acknowledge that you have read and agree to be bound by the Policies, which are incorporated herein by reference. NOTICE REGARDING MARKET RISKS, ORDER ACCEPTANCE, AND CANCELATIONS: By placing an order online or over the phone with Money Money Metals Exchange, you agree to be bound by our Terms and liable for any and all losses in value of the items you ordered. You may not cancel any order after you place it with Money Metals. If you fail to follow through with timely payment on an order, you are responsible to Money Metals for any monetary damages (including, but not limited to, market losses, collection fees, setoffs, etc).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All